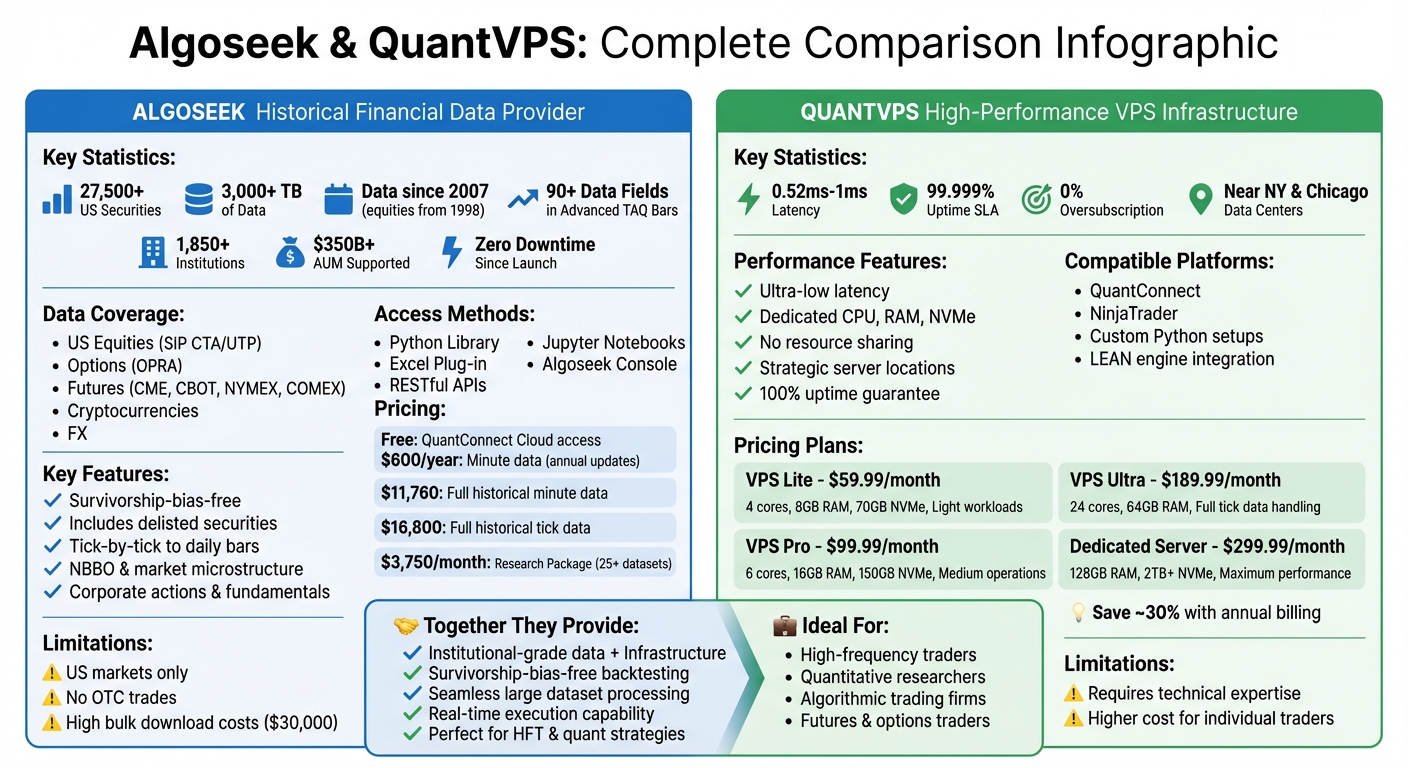

Algoseek provides traders with detailed historical financial data, covering over 27,500 US securities since 2007, and offers tools for seamless integration into trading workflows. Its data is survivorship-bias-free and includes delisted securities, making it ideal for accurate backtesting. Paired with QuantVPS, which delivers ultra-low latency and reliable infrastructure, traders can efficiently process large datasets and execute strategies without interruptions.

Key Highlights:

- Algoseek: Over 3,000 TB of data, 90+ fields in Advanced TAQ Bars, and flexible pricing starting at $600/year for minute data. Supports Python, Excel, and APIs for easy access.

- QuantVPS: High-performance VPS with 0.52ms–1ms latency, starting at $59.99/month. Ideal for handling computationally intensive tasks.

Quick Comparison:

| Service | Strengths | Limitations |

|---|---|---|

| Algoseek | Detailed US market data, survivorship-bias-free, 90+ data fields | US-only, excludes OTC trades, costly tick data downloads |

| QuantVPS | Low latency, 100% uptime, dedicated resources | Requires technical expertise for setup |

Together, these tools provide a robust solution for traders needing reliable data and infrastructure for research and live trading. Pricing and technical know-how are key factors to consider when choosing this setup.

Algoseek vs QuantVPS: Complete Feature and Pricing Comparison for Traders

1. Algoseek Historical Data

Data Features

Algoseek offers extensive data coverage across various markets, including US equities (SIP CTA/UTP), options (OPRA), futures (CME, CBOT, NYMEX, COMEX), cryptocurrencies, and FX. This data is available in multiple resolutions - ranging from tick-by-tick to daily bars - making it suitable for a wide range of trading strategies. What sets Algoseek apart is its detailed and granular data, which includes price, volume, NBBO (National Best Bid and Offer), and other key market microstructure metrics. These features are essential for developing advanced algorithmic trading strategies.

Additionally, Algoseek provides Security Master Files, corporate actions (like splits and dividends), options Greeks, fundamentals, short interest, and index compositions. Their dataset spans US equities data as far back as January 1998, offering an extensive historical view.

Run 24/7 while you sleep. Keep bots, platforms, and trade copiers online on a dedicated VPS.

Low-latency VPS hosting for your trading platform.

From $59.99/mo

Performance and Reliability

Algoseek’s infrastructure is built for high performance and reliability. Data is collected using co-located servers at Equinix and processed by a highly skilled R&D team - over 60% of whom hold PhDs. This setup ensures exceptional data accuracy and reliability. Impressively, Algoseek has maintained zero downtime since its launch, which is crucial for time-sensitive trading and research applications.

The platform follows a "golden source of truth" policy, ensuring consistency across historical, daily updated, and real-time datasets. For fast access to massive datasets, Algoseek employs ArdaDB (based on ClickHouse) and Volant SQL Server, enabling rapid SQL queries.

Usability for Traders

Algoseek enhances usability by offering tools that simplify integration for traders. Users can access the platform through a Python library, Excel plug-in, Jupyter Notebooks, RESTful APIs, and the Algoseek Console - a cloud-based environment ready for immediate use. Data is delivered in widely-used formats like CSV, JSON, Parquet, HDF5, Binary, and Feather, ensuring compatibility with various systems. The platform also integrates directly with QuantConnect's LEAN engine, making it easier to transition from research to live trading.

For large-scale operations, Algoseek’s Gateway Simple Storage (GSS) provides an S3-compatible interface for bulk downloads without egress fees. Additionally, the platform offers custom engineering services, such as "Data Pipeline as a Service" and "Ticker Plant as a Service", to handle tasks like data normalization, cleaning, and entity mapping.

"Trading is exciting, data is grinding. Leave data to algoseek." – Algoseek

Pricing

Algoseek provides flexible pricing options tailored to different needs. Through QuantConnect Cloud, full historical SIP data is accessible for free. For local storage, bulk annual updates cost $600 per resolution per year, while full historical downloads range from $11,760 for minute data to $16,800 for tick data.

Individual files can be purchased for 5–6 QCC per file, and a Research Package - featuring over 25 historical datasets dating back to 2007 - is available for $3,750 per month. Special pricing is available for startups, academic institutions, and emerging funds through an incubator program. Algoseek serves over 1,850 institutions, collectively supporting live trading assets under management (AUM) exceeding $350 billion.

2. QuantVPS: High-Performance VPS for Futures Trading

Performance and Reliability

QuantVPS is built to handle the demands of large historical datasets and intensive computational tasks. It offers ultra-low latency, ranging from 0.52ms to 1ms, and avoids oversubscription, ensuring consistent high-speed processing. This makes it a reliable choice for traders working with extensive data.

MicroTrends Ltd. highlights the platform's edge, stating, "QuantVPS's network consistently outperforms competitors in hop count analysis and avoids oversubscription issues that can hinder performance". This ensures that even during peak trading hours, backtesting operations remain smooth and uninterrupted. Such low-latency performance allows traders to fully leverage Algoseek's data in critical trading scenarios. These capabilities integrate seamlessly with the Algoseek data ecosystem, delivering the reliability traders need.

Usability for Traders

QuantVPS is equipped with dedicated resources, including CPU, RAM, and NVMe storage. Its servers are strategically located near key financial centers like New York and Chicago, ensuring quick access to data sources and execution venues.

For traders using platforms such as QuantConnect, NinjaTrader, or custom Python setups, QuantVPS simplifies deployment, enabling fast and efficient strategy execution. With a 99.999% uptime SLA, you can confidently run continuous backtesting or live trading strategies without interruptions.

By combining performance with ease of use, QuantVPS ensures a seamless trading experience, backed by competitive pricing designed to meet a variety of trading needs.

Pricing

QuantVPS offers plans tailored to different levels of trading activity:

- VPS Lite: $59.99/month – 4 cores, 8GB RAM, 70GB NVMe. Ideal for lighter workloads.

- VPS Pro: $99.99/month – 6 cores, 16GB RAM, 150GB NVMe. Suitable for medium-scale operations.

- VPS Ultra: $189.99/month – 24 cores, 64GB RAM. Designed for handling full historical tick data.

- Dedicated Server: $299.99/month – 128GB RAM, 2TB+ NVMe. Perfect for the most demanding computational needs.

Stay online and closer to execution. Choose a VPS location for CME futures, New York markets, London FX, API trading, and more.

Host your platform near the market route that matters.

From $59.99/mo

Opting for annual billing can save around 30% on all plans, making these options even more cost-effective for traders looking for long-term reliability.

Pros and Cons

When weighing the options between Algoseek and QuantVPS, both platforms bring distinct advantages and challenges to the table.

Algoseek stands out for its comprehensive, high-quality data. With over 90 data fields in its Advanced TAQ Bars - far surpassing the industry norm of around 20 fields - it provides an unmatched level of detail. Another key benefit is its inclusion of all delisted securities, offering a survivorship bias-free dataset that spans more than 100,000 US securities dating back to 2007.

That said, Algoseek's focus is heavily centered on US markets, limiting its appeal for those needing global data coverage. It also excludes Over-the-Counter (OTC) trades, and the cost of bulk tick downloads can be prohibitively high, reaching $30,000.

QuantVPS, on the other hand, excels in providing the infrastructure to handle massive datasets seamlessly. Features like ultra-low latency (0–1ms), 100% uptime, and dedicated resources ensure reliability during backtesting. Plus, its server locations near New York and Chicago help minimize data access times.

However, QuantVPS requires a certain level of technical expertise for proper setup, especially when integrating it into complex data workflows. Additionally, the VPS Ultra plan, priced at $189.99 per month, might feel expensive for individual traders, though opting for annual billing can lower costs by about 30%.

| Service | Key Strengths | Notable Limitations |

|---|---|---|

| Algoseek | 90+ data fields; survivorship bias-free; SecID tracking; detailed tick-level records | US markets only; excludes OTC trades; high bulk download costs ($30,000) |

| QuantVPS | Ultra-low latency (0–1ms); 100% uptime; dedicated resources; strategic locations | Requires technical expertise |

These comparisons highlight the trade-offs you’ll want to consider when building your trading infrastructure. Each service caters to specific needs, so your choice will depend on your priorities, whether it's data depth or infrastructure reliability.

Conclusion

Combining Algoseek's extensive historical data with QuantVPS's high-performance infrastructure creates a powerful ecosystem for trading and research. Algoseek offers institutional-level data, free from survivorship bias, covering around 27,500 US securities with significant historical depth - perfect for precise backtesting and developing quantitative models. This level of accuracy is crucial for crafting effective high-frequency trading strategies.

On the other hand, QuantVPS enhances this setup with its robust computing capabilities. Its ultra-low latency (0–1ms) and guaranteed 100% uptime ensure seamless processing of large datasets, complex machine learning models, and multi-chart analyses. Together, these tools form a reliable system for conducting in-depth historical research and executing real-time trades without performance hiccups.

For high-frequency traders and quantitative researchers, this partnership is especially beneficial. As QuantConnect highlights, "AlgoSeek data is built for quantitative trading and machine learning". Pairing it with QuantVPS's low-latency infrastructure reduces the risk of poor input data compromising algorithmic strategies. Futures and options traders, in particular, benefit from QuantVPS's swift data access, which ensures timely and accurate order execution.

Pricing also plays a role in shaping this choice. Algoseek's cost positions it for institutional use, but smaller traders or funds can start with more affordable options, such as minute or daily resolutions priced between $600 and $11,760 annually. For those just starting, QuantConnect’s free cloud access offers a way to test Algoseek data before scaling up.

Ultimately, the decision comes down to your strategy and technical expertise. If you require deep historical data for US markets and the infrastructure to handle it, Algoseek and QuantVPS offer a professional-grade solution. However, this setup demands technical know-how to configure and optimize effectively.

FAQs

Which Algoseek dataset should I choose for my strategy?

When choosing an Algoseek dataset, it’s essential to match it with your strategy and the level of detail you require. For intraday trading, the US Equities Trade and Quote Minute Bar datasets are a great fit. They provide minute-level insights, including metrics like OHLCV (Open, High, Low, Close, Volume), trade details at bid/mid/ask prices, and spread analysis - perfect for precise, short-term strategies.

If you're working with longer-term strategies, the US Equities dataset is ideal. It offers survivorship bias-free daily data going back to 1998, making it suitable for broader, high-level analysis without needing minute-by-minute granularity.

How do I avoid survivorship bias when backtesting with Algoseek?

To steer clear of survivorship bias when backtesting with Algoseek, it's crucial to use datasets that include both active and delisted securities. Algoseek’s US Equities dataset is a great example - it’s free from survivorship bias. It covers all stocks traded on US SIP CTA/UTP feeds since 1998, including those that have been delisted. This approach ensures your backtests reflect the performance of not only successful assets but also those that failed or were removed, giving you a more accurate and realistic view of potential outcomes. Always double-check that your data source explicitly mentions the inclusion of delisted securities.

What’s the simplest way to store and query Algoseek data on a VPS?

If you're working with Algoseek data on a VPS, the simplest solution is the algoseek-connector Python library. You can install it quickly using pip: pip install algoseek-connector. This library provides SQL-like tools for tasks like filtering, grouping, and sorting your data. Plus, it allows you to retrieve results as pandas DataFrames, making it easy to analyze large datasets without a complicated setup.