High-Frequency Trading (HFT) platforms are built for speed, processing market data and executing trades in nanoseconds. By 2026, the standard for success in HFT relies on ultra-low latency systems, advanced hardware like FPGAs, and strategic infrastructure like co-location near exchange data centers. Here's what you need to know:

- Speed is everything: A delay of just 5 microseconds can cost trades.

- Nanosecond precision: Systems now achieve tick-to-trade times under 500 nanoseconds.

- Infrastructure costs: Building HFT setups ranges from $1M–$5M, with ongoing expenses of $50K–$200K/month.

- Key technologies: FPGAs, hollow-core fiber, and microwave links reduce latency.

- AI in trading: Machine learning models are increasingly integrated for better decision-making.

HFT success depends on eliminating delays, ensuring system reliability, and maintaining consistent performance - even under extreme market conditions. The right combination of hardware, network optimizations, and location can put traders ahead in the competitive landscape.

Key Components of HFT Platform Architecture

The architecture of a High-Frequency Trading (HFT) platform is meticulously designed to handle ultra-low latency operations. It integrates real-time market data ingestion, algorithmic decision-making, and lightning-fast execution, all while embedding robust risk controls. Every layer is fine-tuned to minimize delays, using specialized hardware and software to overcome the inefficiencies of traditional systems. Here's a closer look at the critical components that enable such high performance.

Market Data Ingestion

Market data is delivered through multicast feeds over ultra-low-latency fiber connections. To further reduce latency, technologies like DPDK (Data Plane Development Kit) and RDMA (Remote Direct Memory Access) bypass the standard network stack, cutting latency down from 20–50 microseconds to an impressive 1–5 microseconds. Once the data is received, the system maintains the entire order book in RAM, leveraging efficient memory structures like lock-free ring buffers. This approach ensures near-instantaneous, disk-free access to data.

Fast Execution Systems

At the heart of the platform are execution engines that transform trading decisions into actionable orders. These engines are typically written in low-level languages like C++ or Rust, chosen for their predictable performance and minimal runtime interference. With FPGA (Field-Programmable Gate Array) acceleration, tick-to-trade execution times can range between 100–500 nanoseconds. Pre-staged order templates stored in transmit buffers allow for sub-microsecond order execution when specific market conditions are met. Additionally, Smart Order Routing systems evaluate multiple venues - such as NASDAQ and NYSE - in real time, selecting the optimal destination based on latency, fill likelihood, and fee structures.

Advanced Algorithms and Order Books

The algorithmic core of the HFT platform processes real-time data to construct a complete market view, enabling the identification of fleeting trading opportunities. Direct binary feeds facilitate the creation and maintenance of a comprehensive view of market liquidity, with the entire order book stored in RAM for immediate access. Optimized memory layouts ensure that frequently accessed data resides within the CPU's L1 and L2 caches, reducing delays caused by slower RAM access. This focus on deterministic performance ensures consistency during volatile market conditions, where reliability is just as important as speed.

Real-Time Risk Management Engines

Risk management is seamlessly integrated into the execution pipeline. Modern risk engines, often implemented using FPGA technology, can perform exposure and threshold checks in under 50 nanoseconds. Multiple layers of safeguards - such as position limits, token bucket rate limiting for order submissions, and price bands to filter out anomalous orders - ensure that security measures do not compromise speed. Deterministic kill switches add an extra layer of protection, allowing for the immediate cessation of all trading activity if needed. Even at nanosecond speeds, maintaining safety and control is non-negotiable.

Why Speed Matters in High-Frequency Trading

In high-frequency trading (HFT), speed isn't just an advantage - it's the deciding factor. A delay as small as 5 microseconds can mean losing out on profitable trades. When multiple orders hit an exchange, the first ones to reach the matching engine get executed. But it’s not just about raw speed; predictability is equally critical. For example, a stable 15-microsecond path will outperform a faster but inconsistent 9-microsecond path under load. As Sarah Jenkins, a Quantitative Strategist, aptly explains:

"If your execution path exceeds 500 microseconds, you are effectively trading history."

The key metric in HFT is the tick-to-trade loop - the time it takes from receiving market data to sending out an order. By 2026, top firms have refined this process to lightning-fast speeds of 100–500 nanoseconds using FPGA technology. This ultra-low latency is essential to avoid slippage, where price advantages can disappear during order transmission, eroding a strategy's edge. With the competition now measured in nanoseconds, speed has become the foundation for every infrastructure decision in the industry.

Co-Location Services Near Exchanges

Run 24/7 while you sleep. Keep bots, platforms, and trade copiers online on a dedicated VPS.

Low-latency VPS hosting for your trading platform.

From $59.99/mo

Co-location places trading servers directly inside exchange data centers, reducing the physical distance to the exchange’s matching engine from miles to mere meters. This proximity slashes propagation delays, bringing firms closer to the limits of physics. For instance, being based near CME’s data center in Aurora, Illinois, provides a measurable latency edge. Co-located servers also benefit from direct cross-connects, bypassing the network hops that burden retail setups. As Mohammad Mazeh, Head of Brokerage and Platform Administration at FxGrow, points out:

"Minimizing the latency from our trading infrastructure to the bridge infrastructure is a huge selling point."

However, true co-location comes with steep costs. Expenses for rack space, power, cross-connects, and specialized data feeds can climb into the tens of thousands of dollars per month. For firms unable to commit to full co-location, renting a VPS in the same city as the exchange (like Chicago for CME) is a cost-effective alternative, cutting end-to-end acknowledgment times to under 500 microseconds. Modern co-location facilities also use advanced cooling methods, such as liquid cooling, to handle the heat generated by overclocked servers. To ensure fairness, exchanges enforce equidistant cabling rules, eliminating proximity bias.

Network Optimization and Low-Latency Hardware

Standard network interface cards (NICs) introduce 20–50 microseconds of latency due to operating system overhead. Technologies like DPDK and Solarflare OpenOnload bypass the OS, mapping NIC memory directly to applications and reducing latency to just 1–5 microseconds. The choice of transmission medium also plays a massive role. Light travels 31% slower through standard fiber than through air, but hollow-core fiber (HCF) offers nearly 30% lower latency compared to traditional fiber. For longer distances, microwave and RF links beat fiber optics, achieving round-trip latencies of about 8 milliseconds compared to fiber’s 13 milliseconds. Specialized Layer 1 switches further cut latency, forwarding data in as little as 4 nanoseconds by bypassing packet buffering.

Fine-tuning hardware settings is just as important. Disabling features like hyper-threading, C-states, and frequency scaling keeps processors in high-performance states, avoiding microsecond delays. Thread pinning - assigning trading threads to specific CPU cores - reduces scheduling jitter and cache misses. Additionally, binary protocols like SBE, ITCH, and OUCH eliminate the parsing overhead of text-based FIX protocols. Looking ahead, firms are exploring low Earth orbit (LEO) satellite systems, such as Starlink and Kuiper, for global arbitrage opportunities, bypassing the limitations of undersea cables and Earth’s curvature.

While these hardware optimizations reduce transmission delays, efficient data handling is equally crucial for staying ahead.

In-Memory Data Structures

Modern HFT platforms rely on lock-free ring buffers, like the LMAX Disruptor, to eliminate contention and reduce memory-access delays. This zero-copy approach processes market data and dispatches orders without waiting for traditional memory management or operating system interrupts. Optimizing memory layout ensures frequently accessed data stays in the CPU’s L1 and L2 caches, while pre-allocated memory pools and cache-aware data structures maintain low latency. NUMA-aware memory allocation further reduces delays by ensuring each CPU core accesses its local memory bank. Using huge pages also minimizes translation lookaside buffer (TLB) misses, which can otherwise add microseconds of delay.

Infrastructure and Hardware Requirements for HFT

HFT Infrastructure Cost Comparison: Co-Location vs VPS Solutions

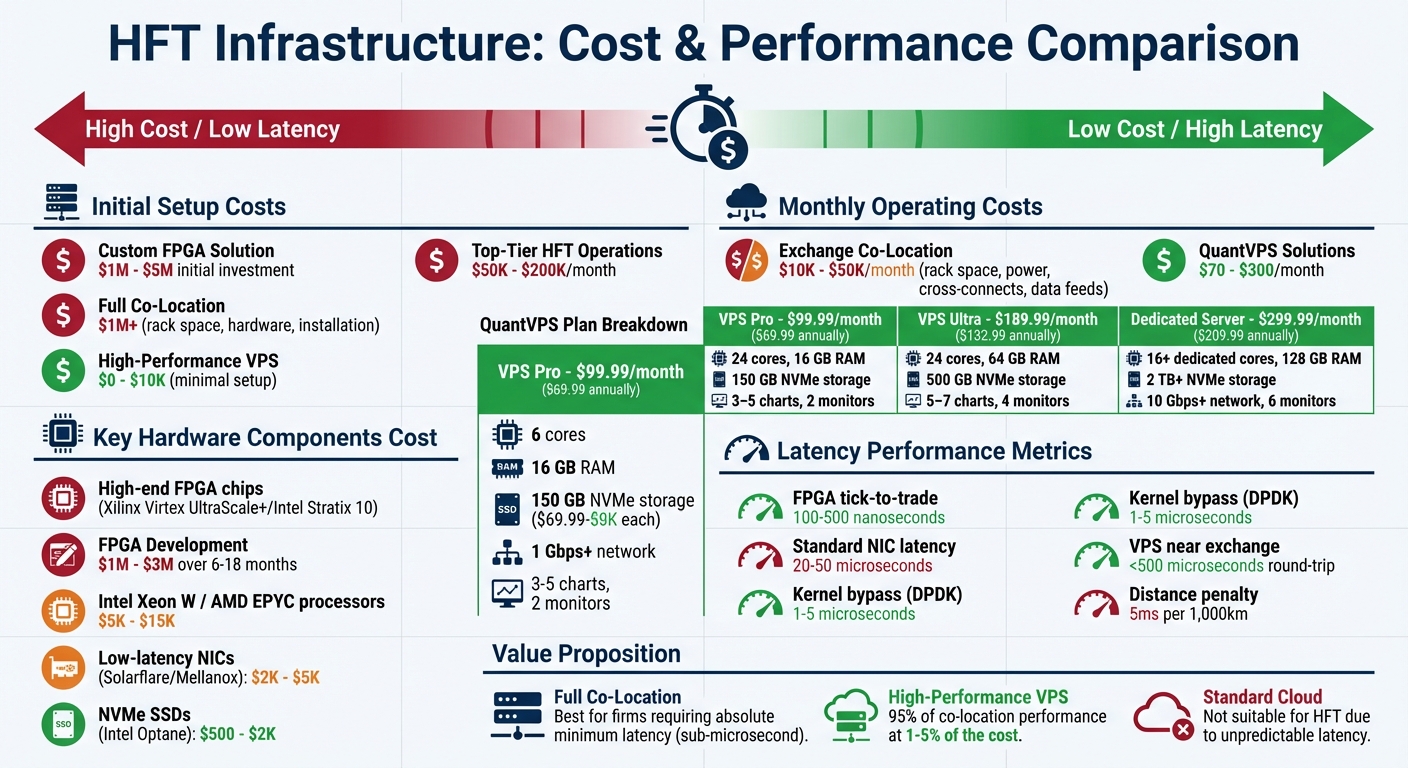

High-frequency trading (HFT) demands specialized hardware and infrastructure to maintain the precision needed for success. In this world of nanosecond-level decision-making, the hardware you choose can mean the difference between profit and loss. Building a functioning HFT infrastructure from scratch typically costs between $1 million and $5 million, with ongoing monthly expenses for top-tier operations ranging from $50,000 to $200,000.

Core Hardware Components

For HFT, the choice of processors is critical. CPUs with high single-thread clock speeds and large L3 caches are favored over those with higher core counts. Intel Xeon W and AMD Threadripper/EPYC processors are often used because they reduce execution variance. These processors work best with low-latency network interface cards (NICs) that support kernel bypass technologies like DPDK or OpenOnload. NICs from companies like Solarflare or Mellanox can cut network latency to under 5 microseconds. To avoid bottlenecks, high-performance NVMe SSDs, such as Intel Optane drives, are used for logging and state persistence.

The physical setup is just as important. Liquid cooling systems prevent overheating and ensure consistent performance, while redundant A/B power feeds safeguard against outages. Precision Time Protocol (PTP) and GPS-based clocks synchronize systems to sub-microsecond accuracy. Even small optimizations, like disabling CPU power-saving features or configuring huge pages to reduce TLB misses by 100×, contribute to the deterministic performance HFT requires.

FPGA Technology for Hardware Acceleration

Field Programmable Gate Arrays (FPGAs) are game-changers in HFT. By running trading algorithms directly in hardware, FPGAs can handle tasks like market data parsing, order book updates, and signal generation simultaneously. This parallel execution results in tick-to-trade latencies of just 150–500 nanoseconds. Unlike traditional systems, FPGAs eliminate delays caused by operating system interrupts, context switching, and cache misses, ensuring consistent latency. For example, an FPGA ITCH parser can achieve latencies under 25 nanoseconds, processing up to 150,000 orders per second.

However, this speed comes at a price. High-end chips like the Xilinx Virtex UltraScale+ or Intel Stratix 10 can cost between $20,000 and $80,000 each. Developing a custom FPGA trading system requires expertise in languages like Verilog or VHDL and can take 6–18 months, with costs ranging from $1 million to $3 million. Despite these challenges, FPGAs are highly efficient, using 3–4× less power than GPUs for similar workloads, making them ideal for dense data center environments. Modern FPGA designs even integrate pre-trade risk management into the hardware, adding only 15–25 nanoseconds of latency while ensuring compliance with regulations like SEC Rule 15c3-5. As Digital One Agency puts it:

"FPGAs don't make bad strategies good. They make good strategies unavoidable."

QuantVPS High-Performance VPS Plans

For traders who can’t justify the cost of custom FPGA solutions, high-performance virtual private server (VPS) plans offer a more affordable alternative. QuantVPS delivers dedicated CPU cycles and NVMe storage, eliminating performance issues caused by "noisy neighbors" in standard cloud hosting. This ensures the deterministic performance needed for HFT. Their edge data centers, located in key financial hubs like Equinix LD4 in London and NY4 in New York, enable sub-millisecond round-trip times.

QuantVPS offers several plans:

- VPS Pro: $99.99/month ($69.99/month annually) with 6 cores, 16 GB RAM, 150 GB NVMe storage, and a 1 Gbps+ unmetered network. Suitable for 3–5 charts and up to 2 monitors.

- VPS Ultra: $189.99/month ($132.99/month annually) with 24 cores, 64 GB RAM, 500 GB NVMe storage, and support for up to 4 monitors. Ideal for 5–7 charts.

- Dedicated Server: $299.99/month ($209.99/month annually) with 16+ dedicated cores, 128 GB RAM, 2 TB+ NVMe storage, a 10 Gbps+ network, and support for up to 6 monitors.

All plans include Windows Server 2022, full root access, and compatibility with platforms like NinjaTrader, MetaTrader, and TradeStation. Enhanced "Performance Plans (+)" are also available for firms needing more consistent performance under load.

Physical proximity to exchanges remains crucial. Light travels through fiber optic cables at about 200,000 km/s, so a server 1,000 km away adds at least 5 milliseconds of one-way delay. QuantVPS addresses this by placing infrastructure near major exchanges, offering low-latency solutions without the high costs of exchange co-location.

DDoS Protection, Uptime, and Monitoring

Strong hardware needs equally strong protection. QuantVPS guarantees 100% uptime with dual A/B power feeds, redundant generators, and automated failover systems that instantly switch to backup infrastructure during outages. DDoS protection and stateless firewalls secure the management plane without slowing down trading data.

In 2025, ArkTechnologies showcased the value of multi-site redundancy. When ISP maintenance disrupted their main Amsterdam server, clients were seamlessly rerouted to a Hong Kong node, maintaining stability. This setup demonstrates how professional infrastructure enables global scalability, with deterministic WAN links between key liquidity hubs like Chicago, Frankfurt, and Tokyo.

Real-time monitoring tracks CPU usage, memory, network throughput, and disk I/O to spot potential issues before they escalate. Automatic backups protect strategy configurations and historical data. Mohammad Mazeh, Head of Brokerage and Platform Administration at FxGrow, highlights the importance of proximity:

"Minimizing the latency from our trading infrastructure to the bridge infrastructure is a huge selling point... This minimizes errors and latency with our traders."

New Trends in High-Frequency Trading (2026)

High-frequency trading (HFT) continues to evolve with cutting-edge technologies like artificial intelligence, modular microservices, and advanced failover systems. These advancements are reshaping how firms approach execution speed and system reliability in live trading environments.

Stay online and closer to execution. Choose a VPS location for CME futures, New York markets, London FX, API trading, and more.

Host your platform near the market route that matters.

From $59.99/mo

AI and Machine Learning in HFT

AI and machine learning have become indispensable tools in HFT, meeting the strict latency requirements of live trading. A notable example comes from November 2025, when Lynx Trading Technologies transitioned its AI workloads from the cloud to on-premises NVIDIA HGX B200 systems provided by Arc Compute. This shift eliminated cloud-induced delays, giving their researchers greater control over hardware performance. As a result, they could run larger models, generate more reliable signals, and cut long-term computing expenses.

Modern GPUs are game-changers, accelerating Monte Carlo risk calculations by 50 to 800 times compared to CPUs. AI inference latencies have dropped below 100 microseconds, making these models viable for strategies where every microsecond counts. Nive Mahalingam from Arc Compute highlights this trend:

Modern HFT increasingly relies on machine learning inference, including short term direction prediction, liquidity shifts, and volatility forecasts.

The JaxMARL-HFT framework is another breakthrough. By training agents on a year’s worth of Limit Order Book data (400 million orders), researchers achieved a 240× reduction in training time compared to earlier methods. Valentin Mohl and his team explain:

Leveraging JAX enables up to a 240x reduction in end-to-end training time, compared with state-of-the-art reference implementations on the same hardware.

Hybrid setups are also gaining traction. FPGAs handle nanosecond-critical tasks, while GPUs manage complex analytics. AMD's Versal series integrates AI engines directly into FPGA chips, enabling real-time inference alongside traditional logic. Arc Compute emphasizes the importance of speed:

Competitive edge now depends on who understands the data fastest, not only on who receives it first.

While AI optimizes decision-making, evolving system architectures ensure that execution remains seamless and efficient.

Microservices and Cloud Scaling

HFT firms are increasingly splitting their infrastructure into two distinct parts. The "hot path", responsible for execution and order routing, remains on physical hardware for ultra-low latency. Meanwhile, the "cold path", which handles research, backtesting, and historical data analysis, takes advantage of cloud-based scalability. This modular setup allows firms to update specific components - like exchange connectors or risk rules - without disrupting core operations.

Microservices isolate latency-sensitive processes from less critical functions. For instance, a firm can deploy a new FIX connector to a European exchange without restarting the entire trading system. This reduces risks during deployment and speeds up development cycles. However, the execution path stays on bare-metal hardware to avoid virtualization delays, as even minor jitters are unacceptable when microseconds matter.

Automated Failover and Disaster Recovery

Failover systems in 2026 focus on preserving the exact trading context during disruptions, rather than just switching to backup servers. John Murillo of B2BROKER explains:

What teams usually misunderstand is that failover in trading is not just about switching systems. It's about carrying over the exact trading context at the moment of failure.

This means maintaining open orders, partial fills, client exposure, and risk limits during a failover.

Modern active-active architectures achieve recovery times (RTO) under 60 seconds and zero data loss (RPO), ensuring uninterrupted operation and data integrity. Platforms aim for "five nines" (99.999%) uptime, translating to only five minutes of downtime annually.

Chaos Engineering now plays a crucial role in testing resilience against outages and cyber threats. Raft consensus algorithms synchronize data across multiple locations within 1 millisecond. Additionally, FPGA-based kill switches provide an extra layer of safety by instantly halting order flow, meeting MiFID II regulations that mandate trading stops within 5 seconds. Non-compliance with SEC Rule 613, which requires accurate audit trails, can lead to fines of up to $1 million per day.

| Metric | Target Requirement | Purpose |

|---|---|---|

| RTO (Recovery Time Objective) | < 60 Seconds | Maximum allowable offline time |

| RPO (Recovery Point Objective) | 0 Seconds | Maximum acceptable data loss |

| Failover Trigger | 50 Milliseconds | Speed of automated system switchover |

| Kill Switch Response | < 5 Seconds | Regulatory requirement under MiFID II |

Conclusion

The future of high-frequency trading (HFT) in 2026 hinges on reducing physical latency. The architecture, speed, and infrastructure decisions you make will determine whether your orders hit the exchange ahead of competitors or lag behind. Understanding every point of latency in your system is absolutely critical.

Investing in the right infrastructure directly impacts performance. Today, the competitive edge relies on consistent performance rather than just raw speed. For example, a stable 15µs path outperforms a faster 9µs path that suffers from jitter under load. This makes it essential to choose infrastructure that eliminates unpredictable delays. Technologies like kernel bypass, FPGA-driven execution, and proximity to exchange matching engines are key to achieving this. Nearly 75% of quantitative firms have reported disruptions during periods of high market volatility, highlighting the importance of maintaining stable latency even under stress.

For firms weighing infrastructure costs, balancing premium co-location with practical VPS solutions is crucial. Full co-location - where expenses for rack space, power, and cross-connects can run into thousands of dollars each month - isn't feasible for everyone. This is where QuantVPS offers a practical alternative. By hosting your trading engine on enterprise-grade infrastructure near exchange hubs, such as CME Aurora, you can bypass the instability of residential ISPs and reduce network hops. Transitioning from standard retail setups to optimized VPS solutions can significantly cut latency, which is critical when even a 10–20 ms delay can lead to missed trades.

HFT has evolved to demand both speed and reliability, with competition now measured in nanoseconds. Whether you're executing AI-driven strategies or cross-asset arbitrage, your infrastructure must deliver on both fronts. QuantVPS high-performance plans offer dedicated resources, DDoS protection, and 100% uptime guarantees - providing a cost-effective alternative to full co-location. The choices you make in architecture and infrastructure will ultimately shape your success in the market.

As Algotradingdesk aptly puts it:

In HFT, latency is not just speed - it is priority in order execution.

The first orders to hit the exchange are executed first, while slower orders face adverse selection. By optimizing your infrastructure with QuantVPS, you can ensure your orders consistently reach the front of the line when every microsecond counts.

FAQs

What latency should I target for my strategy?

For high-frequency trading (HFT) strategies in 2026, the goal is to achieve latency measured in nanoseconds to microseconds. Operating at nanosecond-level latency is seen as the standard for peak performance in this highly competitive arena.

When do FPGAs actually beat CPU-only trading?

FPGAs excel over CPU-only setups in trading environments where nanosecond-level latency is critical. By executing logic directly in hardware, they eliminate operating system and software delays. This enables them to send fully-formed, exchange-compliant order messages with incredible speed and minimal jitter. These qualities make FPGAs a perfect fit for ultra-low latency demands in high-frequency trading.

Is co-location worth it for smaller firms?

Co-location offers smaller firms in high-frequency trading (HFT) a chance to level the playing field, even though it's often linked with larger institutions. By positioning servers close to exchange data centers, firms can drastically cut down latency, enabling quicker trade execution. While the initial investment might seem steep, the advantages - such as accelerated execution speeds and cutting-edge optimizations like FPGA (Field-Programmable Gate Array) acceleration - can empower smaller players to stay competitive in the ultra-low latency trading landscape of 2026.