Slippage is the difference between the price you expect when placing a trade and the actual price at execution. While it may seem minor, slippage can quietly erode your profits over time, especially in fast-moving or low-liquidity markets. For traders, understanding and minimizing slippage is critical to protecting returns.

Key Takeaways:

-

Causes of Slippage:

- Market volatility (e.g., during economic announcements).

- Low liquidity (fewer buyers/sellers in the market).

- Execution delays (latency between order placement and execution).

-

Impact:

- Even small slippage adds up, costing thousands annually for active traders.

- High-frequency traders face sharper losses due to execution delays.

How to Reduce Slippage:

- Use Limit Orders: Control the price you’re willing to accept.

- Trade During High Liquidity Hours: For forex, the London–New York overlap (8:00 AM–12:00 PM ET) offers tighter spreads.

- Split Large Orders: Break big trades into smaller parts to avoid price shifts.

- Upgrade Infrastructure: Using a VPS like QuantVPS can reduce latency, improving execution speed.

Slippage is an unavoidable cost, but with the right strategies, you can minimize its impact and keep more of your profits intact.

What Causes Slippage in Financial Markets

Understanding what triggers slippage is essential for anticipating when it’s most likely to happen and minimizing hidden costs. Slippage occurs when there’s a difference between the price you expect and the actual execution price of your order. This gap is influenced by three main factors: market conditions, trade size, and execution speed. Let’s break these down.

Market Volatility and Low Liquidity

Sharp price swings are a major driver of slippage, especially during significant economic events. For instance, announcements like the Federal Reserve’s interest rate decisions or the release of the Non-Farm Payroll (NFP) report can cause prices to "gap" in milliseconds. Imagine targeting $50.25 for an order, but by the time it executes, the market has already moved to $50.32.

Low liquidity also plays a role, particularly during off-peak trading hours, such as the Asian session overlap or the daily market rollover at 5:00 PM EST. During these periods, there are fewer participants in the market, which means fewer buyers and sellers to match orders. Liquidity providers often withdraw during uncertain times, further thinning the order book. This lack of depth can lead to spreads on less-traded currency pairs widening significantly - sometimes by as much as 500% during rollover periods.

But market conditions aren’t the only factor. The size of your trade also has a direct impact on execution quality.

Order Size and Market Depth

The larger your trade, the more likely it is to encounter slippage. Why? Large orders can quickly deplete the available volume at the best price. Once that happens, the system starts filling the remainder of your order at progressively less favorable prices. For example, in a 100-lot order, the first 20 lots might execute at your target price, but the remaining 80 could fill at higher prices as liquidity thins out.

"Large institutional orders frequently exhaust the liquidity available at the best bid or offer." - Alexander Shishkanov, Writer, B2Broker

Run 24/7 while you sleep. Keep bots, platforms, and trade copiers online on a dedicated VPS.

Low-latency VPS hosting for your trading platform.

From $59.99/mo

This phenomenon is explained by the square-root law of market impact: doubling the size of your trade doesn’t double the slippage - it increases it by roughly 1.41 times. For institutional traders, this market impact can account for 60% to 80% of total transaction costs. Even smaller, retail traders can cause noticeable price shifts in markets with low trading volume.

Finally, the speed at which your order reaches the market plays a crucial role in slippage.

Execution Speed and Latency Issues

Delays in order execution create opportunities for the market to move against you. A typical home internet connection introduces 50 to 200 milliseconds of latency between your system and the broker’s servers. While this might seem trivial, in fast-moving markets, it’s enough time for prices to shift by several pips.

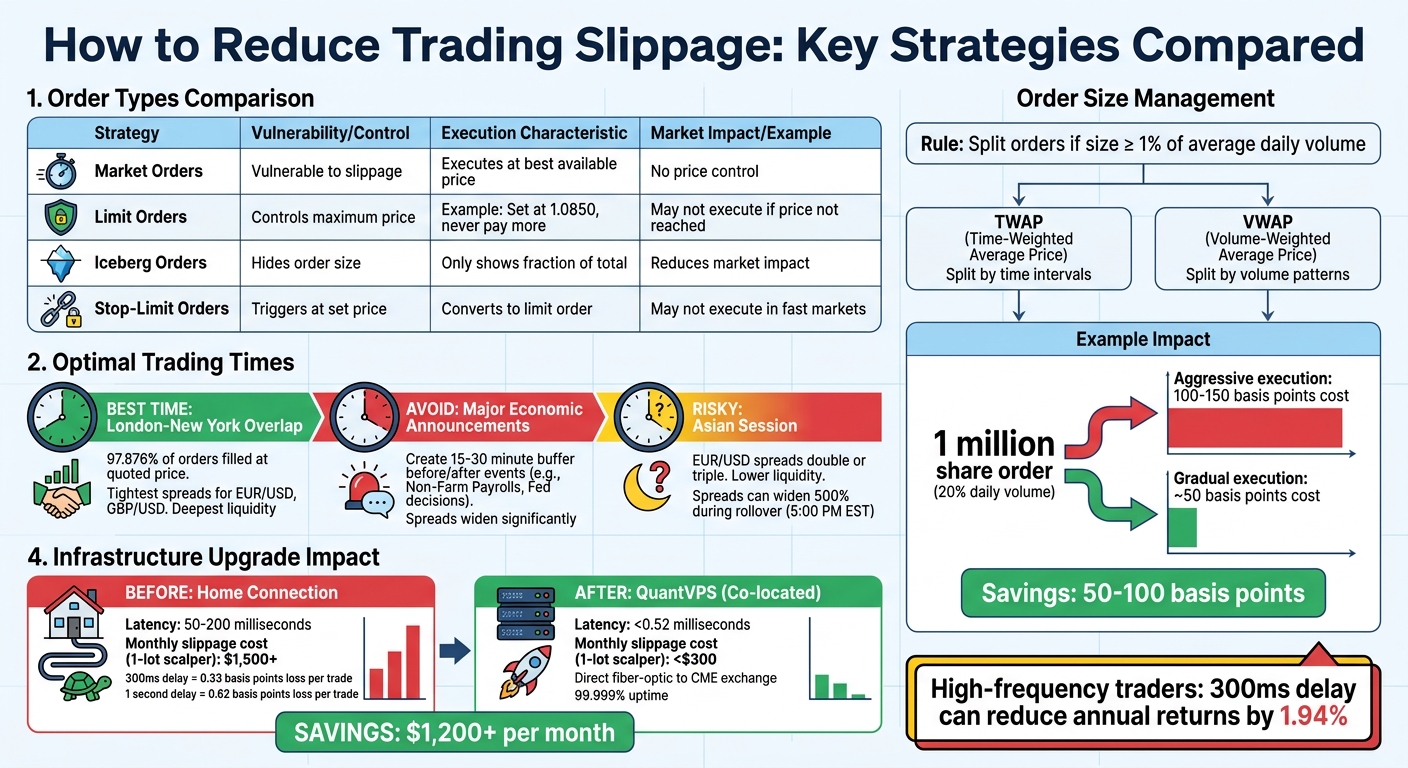

For traders with a 70% success rate in predicting market direction, a 300-millisecond delay can reduce returns by 0.33 basis points per trade. Stretching that delay to one second nearly doubles the loss to 0.62 basis points. For high-frequency trading strategies, even a 300-millisecond delay can erode annual returns by as much as 1.94%. The longer your order takes to execute, the higher the risk of being filled at an outdated and less favorable price.

How to Reduce Trading Slippage

Trading Slippage Reduction Strategies: Order Types, Timing, and Infrastructure Comparison

Understanding market volatility, order size, and execution speed is just the beginning. To minimize slippage and avoid hidden costs, you can apply these practical strategies.

Choose the Right Order Types

Using the right order type can make a big difference in controlling slippage. Limit orders, for example, allow you to set a specific price you're willing to accept, unlike market orders that execute at the best available price. If you place a limit order at 1.0850, you'll never pay more than that price, though it might not execute if the market doesn't reach your set level.

"Market orders are particularly vulnerable to slippage because they are executed at the best available price at the time of execution."

– Brady Young, Marketing Specialist, LuxAlgo

For larger positions, iceberg orders can help. They only display a fraction of your total order, reducing the chance of moving the market. Stop-limit orders are another option, offering a mix of price control and execution flexibility. These orders turn into limit orders when your trigger price is hit, though they might not execute during fast-moving markets.

Choosing the right order type gives you more control and helps you navigate changing market conditions effectively.

Trade During High Liquidity Periods

Timing your trades to align with high liquidity periods is another way to reduce slippage. The London–New York overlap (8:00 AM–12:00 PM ET) is an ideal time for trading forex majors like EUR/USD and GBP/USD because of tighter spreads and deeper liquidity. For example, CMC Markets reported that as of August 31, 2023, 97.876% of market-open orders were filled at the quoted price under normal conditions.

On the flip side, avoid trading during major economic announcements. Spreads can widen significantly around events like Non-Farm Payrolls or Federal Reserve decisions, so it's wise to create a 15- to 30-minute buffer before and after these events. Similarly, trading during the Asian session can be riskier, as spreads for pairs like EUR/USD often double or triple compared to peak liquidity hours.

By combining smart timing with careful order management, you can minimize unnecessary risks.

Split Large Orders into Smaller Trades

Large orders can cause slippage by eating into available liquidity and pushing prices against you. If your order size is close to or exceeds 1% of a stock's average daily volume, consider breaking it into smaller trades. Using strategies like TWAP (Time-Weighted Average Price) or VWAP (Volume-Weighted Average Price) can help. These methods split large orders into smaller portions based on time intervals or trading volume patterns, reducing the market impact.

For instance, executing a sell order of 1 million shares - about 20% of a US large-cap stock's daily volume - could lead to execution costs ranging from 50 to 150 basis points, depending on how aggressively you trade. By splitting the order and trading more gradually, you can lower costs, potentially keeping them closer to the 50-basis-point range.

Breaking down large trades into smaller, more manageable chunks can significantly reduce slippage and save on transaction costs in the long run.

Using QuantVPS to Lower Latency and Reduce Slippage

When it comes to trading, even the smallest delays can make a big difference. A few milliseconds could mean the difference between hitting your target price or dealing with slippage. That’s why having the right infrastructure is so important - specifically, how close your trading server is to the exchange and how efficiently it processes orders.

How VPS Hosting Speeds Up Execution

Local setups often struggle with execution delays. QuantVPS solves this by operating datacenters in Chicago and New York. Their Chicago facility is located right next to the CME Group’s matching engines, drastically reducing network travel time. Using direct fiber-optic cross-connects to the CME Group exchange, QuantVPS eliminates unnecessary network hops to minimize data latency.

"Our Chicago datacenter provides ultra‐low latency (<0.52ms) directly to the CME exchange, enabling faster futures trade execution and significantly minimizing slippage." - QuantVPS

QuantVPS servers are equipped with enterprise-grade processors, high-speed memory, and NVMe SSDs to ensure there are no processing bottlenecks. With a 99.999% uptime SLA, your automated strategies and bots can run continuously - even when your local computer is turned off. The network infrastructure supports speeds of 1Gbps or higher, with the ability to burst up to 10Gbps during periods of high market activity.

Stay online and closer to execution. Choose a VPS location for CME futures, New York markets, London FX, API trading, and more.

Host your platform near the market route that matters.

From $59.99/mo

By reducing delays, QuantVPS tackles slippage head-on, helping traders protect their profits from hidden costs. This advanced setup is crucial for maintaining efficiency and reducing the impact of latency on trading outcomes.

Each server comes pre-installed with Windows Server 2022 and is optimized for popular trading platforms. You can securely manage your strategies via remote desktop access from any device - whether you’re using Windows, Mac, iOS, or Android - while the VPS handles the heavy lifting for you. QuantVPS offers a range of plans designed to suit various trading needs.

QuantVPS Plans and Pricing

QuantVPS provides four main plans, each tailored to meet specific trading requirements. The VPS Lite plan starts at $59.99 per month, ideal for traders running one or two charts or strategies. At the higher end, the Dedicated plan costs $299.99 per month and supports six or more charts, as well as extensive backtesting. These plans are designed to give traders the flexibility to choose the right balance of performance and cost.

| Plan | Price | CPU | RAM | Storage | Best For |

|---|---|---|---|---|---|

| VPS Lite | $59.99/mo | 4x AMD EPYC Cores | 8GB DDR4 | 75GB NVMe | 1–2 charts/strategies |

| VPS Pro | $99.99/mo | 6x AMD EPYC Cores | 16GB DDR4 | 150GB NVMe | 3–4 charts; simple backtesting |

| VPS Ultra | $189.99/mo | 12x AMD EPYC Cores | 32GB DDR4 | 300GB NVMe | 5+ charts; moderate backtesting |

| Dedicated | $299.99/mo | 12x+ AMD Ryzen Cores | 128GB DDR4 | 1TB NVMe | 6+ charts; extensive backtesting |

Each plan includes a dedicated IP address, unmetered bandwidth, enterprise-grade DDoS protection, and 24/7 customer support. You can start with a lower-tier plan and upgrade as your trading needs grow. Upgrades are processed instantly with prorated billing, ensuring no data loss during the transition.

Tracking and Improving Your Execution Performance

Reducing slippage isn't a one-and-done task - it demands constant monitoring and tweaking to safeguard your trading profits. Many traders find that the gap between their backtested results and live performance often comes down to underestimating slippage. By carefully tracking and analyzing this, you can fine-tune your strategy through more informed backtesting.

How to Measure Slippage in Your Trades

Start by logging accurate timestamps for every step in the order process: when your strategy generates a signal, when you submit the order, when your broker receives it, when the exchange acknowledges it, and when it finally executes. This level of detail helps you pinpoint where delays or inefficiencies might be happening.

Then, compare your fill prices against specific benchmarks. Here are a few to consider:

- Arrival Price: Tracks the mid-price at the time you submit your order, showing market movement during transit.

- Mid-Price Slippage: Measures the difference between your fill price and the midpoint of the best bid/offer at execution.

- VWAP Slippage: Compares your fill price to the volume-weighted average price over your execution window.

Each of these benchmarks highlights different aspects of your trading costs.

Don't stop at averages - they can hide critical details. Instead, use tools like histograms and box plots to visualize slippage distributions and uncover outliers. Break down your data by factors like asset class, order size, trading time, and market volatility. For instance, you might notice that slippage tends to spike during periods of low liquidity.

Using Backtesting to Refine Your Strategy

Once you've measured slippage, use that data to improve your backtesting process. Incorporate realistic slippage assumptions, such as modeling it as a percentage of the Average True Range (ATR). For example, estimating slippage at 5% of ATR can better reflect higher costs during volatile markets. For exit orders, consider applying even higher estimates - 1.5 to 2 times your entry slippage - to account for the added pressure on fills.

To test how robust your strategy is, run stress tests with slippage set at 2x or even 3x your normal estimates. A strategy that stays profitable under these conditions is more likely to hold up in real-world trading. Keep in mind that even tiny slippage - like 0.027% per trade - can add up fast. If you're aiming for 25% annual returns across 400 trades a year, that small percentage could eat up as much as 43% of your profits.

Conclusion

Slippage is an unavoidable cost in electronic order execution. Knowing what causes it and taking practical steps to minimize its effects can make all the difference between turning a profit or taking a loss.

This issue can significantly eat into returns - sometimes by as much as 1.94% annually for high-frequency strategies, with transaction costs consuming 3–5% or more of total returns.

To address slippage effectively, consider adopting specific strategies. Use limit orders to maintain control over execution prices and aim to trade during peak liquidity hours, such as the London–New York overlap from 8:00 AM to 12:00 PM EST. Breaking large orders into smaller portions can help reduce market impact, and setting realistic slippage tolerance levels - usually between 0.3% and 0.5% under normal conditions - can further manage risk.

Investing in better infrastructure can also lower latency and reduce slippage. For instance, upgrading from a home connection to a co-located VPS can dramatically cut monthly slippage costs for a 1-lot scalper - from over $1,500 to under $300. QuantVPS offers plans starting at $59.99 per month, delivering low and ultra-low latencies as low as 0.52 ms, dedicated resources, and a 99.999% uptime guarantee, ensuring your strategies stay operational around the clock.

FAQs

How much slippage is too much?

Slippage levels can vary depending on market conditions. Generally, a slippage rate between 0.3% and 0.5% is considered manageable under normal circumstances. However, when slippage exceeds 10%, it’s often seen as excessive, potentially leading to higher costs or even order cancellations. To reduce the impact of slippage, it’s essential to refine your trading strategy and improve your execution methods.

What’s the best way to estimate slippage in backtests?

To estimate slippage accurately in backtests, it's crucial to model it in a way that mirrors real-world conditions. This means factoring in latency slippage - the delays between identifying a signal and executing an order - and liquidity slippage, which arises due to market conditions, particularly with large orders or during periods of high volatility. Using variable slippage models that adjust based on trading volumes and market dynamics can help create more realistic simulations. Avoid assuming perfect order fills to better reflect actual trading costs.

Is a trading VPS worth it for reducing slippage?

A trading VPS can be a game-changer when it comes to reducing slippage. By improving execution speed and cutting down on latency, it helps traders avoid hidden costs and boosts overall performance. Faster, more reliable order execution means you’re less likely to miss out on profits or face unexpected losses due to delays.