Crude Oil (CL) futures are contracts traded on NYMEX that represent 1,000 barrels of West Texas Intermediate (WTI) crude oil. These contracts are key for traders managing risk or speculating in the energy market. Here’s what you need to know:

- Contract Size: 1,000 barrels of WTI crude oil.

- Tick Size: $0.01 per barrel, equal to $10.00 per contract.

- Margin Requirements: $2,000 for day trading, $4,132 for overnight positions (as of March 2026).

- Trading Hours: Nearly 24/5 on CME Globex, with a daily break from 4:00 p.m. to 5:00 p.m. CT.

- Settlement: Physical delivery in Cushing, Oklahoma, unless positions are closed before expiration.

Smaller traders can opt for Micro WTI (MCL) contracts, which represent 100 barrels with a $1.00 tick value, offering lower margin requirements and reduced exposure. Success in CL trading depends on understanding contract specs, managing risk, and using tools like stop-loss orders and reliable trading platforms.

CL Futures Contract Specifications

This section breaks down the essential details of CL futures, providing a clear understanding of how these contracts work and the risks involved. Each CL futures contract on the New York Mercantile Exchange (NYMEX) - a division of CME Group - represents 1,000 U.S. barrels of West Texas Intermediate (WTI) crude oil. This standard size means even small price changes can lead to significant financial impacts. For instance, a $1.00 price change results in a $1,000 movement in contract value. Even a modest $0.30 shift during a volatile session translates to a $300 gain or loss per contract.

Contract Size and Trading Unit

The 1,000-barrel contract size determines your exposure and risk. Futures trading uses leverage, allowing you to control the full value of the contract with only a fraction of its cost. This amplifies both potential gains and losses. For traders seeking reduced exposure, the Micro WTI Crude Oil (MCL) contract offers a smaller alternative, representing just 100 barrels - or one-tenth the size of the standard CL contract.

Tick Size and Minimum Price Fluctuation

The smallest price movement, known as the tick size, is $0.01 per barrel, equating to a $10.00 tick value per contract (1,000 barrels x $0.01). Even tiny price shifts can significantly impact your position, especially during volatile periods. To calculate your dollar risk, multiply the number of ticks by $10 when setting stop-loss orders. High-volatility events, like the EIA Weekly Petroleum Status Report (released Wednesdays at 10:30 a.m. ET), can cause slippage that exceeds several ticks in mere seconds.

"In CL, slippage is not just 'a few ticks' - it can expand rapidly during energy headlines and inventory releases. Always factor realistic execution costs into your targets and stops." – Richard O. Zamora III, CMT, Founder & Principal, Global Market Raiders LLC

Understanding these price increments is crucial, as they directly influence contract value changes.

Contract Value and Point Value

For standard CL contracts, a one-point move (equivalent to a $1.00 price change) results in a $1,000 profit or loss. On the other hand, the Micro WTI contract moves by $100 per point, making it a better fit for traders who prefer smaller positions. To determine the total value of a contract, multiply the current oil price by 1,000 barrels. For example, if crude oil is trading at $75.00 per barrel, the contract controls $75,000 worth of oil. This calculation highlights how even minor price changes can have a big impact on your portfolio.

Trading Hours and Exchange Details

CL futures trade electronically on CME Globex almost 24 hours a day, five days a week. Trading begins on Sunday at 5:00 p.m. CT and runs through Friday at 4:00 p.m. CT, with a one-hour daily break between 4:00 p.m. and 5:00 p.m. CT. This schedule gives traders the flexibility to react to global energy developments. The daily settlement price is determined during a two-minute window from 2:28 p.m. to 2:30 p.m. ET.

| Trading Venue | Days | Trading Hours (Central Time) |

|---|---|---|

| CME Globex | Sunday - Friday | 5:00 p.m. – 4:00 p.m. (with a 60-minute daily break) |

| TAS (Trading at Settlement) | Sunday - Friday | 5:00 p.m. – 1:30 p.m. |

| CME ClearPort | Sunday - Friday | 5:00 p.m. Sunday – 4:00 p.m. Friday (no reporting 4-5 p.m. Mon-Thu) |

These extended hours allow traders to manage positions and respond to the rapid value changes typical of CL futures.

Expiration and Settlement Procedures

CL futures are physically deliverable contracts, meaning they can settle through the delivery of crude oil to designated pipeline or storage facilities in Cushing, Oklahoma. Trading for a contract stops three business days before the 25th calendar day of the month preceding the contract month. Most retail traders close their positions before expiration to avoid the obligation of physical delivery. Since each CL contract represents approximately 42,000 gallons of crude oil, it’s essential to monitor contract month selection and roll timing carefully to avoid unintended delivery obligations.

Margin Requirements for CL Futures

Understanding margin requirements is a cornerstone of managing risk and developing trading strategies in CL futures. Margin serves as a performance bond - a deposit that ensures traders can meet their obligations. Unlike a down payment, margin doesn't grant ownership. Instead, it allows traders to control a much larger position, amplifying both potential gains and losses.

Initial and Maintenance Margins

When trading CL futures, two types of margin come into play: initial margin and maintenance margin. The initial margin is the amount required to open a position, which, as of March 2026, is around $4,132 for a standard CL contract. The maintenance margin, on the other hand, is the minimum balance needed to keep the position open - currently about $3,829.69. If your account balance dips below this level due to market movements, your broker will issue a margin call, requiring you to deposit more funds or risk having your position liquidated.

"Think of margin requirements as a performance bond. The dollar amount you must have available in your account in order to trade one particular commodity futures contract." – Insignia Futures

Margin requirements can change based on factors like market volatility, geopolitical events, or disruptions in supply. For instance, as of March 19, 2026, the maintenance margin for the April 2026 CL contract is $10,776 for long positions and $11,030 for short positions, while the December 2026 contract requires just $6,462 for long positions. Shorter-term contracts often demand higher margins due to increased volatility and liquidity concerns.

NEVER MISS A TRADE

Your algos run 24/7

even while you sleep.

99.999% uptime • Chicago, New York, London & more data centers • From $59.99/mo

Day trading margins, in contrast, are much lower, ranging from $1,000 to $2,000 per contract. However, these reduced margins apply only if you close your position before the trading session ends. Otherwise, your broker will require the full initial margin, potentially triggering a margin call if your account lacks sufficient funds.

Next, we’ll explore how margin requirements vary across different contract sizes, offering flexibility for traders with varying account sizes and risk preferences.

Margin Variations Across Contract Sizes

CL futures offer multiple contract sizes, catering to traders with different risk appetites and account balances. For smaller accounts, the Micro WTI Crude Oil (MCL) contract is a popular choice. It represents 100 barrels of crude oil and requires just one-tenth the margin of a standard CL contract. The E-mini WTI (QM) contract, representing 500 barrels, provides a middle ground between the Micro MCL and the standard CL contract.

| Contract Type | Contract Size | Tick Value | Day Trading Margin (Approx.) | Maintenance Margin (Mar 2026) |

|---|---|---|---|---|

| Standard CL | 1,000 Barrels | $10.00 | $2,000 | $10,776 |

| E-mini QM | 500 Barrels | $12.50 (per 0.025) | Varies | Varies |

| Micro MCL | 100 Barrels | $1.00 | ~$200 | ~$1,077 |

Individual brokers may also set house margin requirements that are higher than exchange minimums to protect against extreme market swings. To avoid forced liquidation during volatile periods - such as the release of the EIA Weekly Petroleum Status Report every Wednesday at 10:30 a.m. ET - it’s wise to maintain a cushion above the maintenance margin.

These margin requirements are critical for managing exposure effectively in the fast-moving and unpredictable CL futures market.

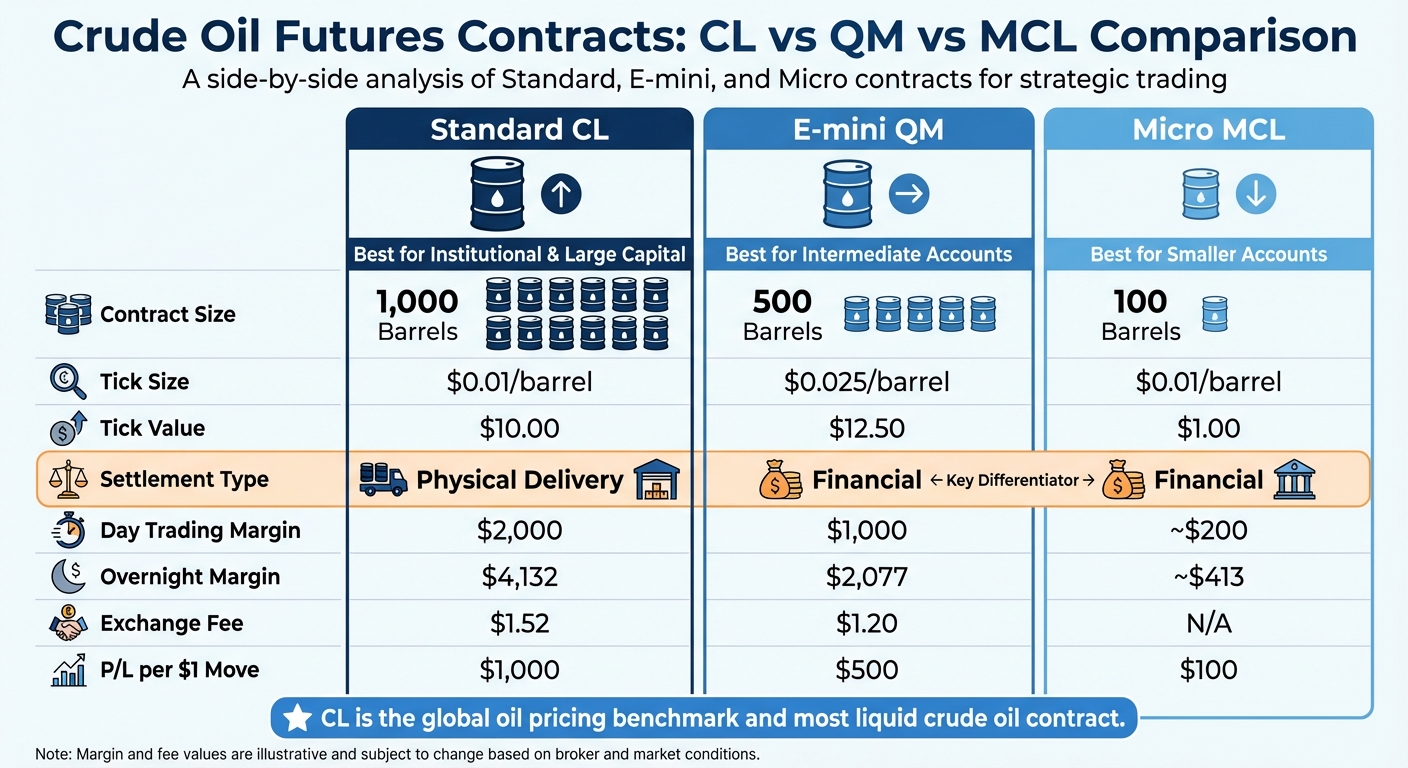

Crude Oil Contracts Comparison

CL vs QM vs MCL Crude Oil Futures Contract Comparison

CME Group offers three crude oil futures contracts - standard CL, E-mini QM, and Micro MCL - designed to meet different risk appetites and account sizes. The standard CL contract is the global oil pricing benchmark and the most liquid crude oil contract in the market. However, its size of 1,000 barrels can be challenging for smaller accounts, leading to the creation of the E-mini (QM) and Micro (MCL) contracts.

The E-mini QM contract is half the size of the standard CL at 500 barrels, while the Micro MCL represents 100 barrels. A major distinction lies in settlement: the standard CL involves physical delivery, while QM and MCL are settled financially. Understanding these differences can help you select the contract that aligns with your trading strategy.

Though the QM contract is half the size of the CL, its tick value is higher at $12.50 due to a minimum price change of $0.025 per barrel, compared to the CL’s $10.00 tick value with a $0.01 price change. The MCL, on the other hand, shares the same $0.01 tick size as the CL but has a much smaller tick value of $1.00. These variations directly impact profit/loss calculations and margin requirements, highlighting the importance of choosing the right contract for your trading needs.

Comparison Table

Here’s a breakdown of the key differences between the three contracts:

| Feature | Standard CL | E-mini QM | Micro MCL |

|---|---|---|---|

| Contract Size | 1,000 Barrels | 500 Barrels | 100 Barrels |

| Tick Size | $0.01/barrel | $0.025/barrel | $0.01/barrel |

| Tick Value | $10.00 | $12.50 | $1.00 |

| Settlement Type | Physical Delivery | Financial | Financial |

| Day Trading Margin | $2,000 | $1,000 | ~$200 |

| Overnight Margin | $4,132 | $2,077 | ~$413 |

| Exchange Fee | $1.52 | $1.20 | N/A |

For every $1.00 price movement, the profit or loss equates to $1,000 for CL, $500 for QM, and $100 for MCL. This flexibility allows traders to scale their exposure based on their risk tolerance and account size.

How to Trade CL Futures: Strategies and Risk Management

Navigating the CL futures market requires a mix of smart strategies and careful risk management. Crude oil futures behave differently from equity indices, reacting sharply to changes in supply and demand. For example, trend-following strategies often thrive during geopolitical events or OPEC decisions, which can drive extended price movements. Similarly, breakout trading can capture swift price shifts when key support or resistance levels are breached on heavy volume. Just keep in mind that this approach comes with heightened volatility.

Trading Strategies for CL Futures

Mean reversion strategies focus on short-term market overreactions. One tested method is to buy on Tuesdays or Thursdays when the closing price drops significantly below the previous day's range. Another approach is spread trading, which allows you to profit from price differences. This could involve trading the spread between Brent and WTI crude, using calendar spreads (long-dated versus near-dated contracts), or trading crack spreads - essentially the price difference between crude oil and refined products like gasoline.

Seasonal trends also play a role. Crude oil prices often hit their highest levels in December and January due to winter heating demand, while they tend to dip during the summer. However, summer driving season can sometimes cause unexpected price spikes. The best trading hours are typically between 8:00 AM and 12:00 PM EST, when European and North American markets overlap, boosting liquidity.

With these strategies in place, let’s look at how to size positions effectively to manage leverage and risk.

Position Sizing and Leverage

Position sizing is a critical aspect of risk control. Since crude oil contracts can lead to significant profit or loss with even small price movements, professional traders generally risk no more than 0.5% of their equity per trade. They often adjust their positions based on recent volatility, using tools like the 25-day Average True Range.

Your margin cushion also plays a big role. For instance, in a $5,000 account, a 1-lot position (requiring $1,000 intraday margin) gives you 400 ticks of breathing room. But a 4-lot position (with a $4,000 margin requirement) leaves just 25 ticks before liquidation becomes a risk. As StoneX aptly puts it:

"Use [leverage] recklessly and perish; respect its power and prosper"

STOP LOSING TO LATENCY

Execute faster than

your competition.

Sub-millisecond execution • Direct exchange connectivity • From $59.99/mo

For smaller accounts, Micro Crude Oil (MCL) contracts offer a more flexible alternative. These contracts, representing 100 barrels with a $1.00 tick value, allow for finer position sizing and better risk control. They’re also a great way to test strategies without taking on excessive risk.

Risk Management Methods

Effective risk management starts with stop-loss orders, which should be based on technical levels or volatility metrics rather than fixed dollar amounts. Richard O. Zamora III, CMT, cautions:

"If your setup requires perfect fills to work, it is not robust enough for crude oil"

Crude oil markets can experience rapid price swings, especially during major announcements like the EIA Weekly Energy Stocks report (released Wednesdays at 10:30 AM ET). To protect against these moves, consider using OCO (One Cancels Other) bracket orders, which set both stop-losses and profit targets simultaneously. This is particularly useful during periods of high volatility when manual adjustments may lag.

Avoid holding large, unhedged positions during events like OPEC meetings or EIA reports to minimize the risk of extreme slippage. When volatility spikes, adjusting your contract size to maintain consistent dollar risk is a smart move. For example, during periods of higher Average True Range, scaling down your position can help keep your risk profile steady. Diversifying across different contract months or pairing CL with other energy products can also help smooth out your equity curve.

This naturally brings us to the role of technology in improving trade execution.

Using QuantVPS for Low-Latency CL Trading

For automated trading and scalping, having 24/7 uptime and ultra-low latency is critical. QuantVPS offers Windows-based remote servers designed specifically for financial markets. These servers ensure that platforms like NinjaTrader or MetaTrader remain unaffected by local power outages or internet issues.

In the fast-paced world of crude oil trading, low latency can make all the difference. With WTI averaging over 1 million contracts traded daily, algorithmic systems often execute trades faster than humans can react. QuantVPS minimizes execution delays by hosting servers near broker and exchange infrastructure, which is especially important during news-driven market swings where slippage can quickly escalate.

QuantVPS offers two main plans:

| Feature | Standard Plans | Performance Plans (+) |

|---|---|---|

| Best For | Manual trading, basic automation | High-frequency, scalping, advanced bots |

| Uptime | 24/7 stable environment | 24/7 with ultra-low latency optimization |

| Execution | Reliable | Optimized for speed-critical strategies |

| Starting Price | $59.99/month ($41.99/month annually) | $79.99/month ($55.99/month annually) |

| Network | 1Gbps+ unmetered bandwidth | 1Gbps+ with exchange proximity |

Both plans include features like DDoS protection, automatic backups, NVMe storage, and compatibility with major trading platforms. The Performance Plans (+) are ideal for traders competing with institutional algorithms in the highly liquid crude oil market.

Conclusion

This guide has covered the essential elements for successful CL trading, including contract details, risk management strategies, and the technical tools required for effective execution. To recap, a standard CL contract represents 1,000 barrels of West Texas Intermediate (WTI) crude oil, with a tick size of $0.01 per barrel. This means each tick is worth $10.00, and a full-point price move equates to a $1,000 gain or loss.

Managing risk effectively requires more than just good trading habits - it demands technology that ensures fast and reliable trade execution. Using stop-loss orders, based on technical levels or volatility, is especially critical during major events like the EIA Weekly Energy Stocks report, released every Wednesday at 10:30 AM ET. For those with smaller accounts, Micro WTI (MCL) contracts, representing 100 barrels with $1.00 tick values, provide a more accessible way to manage risk.

Given that CL futures trade nearly around the clock, uninterrupted connectivity is a must. QuantVPS delivers the infrastructure needed for strategies like scalping and automation, with constant uptime and ultra-low latency through servers positioned near exchange hubs. This setup is vital when every millisecond counts during high-volatility periods.

Whether you're trading trends tied to geopolitical events, executing spreads between contract months, or leveraging seasonal price patterns, success hinges on mastering contract specifications, maintaining disciplined risk control, and using dependable technology. Focus on proper position sizing and ensure your trading tools can handle the fast pace and volatility of the crude oil market.

FAQs

When should I roll a CL futures position to avoid delivery?

When trading CL futures, it's crucial to roll your position before the contract's expiration date, which is usually the last trading day of the contract month. To steer clear of the risk of physical delivery, it's wise to roll your position a few days in advance. Keep a close eye on expiration dates and plan ahead to either close or roll over your position, ensuring you avoid any delivery obligations.

How much money should I risk per CL trade based on volatility?

To handle risk in crude oil futures trading, it's wise to limit your risk to a small portion of your trading capital - typically around 1-2% per trade. This approach should also account for market volatility.

Each CL contract represents 1,000 barrels of crude oil, with each price tick valued at $10. For instance, if the average daily price fluctuation is $1 per barrel (equating to $1,000 per contract), setting a risk limit of $200 per trade helps you stay aligned with market movements while keeping potential losses under control.

Should I trade CL, QM, or MCL for my account size?

The best option for trading crude oil futures depends on your account size, goals, and how much risk you're comfortable taking:

- CL (Crude Oil Futures): This is the standard contract, representing 1,000 barrels. It comes with a higher margin requirement (around $2,000) and greater volatility, making it a better fit for larger accounts.

- QM (Mini Crude Oil): A smaller contract size of 500 barrels and a lower margin requirement make this a good choice for those with moderate-sized accounts.

- MCL (Micro Crude Oil): The smallest contract at just 10 barrels, with a margin requirement typically between $50 and $100. This is ideal for beginners or traders with smaller accounts.