Quantitative developers (QDs) are the backbone of modern trading systems, translating financial models into high-performance code. They work at hedge funds, proprietary trading firms, and investment banks, earning starting salaries between $250,000 and $400,000. Their work ensures trading infrastructure operates with precision and speed, often requiring expertise in programming (Python, C++, Rust), mathematics (probability, linear algebra, stochastic calculus), and financial systems (derivatives pricing, market protocols like FIX and OUCH).

Key Takeaways:

- What QDs Do: Build trading platforms, data pipelines, and risk tools.

- Where They Work: Hedge funds (Citadel, Jane Street), banks (Goldman Sachs), and fintechs.

- Skills Needed: Python for research, C++ for production, math for modeling, and low-latency systems knowledge.

- Tools: Libraries like NumPy, QuantLib, and backtesting engines (LEAN, Moonshot).

- Infrastructure: VPS hosting with ultra-low latency (e.g., QuantVPS) is critical for live trading.

Career Path:

- Education: STEM degree (CS preferred); MFE or CQF helps.

- Learning Roadmap: Start with Python, financial math, and move to advanced systems.

- Portfolio: Build production-grade projects like trading bots and data pipelines.

- Interviews: Prepare for coding, math, and system design challenges.

Becoming a QD requires technical expertise, financial knowledge, and the ability to build reliable systems for high-stakes environments. If you're ready to dive in, focus on mastering the skills and tools that power this competitive field.

Core Skills and Knowledge Areas

Quant developers need a strong foundation in technical skills to make the most of modern infrastructure. Here's a closer look at the key areas they must master.

Programming and Software Engineering Skills

Quant developers work across two main layers: research, primarily using Python, and production, where C++ dominates. Python is the go-to for tasks like data analysis, backtesting trading strategies, and machine learning, thanks to libraries like NumPy, Pandas, and PyTorch. Once a strategy is validated, it’s often re-implemented in C++ for production, where performance and ultra-low latency (measured in microseconds) are critical.

In high-frequency trading, Rust is gaining traction for building high-frequency trading infrastructure. For firms like Jane Street, expertise in OCaml is also essential, alongside C++. Beyond languages, developers must have a strong grasp of data structures, algorithms, concurrency, and version control systems.

Math and Finance Foundations

A solid mathematical background is what separates basic coding from true model development. Quant developers need to be fluent in:

- Probability: Covering distributions, Bayesian inference, and problem-solving.

- Linear Algebra: Including principal component analysis, covariance matrices, and eigendecomposition.

- Stochastic Calculus: Such as Itô's Lemma and partial differential equations.

On the finance side, understanding derivatives pricing is crucial. John Hull's Options, Futures and Other Derivatives is a staple in the field, while Paul Wilmott's Quantitative Finance helps build intuition for stochastic calculus. For example, the Black-Scholes equation can be likened to the heat equation, with an added term for interest rates.

Equally important is recognizing the limitations of these models. The collapse of Long-Term Capital Management (LTCM) in 1998 is a key lesson. Despite being co-founded by Nobel laureates, LTCM's reliance on mathematical elegance failed when real-world conditions shifted. With a 265:1 notional-to-equity ratio (roughly $1.25 trillion in derivatives against $4.7 billion in equity), the fund lost $4.6 billion in just four months when asset correlations unexpectedly broke down.

Data and Infrastructure Skills

Quant developers must go beyond simply retrieving market data. They need to understand the protocols that facilitate data exchange in institutional systems. Two key protocols include:

| Feature | FIX Protocol | OUCH Protocol |

|---|---|---|

| Format | Text-based (Tag-Value) | Binary (Fixed Byte Layout) |

| Latency | 80–200 microseconds | < 25 microseconds |

| Use Case | Universal institutional trading | Ultra-low-latency order entry (NASDAQ) |

| Parsing | High overhead | Zero overhead (direct buffer read) |

Run 24/7 while you sleep. Keep bots, platforms, and trade copiers online on a dedicated VPS.

Low-latency VPS hosting for your trading platform.

From $59.99/mo

For ultra-low-latency systems, binary protocols like OUCH are preferred, as they eliminate ASCII parsing overhead and dramatically reduce latency. Developers must also understand advanced techniques like kernel-bypass networking (using tools like DPDK or Solarflare OpenOnload to save 10µs per packet), zero-copy I/O, and NUMA-aware thread pinning.

The 2012 Knight Capital incident demonstrates the risks of overlooking infrastructure. A deployment error caused unintended trades, resulting in a $440 million loss. This underscores the importance of not just performance but also robust safeguards and risk management.

"In HFT environments, the interval between error and consequence is measured in seconds, making the design of safeguards and control mechanisms as important as the performance of the system itself." - Henrico Dolfing

These skills create a foundation for leveraging advanced tools and systems, which will be explored in the next section.

Tools and Platforms Quant Developers Use

Development and Collaboration Tools

Quant developers often start with JupyterLab for research and prototyping before moving to VSCode for writing production-level code. Both tools support workflows in Python and C++ and integrate seamlessly with version control systems like Git.

AI-driven IDEs such as Cursor and Windsurf take things a step further by leveraging MCP servers to automate repetitive tasks like boilerplate coding and backtesting. For team collaboration, Docker is a popular choice. It ensures consistent development environments, so a strategy that works on a developer's laptop will function the same way on a cloud server.

Quantitative Libraries and Frameworks

Specialized libraries are at the heart of quantitative modeling. Python's extensive ecosystem offers tools that are indispensable for quant developers. The core data science stack - NumPy, pandas, SciPy, and scikit-learn - is widely used for tasks like data manipulation and machine learning. For financial modeling, QuantLib stands out as the go-to framework. Written in C++, it provides Python, R, and Java wrappers, enabling derivatives pricing, risk management, and even regulatory-grade calculations.

When it comes to strategy research and backtesting, the choice of engine depends on the complexity and type of strategy. LEAN, the open-source engine powering QuantConnect, is designed for event-driven, multi-asset modeling. It handles impressive volumes, processing over $45 billion in notional value monthly and supporting more than 375,000 live strategies since 2015. On the other hand, Moonshot is optimized for data-heavy strategies, offering backtesting speeds up to 75x faster than LEAN thanks to its vectorized, pandas-based architecture. For tasks like factor analysis and performance attribution, tools like Alphalens and Pyfolio are widely favored.

"The backtesting or analysis library that's right for you depends on the style of your trading strategies. One size does NOT fit all." - QuantRocket

Market Data APIs and VPS Hosting for Trading Systems

Once the right libraries are in place, accessing real-time market data and ensuring reliable execution become the next priorities. Platforms like QuantConnect and QuantRocket offer unified APIs that provide historical and real-time data across multiple asset classes, including equities, futures, forex, options, and crypto. QuantRocket even includes a free tier with five years of historical U.S. stock data (2007–2011), making it easy for developers to experiment with cross-sectional equity strategies without upfront costs.

When transitioning from research to live trading, infrastructure plays a critical role. Running live algorithms on a personal computer can lead to outages, hardware failures, or timing issues. A trading VPS (Virtual Private Server) solves these problems by offering dedicated resources, 24/7 reliability, and physical proximity to exchange servers. For example, QuantVPS provides hosting in Chicago with sub-0.52 ms latency to the CME - a crucial advantage for strategies that depend on precise execution timing. QuantVPS plans start at $59.99/month for VPS Lite (4 cores, 8GB RAM, NVMe storage) and scale up to servers with 128GB RAM and 10Gbps+ networking.

"This geographic optimization enables true ultra-low latency, giving traders a professional-grade execution edge." - QuantVPS

Such infrastructure ensures that validated strategies are executed consistently and without interruptions.

Career Pathways and Learning Roadmap

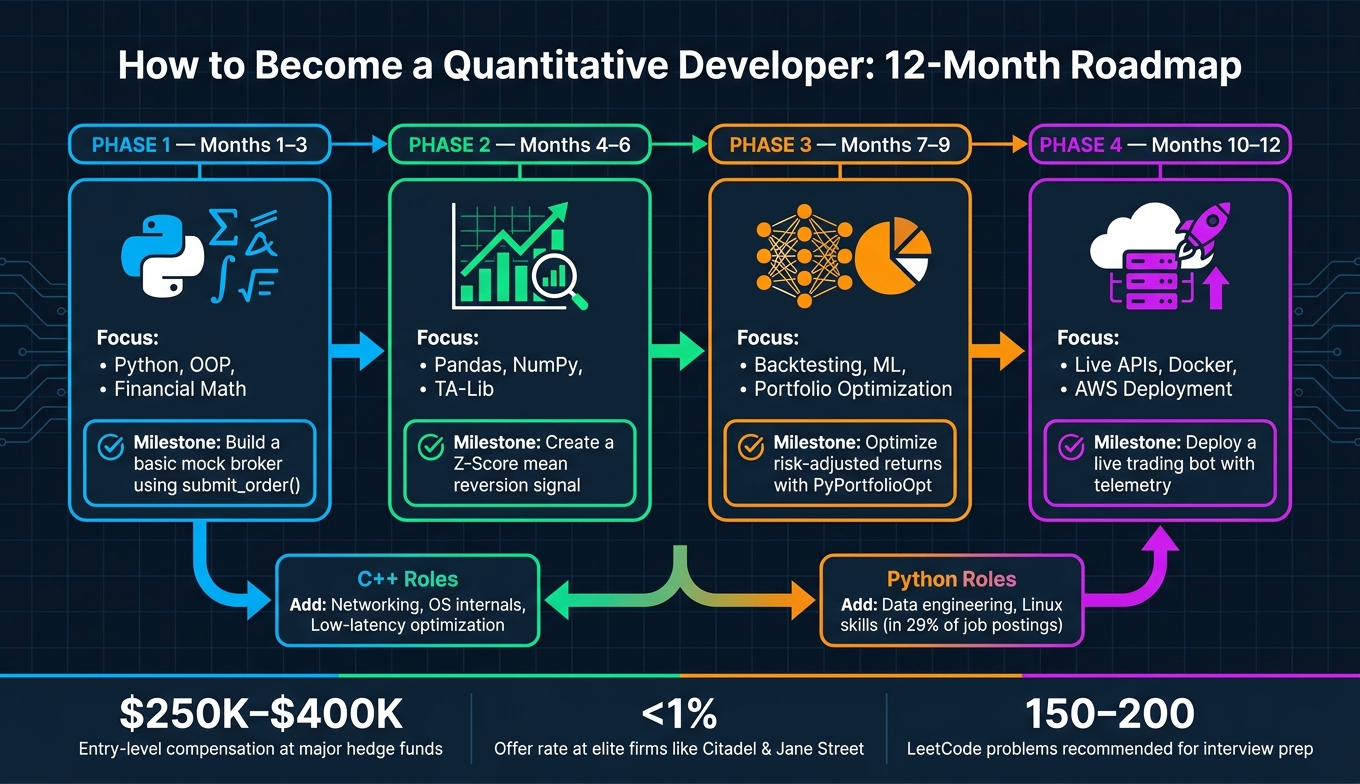

How to Become a Quantitative Developer: 12-Month Learning Roadmap

Education and Career Entry

To break into the field, a STEM degree - preferably in Computer Science - is essential. Alex McMurray from eFinancialCareers explains:

"Starting with the basics, a quant developer needs technical expertise. You'll be expected to have a degree in a STEM subject, preferably computer science, and you should demonstrate aptitude for multiple programming languages."

While a PhD can open doors at traditional investment banks and established hedge funds, it's not always a must - especially for newer proprietary trading firms. A Master's in Financial Engineering (MFE) offers a practical middle ground, providing financial markets knowledge. However, only programs from top-tier institutions carry significant weight with leading employers. Entry-level compensation at major hedge funds often ranges between $250,000 and $400,000, while managing directors on the buy side can earn up to $1.34 million.

Employers prioritize fast, functional solutions over overly academic approaches, making it crucial to focus on applying technical skills effectively in high-pressure trading environments.

Step-by-Step Learning Roadmap

Once you’ve grasped the basics, this four-phase, 12-month roadmap can guide you from learning financial theory to deploying live production systems:

| Phase | Timeframe | Focus | Milestone |

|---|---|---|---|

| 1 | Months 1–3 | Python, OOP, financial math | Build a basic mock broker using submit_order() |

| 2 | Months 4–6 | Pandas, NumPy, TA-Lib | Create a Z-Score mean reversion signal |

| 3 | Months 7–9 | Backtesting, ML, portfolio optimization | Optimize risk-adjusted returns with PyPortfolioOpt |

| 4 | Months 10–12 | Live APIs, Docker, AWS deployment | Deploy a live trading bot with telemetry |

The leap from Phase 3 to Phase 4 is often the most challenging. Transitioning from backtesting on static data to managing real-time WebSocket feeds, handling API rate limits, and dealing with missing ticks introduces a whole new layer of complexity. If you're aiming for C++ roles, it’s wise to add studies in networking, operating systems, and low-latency optimization. For Python-focused roles, sharpening your data engineering skills and mastering Linux - featured in nearly 29% of quant developer job postings - can give you an edge.

Certifications and Study Resources

Certifications and structured learning programs can help you stand out, especially if you're self-taught or new to finance.

The Certificate in Quantitative Finance (CQF) is one of the most respected credentials in the field. This six-month program covers practical quant techniques and machine learning, boasting an alumni network of over 11,500 professionals across 23 years. Borja Garcia Haendler, Head of Market Risk and Product Control Asia at Julius Baer, shares:

"If you are looking to enhance your expertise in quantitative finance, I highly recommend the CQF as an invaluable investment in your professional journey."

For software development, the Quantitative Developer Certificate (QDC) is a six-month course covering Python, C++, and kdb+/q, a high-frequency time series database widely used in HFT. Paul Alexander Bilokon, a kdb+/q expert, notes:

"Knowing the high-frequency time series database kdb+/q will not only increase your earning potential but also set you apart from the competition."

Other standout programs include:

Stay online and closer to execution. Choose a VPS location for CME futures, New York markets, London FX, API trading, and more.

Host your platform near the market route that matters.

From $59.99/mo

- QuantNet C++ Programming for Financial Engineering: Priced at $1,450, this 16-week course has a stellar 4.93/5 rating from over 1,420 reviews. With more than 4,000 alumni, it’s a popular stepping stone into elite MFE programs.

- Certificate in Python for Finance (CPF): Created by Dr. Yves J. Hilpisch, this program includes over 400 video hours and 100,000+ lines of code, blending AI techniques with financial applications.

For those on a budget, The Quant Prep, an open-source GitHub resource, offers an eight-stage roadmap. It covers low-latency C++, system design, and HFT architecture, complete with code for order matching engines and Black-Litterman models.

Building a Portfolio and Landing a Quant Developer Job

How to Build a Portfolio with Example Projects

Creating a standout portfolio is crucial for showcasing your skills as a quant developer. Focus on building production-ready systems like data pipelines, event-driven backtesting engines, and order management systems. For example, you could develop data pipelines that leverage real-time APIs, or design backtesting engines using libraries like vectorbt or Backtrader. If you're aiming for high-frequency trading algorithms and HFT roles, consider implementing advanced tools like a binary OUCH message builder to achieve ultra-low latencies - think under 25 microseconds.

Your projects should reflect rigorous testing and validation. Use techniques like walk-forward analysis and sealed holdout sets to demonstrate your understanding of backtest overfitting and how to address it. In your project READMEs, quantify your achievements. Specific metrics - like "reduced forecast error by 8%" or "achieved sub-microsecond latency in per-tick pipelines" - carry far more weight than generic descriptions. Treat your GitHub repositories as an extension of your resume. Firms often review these profiles for code quality and project depth, so make them shine.

Finally, complement your portfolio by participating in hands-on competitions and conducting live testing. These experiences not only validate your skills but also add credibility to your work.

Ways to Gain Practical Experience

Competitions and live-simulated environments are excellent ways to gain practical experience. Competitions like IMC's Prosperity, Citadel's datathons, and Jane Street programs serve as direct hiring pipelines. Excelling in these events can even help you bypass traditional screening processes. Similarly, achieving strong rankings on platforms like WorldQuant's BRAIN or Kaggle can act as a substitute for formal industry experience.

Deploying your systems in live-simulated environments is another way to hone your skills. For example, using QuantVPS allows you to test your bot under near-production conditions. A VPS with 0–1ms latency and a 1Gbps+ network connection can help you evaluate how your system handles real-time WebSocket feeds, API rate limits, and missed ticks. Unlike running a bot on a local machine - where network jitter and downtime can interfere - a dedicated VPS ensures smoother execution. QuantVPS plans start at $41.99 per month when billed annually, making it a practical investment for serious developers.

Job Search and Interview Preparation

Once your portfolio and practical experience are in place, it's time to focus on targeted interview preparation. Quant developer interviews often test a mix of skills. Allocate your preparation time roughly as follows: Probability & Statistics (35%), Coding & Algorithms (25%), Brain Teasers (20%), Mental Math (10%), and Finance/Markets (10%). Keep in mind that different firms have different focuses. For instance, Citadel Securities and HRT often emphasize deep C++ knowledge and multithreading, while Two Sigma may lean more toward Python and statistical modeling.

To prepare technically, aim to complete 150–200 LeetCode problems, prioritizing areas like sliding windows, heaps, graphs, and dynamic programming. For mental math, daily practice on platforms like Zetamac can help - scores of 60 or higher are considered strong for firms like Optiver or Akuna. Additionally, be ready to tackle system design challenges during interviews. You might be asked to sketch out complex systems, such as a limit order book or a zero-copy market data handler.

During interviews, articulate your thought process clearly. Interviewers value candidates who explain their assumptions, consider edge cases, and discuss tradeoffs as they solve problems. For senior roles, expect questions about deployment architecture and historical incidents. As Henrico Dolfing, a Technical Case Study Author, puts it:

"In HFT environments, the interval between error and consequence is measured in seconds, making the design of safeguards and control mechanisms as important as the performance of the system itself."

Landing a job at elite firms like Citadel or Jane Street is highly competitive - offer rates are typically below 1%. This means you’ll need a solid preparation plan, usually 2–4 months of focused, daily study. Foundational resources like John Hull's Options, Futures and Other Derivatives can help you understand market mechanics, while Xinfeng Zhou's A Practical Guide to Quant Interviews (often called the "Green Book") is invaluable for tackling probability and brain-teaser questions.

Conclusion

Becoming a quantitative developer is a journey that requires dedication and a clear roadmap. It begins with mastering key programming languages like Python for research and C++ for production-level execution. Alongside these skills, building a strong foundation in mathematics - particularly in probability and stochastic calculus - is essential. Equally important is gaining a deep understanding of market mechanics, including order books, matching engines, and financial protocols like FIX and OUCH.

Once the technical groundwork is in place, the focus shifts to creating real-world systems. A portfolio that includes production-grade projects - such as backtesting engines, data pipelines, and order management systems with measurable outcomes - speaks volumes about your capabilities. These practical demonstrations of skill are often more impactful than a traditional resume.

One area where developers often fall short is infrastructure. The gap between a backtest and live trading can be significant. As the Viprasol Tech Team aptly puts it, "A quantitative hedge fund lives and dies by its technology infrastructure." Running systems on a dedicated VPS can mitigate risks like network jitter and downtime. For example, QuantVPS offers sub-0.52ms latency to CME matching engines and 99.999% uptime, starting at $41.99 per month when billed annually. This provides a reliable environment to simulate near-production conditions without the expense of co-location.

Finally, operational reliability is just as critical as technical expertise. Historical examples, such as Knight Capital's $440 million loss in just 45 minutes, highlight the importance of safeguards, disciplined deployments, and kill-switch mechanisms. Adopting a mindset that prioritizes these operational safeguards from the outset can give you a significant edge in the competitive world of quantitative development.

FAQs

Should I learn Python or C++ first?

Choosing between Python and C++ in quantitative finance boils down to your specific objectives. Python stands out for its ease of use and versatility, making it perfect for tasks like research, strategy development, and backtesting. On the other hand, C++ is the go-to for high-performance needs, such as high-frequency trading, where speed and efficiency are critical.

If you're just starting, Python is a great choice to build a solid foundation. Once you're comfortable, consider learning C++ if your focus shifts to low-latency systems or performance-intensive applications.

How do I prove I can build production trading systems?

To showcase your expertise in creating resilient, scalable, and automated systems, focus on projects that demonstrate your ability to handle real-time data, execution, and risk management effectively.

For instance, highlight your experience with live APIs by detailing how you've integrated real-time market data feeds into trading platforms. Explain how these APIs enabled seamless execution of trades while maintaining low latency and high reliability.

When it comes to cloud deployment, share examples of how you've leveraged platforms like AWS or Google Cloud to build scalable infrastructure. This could include deploying microservices for trading strategies or using cloud resources to process large volumes of financial data in real time.

Discuss your proficiency in backtesting frameworks by describing how you’ve designed systems to test trading strategies against historical data. Emphasize how these systems ensured accuracy, speed, and alignment with real-world market conditions.

Address risk management by outlining the safeguards you've implemented. For example, you could mention designing systems with stop-loss mechanisms, position limits, or dynamic portfolio adjustments to minimize exposure during volatile market conditions.

If you've worked on live trading systems, highlight your ability to create robust architectures that withstand market fluctuations and operational challenges. Share how you’ve implemented monitoring tools and automated alerts to ensure system reliability and prevent downtime.

Finally, emphasize your focus on operational safeguards. Describe how you’ve incorporated error handling, redundancy, and failover mechanisms to protect against system failures, ensuring uninterrupted trading operations.

By showcasing these skills and experiences, you’ll demonstrate your ability to develop and manage end-to-end production trading systems with precision and reliability.

What’s the biggest difference between backtesting and live trading?

The main distinction lies in their application: backtesting uses historical data to assess a strategy, while live trading implements it in real-time with actual money. Backtesting can uncover statistical advantages but doesn't factor in real-world variables like slippage or emotional decision-making. In contrast, live trading exposes practical challenges such as execution quality and transaction costs, offering the ultimate test of a strategy's effectiveness.