Tax-loss harvesting helps you reduce your tax bill by selling investments at a loss to offset capital gains. Here’s the key takeaway:

- Offset capital gains: Losses directly reduce taxable gains, dollar for dollar.

- Annual deduction: You can deduct up to $3,000 of excess losses against your ordinary income ($1,500 if married filing separately).

- Carryforward: Any unused losses roll into future years indefinitely.

To avoid IRS penalties, follow the wash-sale rule, which prevents claiming a loss if you buy a “substantially identical” asset within 30 days before or after the sale. Use strategies like Specific Identification (SpecID) to target shares with the highest losses for maximum savings.

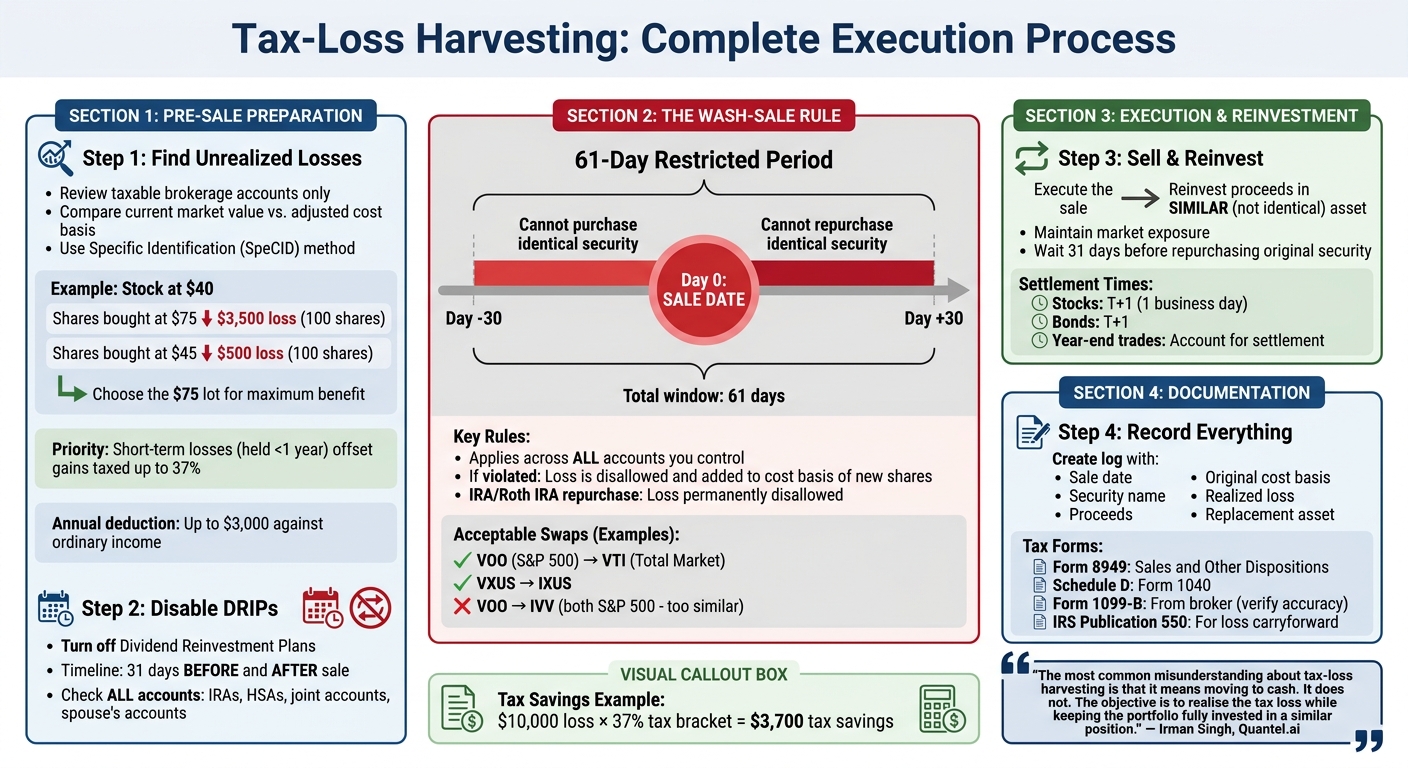

Why it matters: Tax-loss harvesting could boost after-tax returns by 0.5%–1.5% annually. For example, harvesting a $10,000 loss in the 37% tax bracket saves $3,700 in taxes. Reinvesting these savings over time can significantly grow your portfolio.

Automation tools and platforms like QuantVPS can streamline the process, ensuring compliance and efficiency while monitoring for opportunities throughout the year. Whether you’re offsetting short-term gains or carrying losses forward, this strategy is a powerful way to keep more of your investment returns.

IRS Rules and Compliance Requirements

Tax-loss harvesting comes with strict guidelines set by the IRS to prevent misuse. Being aware of these rules is crucial before making any trades.

The Wash-Sale Rule Explained

The wash-sale rule is designed to stop investors from claiming a loss on a security if they buy a "substantially identical" one within 30 days before or after the sale. This creates a 61-day restricted period. If a wash sale occurs, the disallowed loss is added to the cost basis of the replacement shares, delaying the tax benefit until you sell those shares. However, if the repurchase happens in an IRA or Roth IRA during this window, the loss is permanently disallowed and cannot be added to the account's basis.

This rule applies across all accounts under your control - taxable accounts, IRAs, HSAs, joint accounts, and even your spouse's accounts. To avoid triggering a wash sale, turn off Dividend Reinvestment Plans (DRIPs) at least 31 days before and after a planned harvest. If maintaining market exposure is important, consider switching to a "similar but not identical" asset. For example, selling an S&P 500 ETF like VOO and buying a Total Stock Market ETF like VTI is generally acceptable. However, swapping VOO for another S&P 500 ETF like IVV could violate the rule.

"The wash sale rule applies across all accounts you control, not just the one where the sale occurred. The IRS looks at you as an economic unit, not at individual accounts." - SmartFinance

Being aware of these restrictions helps you balance gains and losses more effectively.

Matching Short-Term and Long-Term Losses

The IRS has specific guidelines for offsetting gains and losses. Short-term losses (from assets held for one year or less) must first offset short-term gains, which are taxed at ordinary income rates - up to 37% starting in 2026. Long-term losses (from assets held for more than one year) must first offset long-term gains, which are taxed at lower rates of 0%, 15%, or 20%. If any losses remain, they can offset gains in the other category, a process known as cross-netting. Since short-term gains are taxed at higher rates, focusing on harvesting short-term losses can provide more immediate tax benefits.

With this framework in mind, traders can refine their strategies through careful share selection.

Specific Identification of Cost Basis

Maximizing tax savings often depends on selecting the right shares to sell. Instead of defaulting to your broker's method (usually First-In, First-Out), you can use the "Specific Identification" (SpecID) method. This allows you to choose which shares to sell, enabling you to target shares with the highest purchase price to realize larger losses. For example, selling 100 shares bought at $50 when the stock is at $25 results in a $2,500 loss, compared to just $500 if selling shares purchased at $30.

Notify your broker of your specific share selections before settlement, which is typically within one business day (T+1). Keeping detailed records of these selections - such as trade confirmations and screenshots - is essential for accurate tax filing.

"Reconcile all buys and sells across accounts before filing. Brokerage reporting is helpful - but not definitive." - Tax Specialty

How to Execute Tax-Loss Harvesting

Tax-Loss Harvesting Step-by-Step Process and Wash-Sale Rule Timeline

Finding Unrealized Losses in Your Portfolio

Start by reviewing your taxable brokerage accounts. Compare the current market value of each security to its adjusted cost basis to spot positions trading at a loss. Use the Specific Identification (SpecID) method to focus on tax lots with the highest purchase prices. For instance, if a stock is currently priced at $40, selling 100 shares purchased at $75 (resulting in a $3,500 loss) is generally more advantageous than selling 100 shares bought at $45 (resulting in only a $500 loss).

It’s smart to prioritize short-term losses - those from positions held for less than a year - since these can offset short-term gains, which may be taxed at rates as high as 37%. Additionally, you can apply up to $3,000 in net capital losses annually to reduce ordinary income ($1,500 if married filing separately). Once you’ve pinpointed these losses, the next step is to sell the positions and reinvest thoughtfully.

Selling Losses and Reinvesting in Different Assets

After identifying which positions to harvest, make sure to disable any Dividend Reinvestment Plans (DRIPs) for those securities at least 31 days before and after the sale. Also, check across all accounts you control - like IRAs, HSAs, joint accounts, and even your spouse's accounts - to confirm you haven’t purchased the same security within the last 30 days.

Once you execute the sale, reinvest the proceeds into a different, but similar, asset to maintain your market exposure. For example, you could swap an S&P 500 ETF like VOO for a Total Market ETF like VTI, or replace VXUS with IXUS. However, avoid repurchasing the same security or any substantially identical asset for the next 30 days to steer clear of a wash sale and complete the 61-day wash-sale window.

"The most common misunderstanding about tax-loss harvesting is that it means moving to cash. It does not. The objective is to realise the tax loss while keeping the portfolio fully invested in a similar position."

- Irman Singh, Author, Quantel.ai

This 31-day waiting period is crucial to ensure compliance with the wash-sale rule.

NEVER MISS A TRADE

Your algos run 24/7

even while you sleep.

99.999% uptime • Chicago, New York & London data centers • From $59.99/mo

Recording and Documenting Your Trades

Once your trades are complete, it’s essential to keep detailed records for tax purposes and future reference. Create a log that includes the sale date, security name, proceeds, original cost basis, realized loss, and the replacement asset. This information will be necessary when reporting transactions on Form 8949 (Sales and Other Dispositions of Capital Assets) and Schedule D (Form 1040).

Although your broker will provide a Form 1099-B summarizing annual sales, maintaining your own records is a smart way to verify accuracy and track wash sales across all accounts. If your net capital losses exceed the $3,000 annual deduction limit, use the carryforward worksheet in IRS Publication 550 to roll over excess losses into future tax years.

Finally, keep copies of trade confirmations and any related documentation. These records will be invaluable if the IRS ever questions your cost basis calculations. Having everything organized can save you a lot of headaches down the road.

Tax-Loss Harvesting for Algorithmic Traders

Algorithmic trading takes traditional tax-loss harvesting strategies to the next level, making the process more efficient and precise.

Asset Location Across Multiple Accounts

Where you hold your investments matters just as much as what you invest in. Taxable accounts are ideal for tax-efficient assets like index funds and ETFs, as they allow for tax-loss harvesting. On the other hand, tax-inefficient assets, such as REITs or actively managed funds with high turnover, are better suited for tax-advantaged accounts like IRAs or 401(k)s, where annual taxation is not an issue.

This kind of strategic asset placement not only increases your opportunities for harvesting losses but also reduces the tax burden from distributions outside your control. Your algorithm should track asset types and their locations to focus exclusively on taxable accounts when identifying positions for harvesting.

Automating Tax-Loss Harvesting with VPS Hosting

Using QuantVPS for automated tax-loss harvesting ensures constant monitoring, capturing intraday losses that manual reviews might miss. By scanning portfolios daily, automated systems can identify 2 to 4 times more harvestable losses compared to annual reviews. This can result in an additional 0.5% to 1.5% boost to after-tax annual returns.

Low-latency infrastructure plays a critical role here, allowing your algorithm to execute trades at the most advantageous times. For a portfolio worth $1,000,000, continuous harvesting could save you $15,000 to $25,000 annually in federal taxes during an average market year. To ensure trades settle within the same tax year, your algorithm needs to account for settlement times - T+2 for stocks and T+1 for bonds.

To maximize tax benefits, program your system to use Highest In, First Out (HIFO) lot selection, which targets shares with the largest unrealized losses. Additionally, maintaining correlation matrices helps the system choose replacement securities that align with your portfolio's risk profile while avoiding wash-sale violations.

By automating these processes, you can execute strategies quickly and accurately, even in volatile markets. However, setting clear loss thresholds becomes essential for effective implementation.

Setting Loss Thresholds and Review Schedules

Establishing precise triggers ensures the tax benefits outweigh transaction costs. For example, you could set thresholds at 5%–10% below the cost basis or use dollar-based minimums, like $500 per position.

Rather than limiting reviews to year-end, schedule them throughout the year to capture losses during market drawdowns. For instance, the S&P 500 typically experiences an average intraday drawdown of about 14% annually, offering harvesting opportunities nearly every quarter, regardless of overall year-end performance.

Your algorithm should prioritize short-term losses - those from positions held under a year - since they offset short-term gains, which are taxed at rates as high as 37% starting in 2026. Make sure your system enforces wash-sale rules across all linked accounts, including those held by spouses or in IRAs.

Software and Tools for Tax Optimization

Using software can turn sporadic tax-loss harvesting into a consistent and efficient process. The right tools should track cost basis at the lot level, not just overall positions, to pinpoint shares with potential harvestable losses. Additionally, it’s crucial that your software monitors wash-sale risks across all account types.

Portfolio Management Software

Modern portfolio management tools come packed with features to simplify tax optimization. For example, PortfolioPilot users collectively saved $93 million on taxes in 2025 through automated strategies, with subscription plans starting at $20/month. Similarly, TaxHarvest reports that its customers save an average of $30,000 annually, offering plans starting at $399/month, which include unlimited harvesting and wash-sale alerts.

Key features to look for include real-time tax liability estimates and "what-if" scenario tools for testing different trade outcomes. Interactive Brokers' Tax Optimizer lets users experiment with various matching methods - like FIFO, LIFO, or Highest Cost - to determine the best tax outcome for specific trades. For those managing positions across multiple brokerages, TradeLog is a standout option. It imports transaction histories from over 30 brokers and generates IRS-ready Form 8949 and Schedule D reports, with pricing starting around $218/year.

Automating replacement security suggestions can make trade execution faster and easier. Platforms like TaxHarvest.ai suggest alternative securities that maintain market exposure while avoiding wash-sale violations during the crucial 30-day window. Clarity, another platform, offers unified FIFO cost basis tracking and cross-account wash-sale detection. One satisfied user shared:

"I was paying taxes on gains I could have offset with losses. Clarity showed me $22K in harvestable losses across my accounts. That's real money I almost left on the table." - Nathan P., Active Investor

These tools not only simplify the process but also integrate with automated strategies to improve overall tax efficiency.

Running Tax-Loss Algorithms on QuantVPS

For algorithmic tax-loss harvesting, you need infrastructure that can handle continuous, uninterrupted monitoring. QuantVPS offers a high-performance environment tailored for platforms like NinjaTrader and TradeStation. Their pricing starts at $99.99/month (or $69.99/month if billed annually) for the VPS Pro plan, which includes 6 cores and 16GB RAM. For more intensive needs, the Dedicated Server plan costs $299.99/month (or $209.99/month annually) and provides 16+ dedicated cores and 128GB RAM.

This high-performance infrastructure ensures your algorithms can quickly identify and execute optimal trades. Running 24/7, these algorithms monitor for "structure breaks" or "divergence triggers" - signals for harvesting opportunities during intraday market volatility that manual reviews might miss. With a 100% uptime guarantee and strong DDoS protection, your harvesting scripts remain active even during periods of market turbulence, directly supporting the tax-loss harvesting strategies discussed earlier.

STOP LOSING TO LATENCY

Execute faster than

your competition.

Sub-millisecond execution • Direct exchange connectivity • From $59.99/mo

Tax-Loss Harvesting Examples

These examples show how traders can use tax-loss harvesting to lower their federal tax bills, complete with specific figures and outcomes.

Offsetting Short-Term Gains with Short-Term Losses

Short-term capital gains, which come from assets held for one year or less, are taxed at ordinary income rates - up to 37% for high earners. This makes offsetting short-term gains with losses particularly impactful.

Take Sarah in 2026, a single filer in the 32% federal tax bracket with $200,000 in taxable income. She realized $25,000 in short-term gains from tech stocks and $15,000 in long-term gains. By harvesting $25,000 in losses from stocks and cryptocurrency positions (leveraging the 2026 crypto wash-sale exemption), she completely offset her short-term gains. This reduced her federal tax bill from $10,250 to $2,250, saving her $8,000 in taxes.

| Without Harvesting | With Harvesting | Savings |

|---|---|---|

| Short-term gains: $25,000 @ 32% | $0 | $8,000+ |

| Long-term gains: $15,000 @ 15% | $15,000 @ 15% | $0 |

| Total federal tax: $10,250 | $2,250 | $8,000 |

The takeaway? Focus on harvesting short-term losses first, as they offset higher-taxed gains.

Now, let’s look at how exceeding loss limits can provide additional benefits.

Deducting Excess Losses from Ordinary Income

If your total capital losses surpass your gains, you can deduct up to $3,000 ($1,500 if married filing separately) from ordinary income, such as wages or interest. Any leftover losses can be carried forward to future tax years indefinitely.

For example, an investor in the 24% tax bracket with $12,000 in capital losses and no gains deducts $3,000, saving $720 immediately, while carrying forward the remaining $9,000. The savings grow with higher tax brackets: a 37% bracket investor saves $1,110 by deducting $3,000, while a 22% bracket investor saves $660. Reinvesting these annual tax savings - say $3,000 at a 10% return - can grow to about $189,842 over 20 years.

"The 'boring' $3K/year tax harvest can be worth over half a million." - InvestToFire

Next, let’s explore how long-short strategies can maximize tax efficiency.

Tax Efficiency in Long-Short Equity Strategies

Long-short equity strategies involve frequent trading, often generating short-term gains taxed at ordinary income rates. Even in market-neutral portfolios, the varying performance of individual stocks creates opportunities to harvest losses throughout the year.

In 2026, Emily used this approach by selling a retail ETF for an $8,000 loss, which she applied to offset a $15,000 gain from tech stocks. This lowered her taxable gain to $7,000, cutting her tax bill from $3,000 to $1,400 - a $1,600 savings. She reinvested the proceeds into a consumer discretionary ETF, maintaining her sector exposure and avoiding the wash-sale rule.

Monthly optimization in long-short strategies can increase annual returns by up to 1.94%. Similarly, direct indexing strategies - which allow for harvesting losses in individual stocks even when the overall index gains - can harvest 1.9 to 2.1 times more losses over a decade compared to ETF-based strategies.

These examples highlight the power of algorithmic tools in spotting tax-loss harvesting opportunities. For traders using algorithmic systems, platforms like QuantVPS can help identify and execute these opportunities during intraday market fluctuations, something manual reviews might miss.

Conclusion

Tax-loss harvesting isn't just a once-a-year task - it’s an ongoing strategy that can boost after-tax returns by 0.5% to 1.5% annually when applied consistently and thoughtfully. To make the most of it, focus on staying compliant with IRS rules, plan carefully, and use effective tools to seize opportunities as they arise.

Compliance is non-negotiable. Adhering to the wash-sale rule across all accounts is crucial. Using Specific Identification for selecting tax lots can maximize efficiency, and keeping up with changing regulations - like the new digital asset reporting rules set for 2026 - is essential. By mastering these compliance basics, you can turn tax-loss harvesting into a powerful part of your investment strategy.

Frequent reviews make a difference. Regular portfolio monitoring uncovers 2 to 4 times more harvestable losses compared to annual reviews, especially during market shifts like corrections or sector rotations. For algorithmic traders, platforms like QuantVPS provide 24/7 infrastructure, enabling automated tax-loss harvesting that captures intraday market moves that manual reviews may overlook.

The benefits are clear. For example, a $3,000 annual deduction reinvested at a 10% return can grow to over $542,000 in 30 years. And for those in higher tax brackets, a $10,000 loss could lead to immediate federal tax savings of up to $3,700. Whether you're managing long-short equity strategies or customized portfolios, combining discipline with automation can turn tax-loss harvesting from a routine task into a real competitive advantage.

FAQs

What counts as a “substantially identical” investment for wash-sale rules?

Under wash-sale rules, a “substantially identical” investment generally refers to securities that are nearly the same in nature. This could include different shares of the same company or closely related options, as they are treated as equivalent for tax purposes. Since interpretations can vary, it’s a good idea to check the IRS guidelines or consult a tax professional to ensure you understand how this applies to your specific situation.

How do I avoid wash sales across my IRA, taxable, and my spouse’s accounts?

To steer clear of wash sales, make sure you don’t buy identical or substantially identical securities within 30 days before or after selling them at a loss. This rule applies across all accounts, including IRAs and your spouse’s accounts, so it’s important to coordinate trades carefully. If you want to maintain market exposure, consider alternatives like different ETFs or sector funds instead. Lastly, keep thorough records of all transactions to stay compliant and adjust your cost basis correctly when necessary.

When is tax-loss harvesting not worth it because of fees or bid-ask spreads?

Tax-loss harvesting can lose its appeal if the costs associated with trading - like fees or bid-ask spreads - outweigh the tax advantages. This is particularly relevant for smaller portfolios or strategies that involve high transaction costs, as these expenses can eat into, or even cancel out, the savings gained from offsetting capital gains.