Volatility arbitrage is a trading strategy that exploits the difference between implied volatility (IV) and realized volatility (RV). Traders use this approach to profit from options mispricing without predicting market direction. Here’s how it works:

- When IV > RV: Options are overpriced. Traders sell options (short volatility).

- When IV < RV: Options are underpriced. Traders buy options (long volatility).

- Delta-neutral positions: These are used to eliminate directional risk, focusing solely on volatility mispricing.

Key tools and metrics include:

- Volatility Risk Premium (VRP): The consistent difference between IV and RV.

- Z-scores: Used to assess whether VRP is unusually high or low.

- IV Rank (IVR) & IV Percentile (IVP): Help identify actionable opportunities.

Automation is critical in managing delta-neutral positions, rebalancing hedges, and executing trades efficiently. Platforms like QuantVPS offer low-latency infrastructure to handle these tasks in real time.

Effective risk management involves:

- Setting profit targets and time stops.

- Monitoring VRP and market conditions.

- Using automated workflows to minimize errors and delays.

Key Metrics and Tools for Volatility Arbitrage

Implied vs. Realized Volatility: What You Need to Know

Implied volatility (IV) reflects the market's expectations of future price swings based on option prices, while realized volatility (RV) measures the actual historical price fluctuations over a given period.

The difference between these two metrics creates opportunities for volatility arbitrage. As the StrikeWatch EA Research Team explains:

"Implied volatility overstates realized volatility approximately 85% of the time. This is not a temporary anomaly or a statistical artifact."

This consistent disparity, known as the volatility risk premium (VRP), is the foundation of many arbitrage strategies. To minimize noise and improve accuracy, it’s important to align the time frames of IV and RV (e.g., compare 30-day IV with 30-day RV).

A clear grasp of these measures is crucial for identifying profitable arbitrage scenarios.

Key Metrics for Spotting Arbitrage Opportunities

Several metrics help traders refine their approach, particularly for delta hedging and maintaining a market-neutral stance. However, the IV–RV spread must always be interpreted in context. For instance, a 4-point VRP might seem significant in a calm market but could be common in a highly volatile environment. To evaluate the spread more effectively, traders often use a rolling 252-day Z-score to determine whether the current premium is unusually high or low compared to the past year.

| VRP Z-Score | Interpretation | Recommended Action |

|---|---|---|

| > 2.0 | Extreme VRP expansion | Take maximum position size |

| 0.5 to 1.5 | Above-average VRP | Sell premium at 50–75% of position size |

| -0.5 to 0.5 | Average VRP | Limited edge; reduce position size to 25–50% |

| < -1.0 | Deeply compressed | No edge; avoid premium selling |

Run 24/7 while you sleep. Keep bots, platforms, and trade copiers online on a dedicated VPS.

Low-latency VPS hosting for your trading platform.

From $59.99/mo

Beyond the IV–RV spread, traders often monitor two additional metrics for context:

- IV Rank (IVR): Compares the current IV to its 52-week range. A reading above 50 suggests higher-than-usual premium levels.

- IV Percentile (IVP): Indicates the percentage of days in the past year when IV was lower than it is today.

By combining these metrics, traders can better gauge opportunities and risks, especially in varying market conditions.

Tools and Data Sources to Use

Efficient tools can simplify the process of calculating and analyzing volatility. Python libraries like numpy and pandas are excellent for quick computations, while yfinance can retrieve historical OHLC data to construct a basic RV calculator.

The choice of RV estimator is equally important. While the standard close-to-close method is simple, it overlooks overnight price gaps, which can be significant. For equities, the Yang-Zhang estimator is a popular choice because it accounts for both overnight gaps and intraday drift, offering a more accurate and balanced result.

| Estimator | Inputs | Best Use Case |

|---|---|---|

| Close-to-Close | Daily close prices | Quick, basic estimates; misses overnight gaps |

| Parkinson | Daily high/low prices | Captures intraday range; statistically efficient |

| Yang-Zhang | OHLC + prior close | Ideal for equities; handles overnight gaps and intraday drift |

For those looking for ready-made metrics, professional APIs provide pre-calculated data, including ATM IV, multi-window RV, VRP spreads, and Gamma Exposure (GEX) metrics. These APIs can be integrated into custom dashboards or automated systems using Python SDKs. Hosting these tools on a reliable VPS for stocks and options ensures uninterrupted data flow during crucial trading hours.

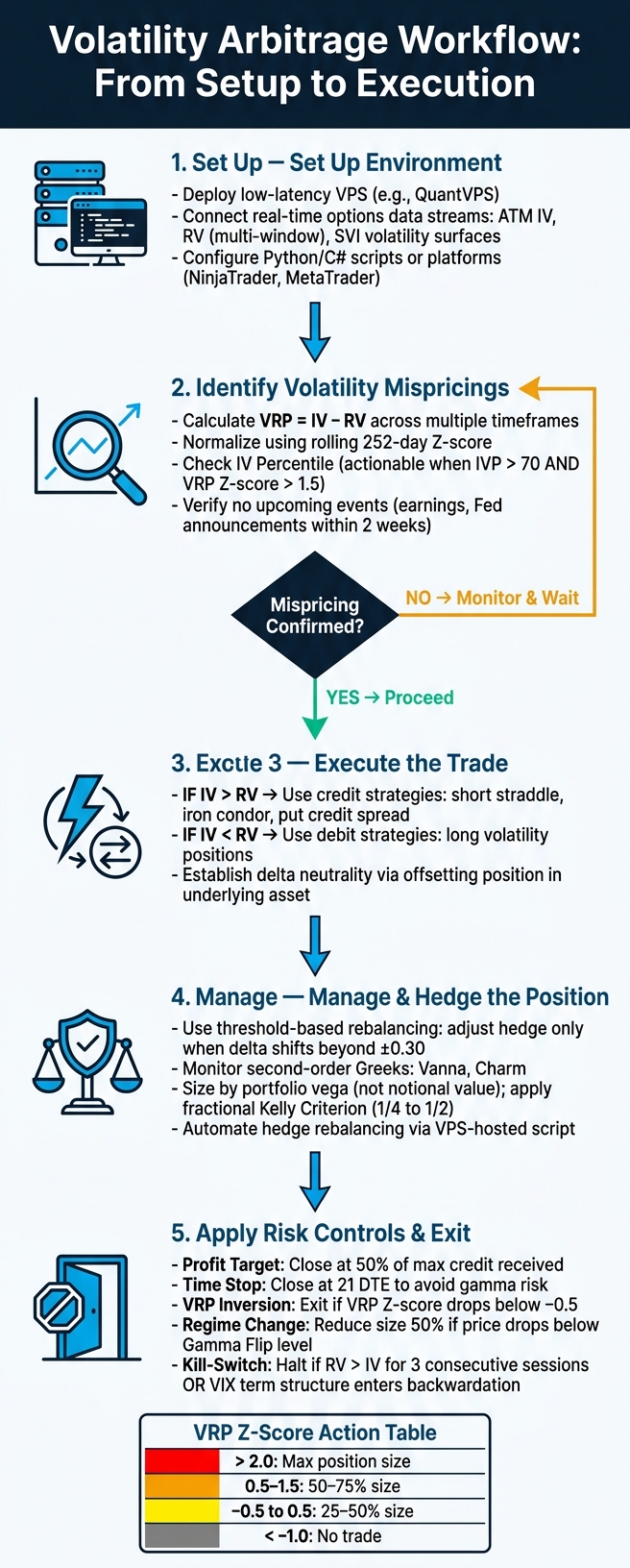

Step-by-Step Volatility Arbitrage Workflow

Volatility Arbitrage Workflow: From Setup to Execution

Setting Up Your Trading Environment

To trade volatility effectively, start with a low-latency VPS. Even a slight delay, like 200ms in updating Greeks, can result in margin calls. Platforms like QuantVPS provide high-performance plans with dedicated resources to handle Greek calculations, data ingestion, and automated hedging routines simultaneously without slowing down. Their 1Gbps+ network and Windows Server 2022 environment make it easy to run tools like NinjaTrader, MetaTrader, or custom algorithmic setups built in Python or C# using broker SDKs.

Your VPS should maintain constant, real-time connections to options data streams. These streams should include metrics like at-the-money (ATM) implied volatility, realized volatility across multiple windows, and SVI volatility surfaces. This setup ensures you’re ready to act during the short windows when mispricings emerge. Once your VPS is live and data streams are active, you’re ready to detect volatility discrepancies.

How to Identify Volatility Mispricings

Start by calculating the Volatility Risk Premium (VRP), which is the difference between implied volatility (IV) and realized volatility (RV), across various timeframes. However, the raw spread isn’t enough. Normalize it using a rolling 252-day Z-score to determine whether the current premium is unusually high or low compared to historical trends.

"The gap between what the market expects and what actually happens is where volatility traders make - or lose - money." - FlashAlpha

To confirm your findings, check the IV Percentile. Mispricings are most actionable when the IV Percentile exceeds 70 and the VRP Z-score is above 1.5, indicating a premium worth selling. Don’t forget to check for upcoming events like earnings releases or Federal Reserve announcements within the next two weeks. Elevated IV in these cases might not be a mispricing but a reflection of anticipated market volatility.

Another factor to consider is the tendency for put VRP to be larger than call VRP. Institutional investors often overpay for downside protection, so when the put-side spread is significantly wider, a put credit spread may offer better risk-adjusted returns than a more balanced strategy like an iron condor. Once you’ve confirmed the mispricing and ensured it aligns with your risk-neutral framework, it’s time to move on to trade execution and hedging.

Executing and Managing Trades

The structure of your trade depends on the relationship between IV and RV. When IV is higher than RV, credit strategies like short straddles, iron condors, or put credit spreads are often effective. On the other hand, if IV is unusually low compared to RV, consider debit strategies or long volatility positions.

To isolate volatility risk, establish delta neutrality by taking an offsetting position in the underlying asset. As the underlying price moves, gamma effects will cause the option’s delta to shift, requiring frequent hedge adjustments. Automate this rebalancing process using a VPS-hosted script to avoid delays, especially in fast-moving markets. This ensures your position remains market-neutral, which is essential for volatility arbitrage.

Position sizing should focus on portfolio vega exposure rather than notional value. For instance, a 1-year LEAPS option has roughly 3.5 times the vega of a 1-month option. Mixing maturities without accounting for this can increase your volatility risk. Additionally, pay attention to second-order Greeks like Vanna and Charm. These metrics help predict how your delta hedge might drift as IV changes or as time passes.

Risk Management and Automation in Volatility Arbitrage

Delta Hedging and Position Management

Keeping a position delta-neutral is the backbone of managing volatility risk in volatility arbitrage. Once a trade is active, your main task is to ensure that delta neutrality is maintained. This is because as the underlying asset moves, the option delta changes, which can erode the volatility edge you’re trying to capture.

"Delta is noise that can get in the way of us [monetizing the difference between implied/realized volatility] successfully." - Sean Ryan, Predicting Alpha

Instead of hedging with every small market move, you can adopt threshold-based rebalancing, which only adjusts the hedge when delta shifts beyond ±0.30. This approach minimizes transaction costs and slippage while still managing directional risk effectively.

For a more active strategy, gamma scalping involves trading the underlying asset to capture small profits from price fluctuations. This method works well when realized volatility exceeds the cost of theta decay, but executing it manually can be challenging and requires precision.

How to Set Risk Controls

Once you’ve established a hedge, having clear exit criteria is essential to protect your position. Risk controls in volatility arbitrage go beyond simple stop-losses; they define the exact scenarios where a trade no longer aligns with your strategy.

The table below highlights key automated risk controls worth integrating into your workflow:

Stay online and closer to execution. Choose a VPS location for CME futures, New York markets, London FX, API trading, and more.

Host your platform near the market route that matters.

From $59.99/mo

| Risk Control | Trigger | Action |

|---|---|---|

| Profit Target | 50% of max credit received | Close position to secure gains and reduce variance |

| Time Stop | 21 days to expiration (DTE) | Close to avoid increased gamma risk |

| VRP Inversion | VRP z-score drops below -0.5 | Exit immediately - the edge has disappeared |

| Regime Change | Price drops below Gamma Flip level | Close or reduce position size by 50% |

| Vega Limit | 0.5% of capital per position | Limit total portfolio vega exposure |

Exiting at 50% of max credit captures roughly 85% of the expected profit while cutting profit-and-loss variance by 60%. For position sizing, using a fractional Kelly Criterion (typically 1/4 to 1/2) calibrated to the VRP z-score can help avoid overcommitting capital during uncertain market conditions.

You should also monitor the GEX-VRP matrix when adjusting position sizes. For instance:

- In a positive gamma, high-VRP scenario (Cell A), you can size up to 1.5–2x.

- In a negative gamma, high-VRP scenario (Cell B), limit exposure to 0.5x and stick to defined-risk structures.

- When both gamma and VRP are unfavorable (Cell D), the best position size is zero.

These risk controls lay the groundwork for automating your trading processes efficiently.

Automating Your Workflow on QuantVPS

To ensure consistent execution of these risk controls, automation is key. Monitoring Greeks, VRP z-scores, and regime changes manually is impractical, especially when market conditions can shift rapidly. Using QuantVPS’s low-latency platform allows you to automate these processes and respond instantly.

An automated workflow on QuantVPS typically involves:

- Pulling live data from options APIs (e.g., ATM implied volatility, realized volatility across multiple timeframes, and VRP spreads).

- Running signal checks against pre-set thresholds.

- Routing orders through broker APIs like Interactive Brokers when conditions are met.

Python scripts are particularly effective for this setup. QuantVPS’s Windows Server 2022 environment supports Python and C# alongside platforms like NinjaTrader or MetaTrader, giving you flexibility in building your automation stack.

For short-volatility strategies, include an automated kill-switch. Program it to halt trading if realized volatility exceeds implied volatility for three consecutive sessions or if the VIX term structure enters backwardation. These signals indicate that the statistical edge has disappeared, and continuing to trade in such conditions could lead to losses.

QuantVPS offers plans like VPS Pro (6 cores, 16GB RAM, 150GB NVMe at $99.99/month) and VPS Ultra (24 cores, 64GB RAM, 500GB NVMe at $189.99/month). These plans provide the computational power to handle real-time Greek calculations, API polling, and order execution - crucial when your hedge scripts need to operate in milliseconds.

Best Practices and Common Pitfalls in Volatility Arbitrage

Common Mistakes to Avoid

When diving into volatility arbitrage, it's crucial to steer clear of common execution errors that can undermine your strategy. One frequent misstep is misjudging the implied volatility (IV) premium. Traders often rush to short volatility when they see elevated IV levels, without considering the event calendar. This can backfire, as events like earnings reports, Federal Reserve meetings, or FDA decisions naturally push IV higher in the days leading up to them. Ignoring these timelines can quickly eat into your profits.

Another classic error involves mismatched timeframes, which can lead to unreliable signals. For example, comparing 20-day realized volatility (RV) to an option with 60 days until expiration creates an inaccurate picture. The RV window should always align with the option's remaining time to expiration. Additionally, transaction costs can quietly erode profits. Frequent delta-hedging, while essential, generates slippage and commissions that can diminish the already thin margins typical of arbitrage strategies.

Best Practices for Running These Strategies

To navigate these challenges, adopting a disciplined approach is key. Start by focusing on a small selection of underlyings and develop a deep understanding of their behavior. Spreading your attention across too many tickers too soon can make it harder to monitor shifts in term structure, skew changes, and event risks simultaneously.

Incorporate IV Percentile into your analysis to determine whether implied volatility is genuinely elevated. Pair this with multi-window realized volatility measurements - such as 5-day, 20-day, and 60-day windows - to identify whether a volatility regime is gaining or losing momentum before entering a trade.

Stress-testing your strategy is another essential step. Underestimating tail risk can lead to significant losses, as history has shown. On major indices, implied volatility outpaces realized volatility about 85% of the time, but extreme deviations can still result in severe drawdowns.

"Volatility arbitrage is not 'true economic arbitrage' (in the sense of a risk-free profit opportunity). It relies on predicting the future direction of implied volatility." - Wikipedia

Finally, ensure your infrastructure is up to the task. Running Greek calculations, API polling, and order routing on unstable or underpowered systems introduces unnecessary execution risk. Tools like VPS Pro and VPS Ultra from QuantVPS offer the processing power and uptime needed to keep automated workflows running smoothly. In fast-moving markets, delayed hedging can quickly turn a neutral position into a losing one, so reliable infrastructure is non-negotiable.

Key Takeaways for Traders

Success in volatility arbitrage demands precision and discipline. Your edge lies in accurately predicting realized volatility and maintaining delta neutrality. Combining this with reliable, low-latency infrastructure ensures transaction costs don’t quietly erode your profits. QuantVPS delivers the high-performance environment, Windows Server 2022 compatibility, and scalable resources that make executing these strategies both efficient and practical.

FAQs

How do I choose the right IV and RV timeframes to compare?

To effectively compare implied volatility (IV) and realized volatility (RV), it's crucial to align their timeframes. Typically, a 30-day horizon is used for at-the-money (ATM) IV, consistent with the VIX standard. For RV, it's best to use a 20- or 30-day window to ensure alignment with IV. Shorter windows, like 5 days, should be avoided as they tend to introduce unnecessary noise. When calculating RV, always annualize it using the square root of 252 to account for the number of trading days in a year.

How often should I rebalance a delta-neutral hedge?

To keep a delta-neutral hedge intact, frequent rebalancing is required as the underlying asset's price fluctuates and the option's delta changes. While the concept of continuous rebalancing sounds perfect in theory, most traders opt for active adjustments that align with current market conditions. Skipping regular rebalancing can allow directional risk to slip back into your volatility arbitrage strategy as the option's sensitivity shifts over time.

What market conditions can break a short-volatility edge?

When realized volatility spikes and outpaces implied volatility, a short-volatility strategy can falter. This often happens during market panics, crashes, or extreme events. Other contributing factors include:

- Extended periods of low volatility, where implied volatility only slightly exceeds realized volatility.

- Persistent market trends that push realized volatility above implied levels.

- Dealer positioning, such as negative gamma, which can intensify sell-offs and heighten tail risks, even when volatility premiums seem appealing.