Liquidity risk management ensures financial institutions can meet obligations during normal operations and crises. A Liquidity Risk Manager monitors cash flows, ensures regulatory compliance, and prepares for sudden market disruptions. Key skills include quantitative analysis, regulatory expertise, and effective communication.

Here’s what you need to know:

- What is liquidity risk? The risk of a firm failing to meet financial obligations due to funding shortages or market illiquidity.

- Why it matters: Mishandling liquidity risk can cause credit crunches, market instability, or even firm collapse.

- Key responsibilities: Monitoring cash flows, conducting stress tests, preparing regulatory reports, and managing contingency plans.

- Skills required: Strong analytical abilities, regulatory knowledge, and clear communication.

- Career path: Entry-level roles (Risk Analyst) lead to senior positions (VP or Treasury Manager), with certifications like FRM and CFA boosting prospects.

The demand for liquidity risk experts is growing, fueled by evolving regulations and the need for real-time risk management. Expect opportunities to expand as automation and AI reshape the field.

Core Responsibilities of a Liquidity Risk Manager

At the heart of liquidity risk management lies the ability to evaluate, predict, and address vulnerabilities in cash flow. Liquidity Risk Managers play a crucial role by keeping a close eye on cash flows, managing risks through technical analysis, ensuring compliance with regulations, and maintaining clear communication within their organizations.

Identifying and Measuring Liquidity Risk

The first step in managing liquidity risk is recognizing where potential issues may arise. Liquidity Risk Managers monitor defined cash flows to detect possible shortfalls early. They rely on key metrics like the Liquidity Coverage Ratio (LCR) and the Net Stable Funding Ratio (NSFR) to gauge the organization's liquidity health.

In addition to these ratios, they analyze areas like maturity mismatches, where short-term liabilities are used to fund long-term assets. They also evaluate available collateral - assessing its type, quantity, and the "haircuts" applied when it’s pledged for funding purposes.

Early Warning Indicators (EWIs) are another critical tool. These might include sudden spikes in withdrawals or reductions in available credit lines. When such signals arise, they trigger timely escalation to address issues before they spiral into crises.

Once risks are identified, managers run simulations to understand how adverse scenarios might impact liquidity.

Stress Testing and Scenario Analysis

Stress testing is essential for evaluating how an organization would fare under extreme market conditions. Managers craft scenarios that include idiosyncratic events (like a credit rating downgrade), market-wide disruptions (such as a freeze in the repo market), and even modern risks like social media-driven bank runs or crypto-asset instability.

These scenarios are designed with varying levels of severity - mild (1-in-10-year events), moderate (1-in-25-year events), and severe (1-in-100-year events) - to provide a comprehensive view of potential outcomes. Advanced teams often use Monte Carlo simulations, running over 10,000 iterations nightly across different time frames (e.g., 1, 7, 30, and 90 days) to model potential liquidity shifts.

A particularly insightful method is reverse stress testing, which flips the usual approach. Instead of asking, “What happens if X occurs?” managers ask, “What would it take to push us to the brink?” This technique helps uncover hidden vulnerabilities that traditional models might miss. As consultant Chris Koo highlighted:

"The collapse of Silicon Valley Bank reminded the industry that liquidity crises can unfold in hours, not days."

These tests not only prepare firms for adverse situations but also guide regulatory reporting and governance strategies.

Regulatory Reporting and Governance

Compliance with regulations is a cornerstone of liquidity risk management. In the U.S., this includes adhering to Basel III standards, which require maintaining an LCR of at least 100% and an NSFR of at least 100% over a one-year horizon to ensure stable funding. Broker-dealers also need to accurately file the Supplemental Liquidity Schedule (SLS), avoiding common errors like misidentifying counterparties or providing incomplete securities lending data.

Governance responsibilities go beyond meeting regulatory requirements. Liquidity Risk Managers establish regular oversight processes for assets and liabilities, engage in strategic planning, and formalize liquidity risk appetite statements - for instance, committing to maintain an LCR buffer of 110% above the regulatory minimum. They also create Contingency Funding Plans (CFPs), which are detailed playbooks outlining roles and actions during a liquidity crisis to ensure swift and coordinated responses.

"Effective coordination with executive management, business units, control departments and technology is critical for success." - Goldman Sachs

Run 24/7 while you sleep. Keep bots, platforms, and trade copiers online on a dedicated VPS.

Low-latency VPS hosting for your trading platform.

From $59.99/mo

Skills Required for Liquidity Risk Managers

Effective liquidity risk management calls for a mix of technical expertise, regulatory knowledge, and strong interpersonal abilities. These skills work together to support quick and informed decision-making.

Quantitative and Analytical Skills

Liquidity risk managers rely on tools like cash-flow modeling and statistical analysis to predict how balance sheets will behave under both normal and stressed conditions. Techniques such as Liquidity-Adjusted Value-at-Risk (L-VaR), which accounts for market impact costs, and Principal Component Analysis (PCA), which identifies the main drivers behind liquidity shocks, are commonly used.

Behavioral analysis sharpens assumptions about liability behaviors. For instance, historical withdrawal patterns might suggest assigning 10% maturity buckets for retail deposits and 40% for wholesale deposits. Stress testing adds another layer, modeling scenarios where roll-over rates for unsecured borrowings could drop by as much as 20–80% during a liquidity crisis.

Monitoring intraday liquidity is also crucial. This involves tracking real-time payment and settlement obligations to avoid funding shortfalls.

Regulatory Knowledge

Understanding and applying regulatory frameworks is more than just meeting compliance standards. As noted by researchers Sebastian Doerr and Mathias Drehmann in BIS Papers No. 164:

"Liquidity regulation is not only a compliance metric. It changes balance sheet structure, funding incentives, lending capacity, asset composition, and the way institutions prepare for stress."

In the United States, key regulations include 12 CFR Part 329 (covering LCR and NSFR for FDIC-supervised institutions), SEA Rule 15c3-3 (the Customer Protection Rule, which limits available liquidity by requiring segregation of customer assets), and DFAST/CCAR stress testing requirements. Managers must also distinguish between assets that are technically eligible as High-Quality Liquid Assets (HQLA) and those that are operationally ready to be monetized under stress.

"A liquidity buffer is only useful if the assets are available, operationally accessible, legally unencumbered, and capable of being converted into cash under stress." - Limax FinRisk

This means regularly revisiting assumptions like deposit run-off rates and collateral haircuts, especially as digital banking accelerates the speed of potential outflows. Staying proactive ensures managers adapt their risk models to evolving market conditions, beyond just meeting regulatory requirements.

Communication and Stakeholder Management

The most sophisticated analysis is useless if it isn’t clearly communicated to the right people. Liquidity risk managers must translate complex data into actionable insights for diverse audiences, from treasury teams to board members.

One critical platform for this is the Asset Liability Management Committee (ALCO), where liquidity metrics are reviewed on a weekly tactical and quarterly strategic basis. Managers who integrate their findings into these regular discussions help create alignment across the organization, enabling faster responses to changing conditions.

Poor communication can have serious consequences. Teams that operate in silos - failing to share information across departments or levels - are slower to identify and respond to risks.

"There needs to be collaboration between risk and the business, vertically up and down but then also horizontally across the organization. The problem is there are silos." - Michael Rasmussen, CEO, GRC Report

Defining clear escalation protocols in advance is essential. For example, specifying who gets notified when an LCR threshold is breached ensures that key leaders, like the CEO and CRO, are informed before a situation escalates. These communication and coordination skills are essential for advancing in liquidity risk management roles.

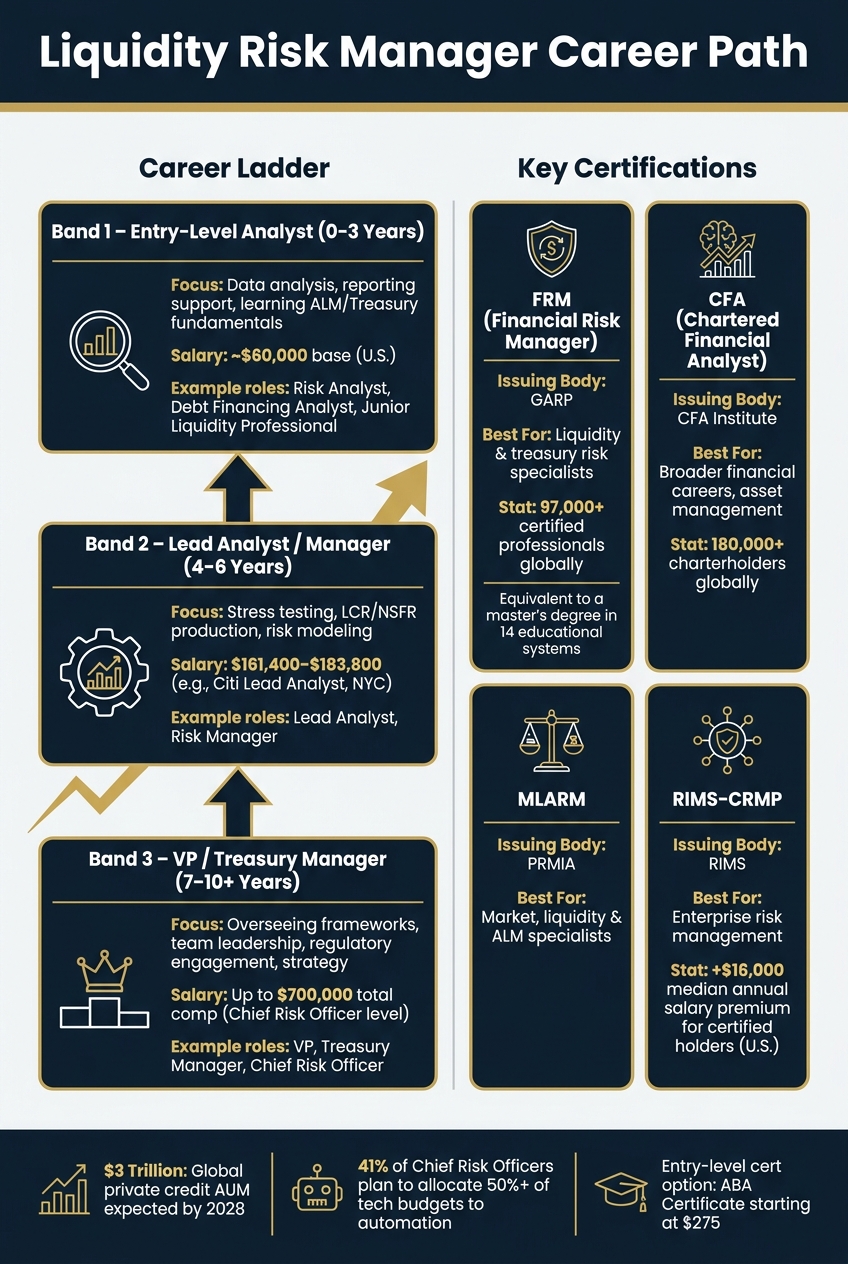

Career Path in Liquidity Risk Management

Liquidity Risk Manager Career Path: Roles, Salaries & Certifications

Entry-Level Roles and Requirements

Starting out in liquidity risk management typically involves roles like Risk Analyst, Debt Financing Analyst, or Junior Liquidity Professional. To land these positions, a bachelor's degree in fields like Finance, Economics, Mathematics, or Business Administration is usually required. Early responsibilities often include tasks such as gathering and cleaning risk-related data, assessing potential exposures, and preparing reports for senior team members.

Many banks offer tailored programs to accelerate skill development for newcomers. For instance, initiatives like Bank of America's Quantitative Analytics Development Program and Goldman Sachs' apprenticeship model provide hands-on experience in real-world risk management settings.

"There is so much opportunity to find things that you never knew you could enjoy so much - they're just there for you to discover." - Stephane, Analyst, Market Risk and Capital Quantification Group, Goldman Sachs

As professionals build foundational skills, they gradually transition into more strategic roles with broader responsibilities.

Mid-Level and Senior Positions

Career growth in liquidity risk management is often straightforward, with advancement typically requiring five to ten years of practical experience. Here's a snapshot of the career progression:

| Career Level | Typical Experience | Primary Focus |

|---|---|---|

| Entry-Level Analyst | 0–3 years | Data analysis, reporting support, learning ALM/Treasury fundamentals |

| Lead Analyst / Manager | 4–6 years | Stress testing, LCR/NSFR production, risk modeling |

| VP / Treasury Manager | 7–10+ years | Overseeing frameworks, team leadership, regulatory engagement, strategy |

At the mid-level, professionals shift from supporting tasks to leading initiatives. For example, a Lead Analyst at Citibank is expected to manage stress testing processes, supervise regulatory reporting, and independently conduct complex risk evaluations. As of April 2026, Citi's Liquidity Management Lead Analyst role in New York offered a salary range of $161,400 to $183,800. This position required either a master's degree with four years of experience or a bachelor's degree with six years.

Senior roles, such as Vice President or Treasury Manager, come with added responsibilities like leading teams, shaping strategies, and directly interacting with regulators. These professionals often present to senior executives and take ownership of the institution's contingency funding plans.

Certifications and Education

Climbing the ladder in liquidity risk management often involves pursuing additional certifications and education. While not mandatory at the entry level, certifications become increasingly valuable as careers progress. Key credentials include the Financial Risk Manager (FRM), CFA Charter, MLARM, and RIMS-CRMP:

| Certification | Issuing Body | Best For |

|---|---|---|

| FRM | GARP | Risk managers focused on liquidity and treasury risk (Part II) |

| CFA | CFA Institute | Broader financial careers, including asset management and investing |

| MLARM | PRMIA | Specialists in market, liquidity, and asset liability management |

| RIMS-CRMP | RIMS | Risk management across organizational functions |

The FRM certification is widely recognized as a standard in the field. It’s considered equivalent to a master’s degree in 14 educational systems, including the U.S., and is held by over 97,000 professionals globally. Certified risk professionals holding the RIMS-CRMP designation in the U.S. reportedly earn a median of $16,000 more annually than their non-certified counterparts.

"The FRM Program gave me the holistic knowledge I need to excel in my job. Thanks to the curriculum, I can now evaluate risks at smaller financial institutions with ease." - Guðmundur Örn Jónsson, Senior Risk Analyst, Central Bank of Iceland

For those looking for a more affordable way to get started, the ABA Certificate in Financial and Credit Risk Management is available at $275 for members and $375 for non-members. Another budget-friendly option is the IIA’s Liquidity Risk Management on-demand course, priced at $89, which offers practical insights for beginners before committing to a full certification program.

Key Challenges and Trends in Liquidity Risk Management

Stay online and closer to execution. Choose a VPS location for CME futures, New York markets, London FX, API trading, and more.

Host your platform near the market route that matters.

From $59.99/mo

Regulatory Changes and Compliance

Regulations are always evolving, and liquidity risk managers must keep up. A recent example is the SEC's update to Rule 15c3-3, which mandates certain firms to shift from weekly to daily reserve formula computations by June 30, 2026. This change isn’t just procedural - it forces firms to rethink how they model funding needs and stress scenarios, requiring a comprehensive review of contingency funding plans ahead of the deadline.

Beyond the specifics of compliance, there's a growing debate about whether current frameworks genuinely achieve resilience.

"It is time to move beyond asking whether banks are compliant and ask whether compliance actually translates into resilience." - Michelle W. Bowman, Vice Chair for Supervision, Federal Reserve

These regulatory updates highlight the broader challenge of ensuring precise reporting and integrating advanced technology to meet compliance demands effectively.

Data Quality and Technology Integration

A liquidity model is only as reliable as the data it relies on. Unfortunately, fragmented systems are a persistent hurdle. When data is scattered across different silos, it becomes a challenge to maintain a real-time, comprehensive view of a firm's liquidity position.

To address this, the industry is leaning heavily on automation and real-time infrastructure. For instance, one financial institution slashed its model run time from 6 hours to just 30 minutes by transitioning from spreadsheets to a real-time processing engine. Tools like Python and SQL are now standard for cash-flow projections and Liquidity-Adjusted Value-at-Risk (L-VaR) calculations, while platforms like Power BI provide live dashboards, enabling management to make decisions based on up-to-the-minute data. Cloud-based data lakes, hosted on platforms like AWS or Azure, further enhance efficiency by streaming cash-flow updates and triggering automated alerts when risk thresholds are exceeded.

Here’s a quick look at common data quality challenges and how technology helps tackle them:

| Data Quality Issue | Mitigation Strategy | Tool/Technology |

|---|---|---|

| Completeness | Data lineage mapping; reconciliation routines | Data lakes, SQL |

| Accuracy | Automated validation checks; exception management | Python, proprietary engines |

| Timeliness | Real-time API feeds; streaming data platforms | APIs, AWS/Azure |

AI and machine learning are also stepping in to improve anomaly detection in intraday flows and predict depositor behavior. This is particularly crucial as digital banking has accelerated the speed and unpredictability of bank runs.

Balancing Growth and Risk

Maintaining larger liquidity buffers provides a safety net during times of stress, but it also means fewer assets are available for lending and other productive uses. This creates a strategic balance sheet challenge that goes beyond mere compliance.

A key issue here is the buffer usability stigma. Large banks currently hold about 25% of their balance sheets in safe assets, compared to just 10% before the 2008 financial crisis. While these buffers are designed to be used during stress, both markets and regulators often treat the Liquidity Coverage Ratio's (LCR) 100% threshold as a hard limit. This discourages firms from tapping into their buffers, even when doing so is appropriate.

"By driving banks to exhaust regulatory buffers before accessing the discount window, we have entrenched discount window stigma. If you only go to the window when things are really bad, then going to the window signals that things are really bad." - Jonathan McKernan, Under Secretary for Domestic Finance

Addressing this issue requires more than regulatory tweaks. Firms need board-approved protocols that outline when and how buffers should be used, with clear escalation processes and communication strategies. Viewing liquidity solely as a compliance task limits flexibility. Firms that integrate it into broader capital and growth strategies will be better equipped to handle this delicate balancing act.

Conclusion and Next Steps

Key Takeaways

Liquidity risk management is more than just crunching numbers or ticking off compliance checklists. It’s a dynamic mix of quantitative analysis, regulatory know-how, and strategic thinking. The job today demands real-time monitoring, the ability to stress-test intricate scenarios, and clear communication with both senior leaders and regulators. Success in this field relies on a combination of sharp analytical skills and a deep understanding of how funding and market liquidity behave under pressure. For those ready to dive in, the career path is challenging but full of opportunity.

Steps to Start a Career in Liquidity Risk Management

If you're looking to break into this field, here’s a practical roadmap to get started:

- Master Basel III requirements: Familiarize yourself with the Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR). These frameworks are critical for understanding how institutions manage funding structures and prepare for stress scenarios.

- Develop quantitative and technical expertise: Learn techniques like cash-flow projection and liquidity-adjusted Value-at-Risk (L-VaR) modeling. Also, get hands-on experience with tools like Moody's Risk Authority, Murex, or Calypso.

- Earn a professional certification: Certifications such as the FRM (Financial Risk Manager) or CFA (Chartered Financial Analyst) are highly respected. With over 71,000 FRM-certified professionals and 180,000 CFA charterholders globally, these credentials can give you a competitive edge.

- Gain early experience: Internships in a bank’s risk or treasury department are invaluable. They not only provide practical exposure but also pave the way for full-time roles.

Future Outlook for Liquidity Risk Managers

The demand for liquidity risk professionals is on the rise. By 2028, global private credit assets under management are expected to hit $3 trillion, creating new challenges in markets that often lack transparency. This will increase the need for experts who can navigate these complexities. Additionally, 41% of Chief Risk Officers plan to allocate more than half of their technology budgets to automation and real-time tracking tools.

With AI taking over routine tasks, the role of liquidity risk managers is shifting toward strategic decision-making. As Mykhailo Kulakov of Epicflow explains:

"The future of risk management in the digital era lies in building a holistic understanding of risk profiles and implementing AI-first analytical systems with humans in the loop."

For those with the right skills, the career potential is impressive. Entry-level analysts in the U.S. can earn base salaries around $60,000, while Chief Risk Officers can see total compensation soar to $700,000. The responsibilities discussed in this article - stress testing, regulatory reporting, and stakeholder communication - are not just essential today but will remain crucial as the field continues to evolve with new challenges and technologies.

FAQs

How do LCR and NSFR differ in practice?

The Liquidity Coverage Ratio (LCR) ensures that banks maintain enough high-quality liquid assets (HQLA) to survive a 30-day period of significant financial stress. Its focus is on short-term resilience, helping banks manage immediate liquidity demands.

On the other hand, the Net Stable Funding Ratio (NSFR) assesses whether banks have adequate stable funding to support their operations and assets over a one-year timeframe. This metric encourages banks to make funding choices that align with long-term stability.

In essence, while the LCR is about handling short-term liquidity crises, the NSFR influences broader, strategic funding decisions for lasting financial health.

What are the first 3 skills to learn for this role?

To thrive as a Liquidity Risk Manager, you’ll need a blend of technical expertise and practical experience. Here are three critical skills for success in this role:

- Deep knowledge of funding markets and cash flow management: Understanding how funding markets operate, managing collateral effectively, and grasping cash flow dynamics are essential for navigating liquidity challenges.

- Regulatory interpretation and application: The ability to analyze complex regulations and seamlessly integrate them into day-to-day operations is a must. This ensures compliance while maintaining operational efficiency.

- Experience with liquidity stress testing: Hands-on involvement in designing and executing liquidity stress tests is crucial. This skill helps in assessing potential risks and preparing for adverse scenarios.

Mastering these areas lays the groundwork for excelling in liquidity risk management.

How do you break into liquidity risk with no experience?

If you're looking to break into liquidity risk management without prior experience, the key is to focus on developing the right skills and knowledge. Start by earning a degree in a related field like finance, economics, or risk management. To further showcase your expertise, consider pursuing certifications such as the CFA (Chartered Financial Analyst) or FRM (Financial Risk Manager).

Practical experience also plays a big role. Seek out internships or entry-level positions in areas like financial analysis or compliance. These roles can give you hands-on exposure to the financial industry and help you build a solid foundation.

Lastly, networking is essential. Connect with professionals in the field to learn from their experiences and uncover potential opportunities. A strong grasp of liquidity risk concepts and financial regulations will make you stand out as a candidate.