If you're trading futures, you could be paying less in taxes thanks to the 60/40 tax rule under IRS Section 1256. Here's the key takeaway: 60% of your profits are taxed at the lower long-term capital gains rate, and 40% at the higher short-term rate - no matter how long you hold the trade. This can significantly reduce your tax burden compared to stock day trading, where 100% of gains are taxed as short-term income.

For instance:

- A trader in the highest tax bracket (37%) pays 26.8% on futures gains instead of 37%, saving 10.2%.

- A $100,000 profit from futures trading would result in a $26,800 tax bill compared to $37,000 for stocks - a savings of $10,200.

This tax treatment applies to Section 1256 contracts like equity index futures (e.g., /ES, /NQ), commodity futures (e.g., /GC, /CL), and broad-based index options (e.g., SPX, VIX). However, it excludes ETF options (e.g., SPY), individual stock options, and cryptocurrencies.

The IRS simplifies reporting with mark-to-market accounting, taxing unrealized gains at year-end but adjusting the cost basis to avoid double taxation. To take advantage of this, use Form 6781 when filing your taxes.

Key benefits include:

- Lower blended tax rates

- No holding period required for long-term rates

- Loss carryback for up to 3 years

- Exemption from wash sale rules

However, you'll owe taxes on unrealized gains, and not all states follow the federal rules (e.g., California taxes futures gains as ordinary income). By focusing on qualifying instruments and consulting a tax professional, you can maximize these savings while staying compliant.

What Is the 60/40 Tax Rule?

The 60/40 tax rule, outlined in Section 1256 of the Internal Revenue Code, divides trading profits into two parts for tax purposes: 60% taxed as long-term capital gains and 40% taxed as short-term capital gains - regardless of how long the asset is held.

This rule applies exclusively to Section 1256 contracts, which include derivatives like futures (e.g., /ES or /NQ), commodity contracts (e.g., /CL or /GC), and broad-based index options (e.g., SPX, VIX, or RUT). Unlike traditional equity trading, which requires holding an asset for over a year to qualify for long-term capital gains, the 60/40 split is applied automatically to these contracts.

Let’s take a closer look at what qualifies as a Section 1256 contract.

Section 1256 Contracts Explained

Not all trading instruments fall under the 60/40 tax treatment. Section 1256 contracts are derivatives traded on IRS-approved exchanges, including regulated futures contracts, certain options, and specific foreign currency contracts.

Here’s a breakdown of what qualifies:

| Contract Type | Examples | Section 1256 Qualified? |

|---|---|---|

| Equity Index Futures | /ES (S&P 500), /NQ (Nasdaq 100) | Yes |

| Commodity Futures | /CL (Crude Oil), /GC (Gold) | Yes |

| Broad-Based Index Options | SPX, VIX, RUT, NDX | Yes |

| Options on Futures | Options on /ES or /GC | Yes |

| ETF Options | SPY, QQQ, IWM options | No |

| Equity Options | AAPL, TSLA, NVDA options | No |

A key distinction lies between broad-based and narrow-based instruments. For example, options on broad-based indices like SPX qualify for Section 1256 treatment, while options on ETFs like SPY do not. Similarly, individual stock options (e.g., Apple or Tesla) and most spot forex trades are excluded. Cryptocurrency, when treated as property, also doesn’t qualify.

There’s one notable exception: futures contracts used for hedging business transactions. These are treated as ordinary income or loss and don’t benefit from the 60/40 split. To qualify as a hedge, the transaction must be properly identified by the end of the trading day.

Now that the qualifying instruments are clear, let’s discuss how the 60/40 split impacts taxation.

How the 60/40 Split Is Applied

The 60/40 tax split often results in a lower effective tax rate than the standard short-term capital gains rate. Here’s how it works:

- 60% of gains are taxed at the long-term capital gains rate (0%, 15%, or 20%, depending on your income).

- 40% of gains are taxed at your ordinary income rate (which can go up to 37%).

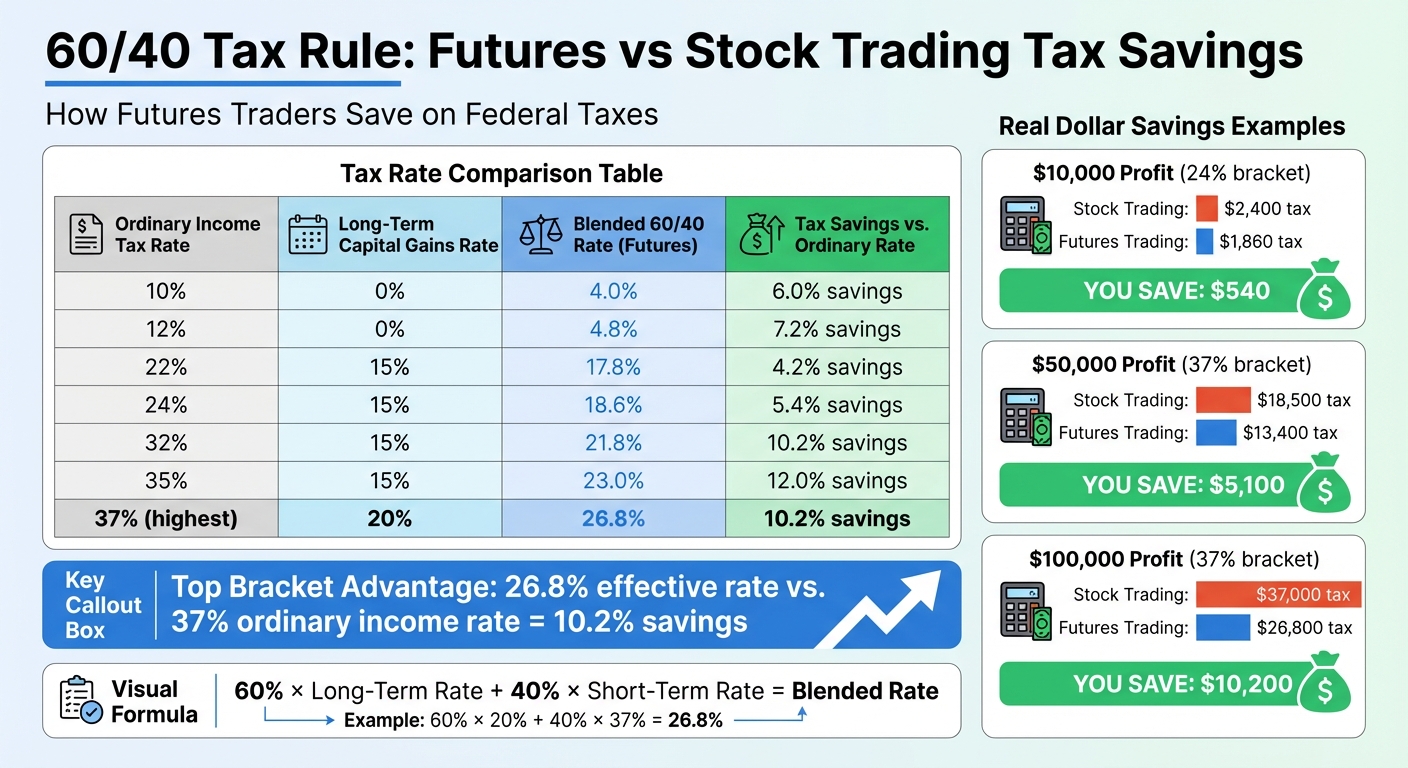

For example, if you’re in the highest tax bracket (where the long-term rate is 20%), the blended tax rate comes to 26.8%. This is significantly lower than the 37% you’d pay on short-term gains alone. The calculation looks like this:

- 60% taxed at 20% = 12%

- 40% taxed at 37% = 14.8%

- Total blended rate = 26.8%

Run 24/7 while you sleep. Keep bots, platforms, and trade copiers online on a dedicated VPS.

Low-latency VPS hosting for your trading platform.

From $59.99/mo

This difference translates to a 10.2% savings compared to being taxed entirely at the short-term rate.

The IRS simplifies this process with Form 6781, which automatically applies the 60/40 split. The results are then transferred to Schedule D for final tax reporting.

Another unique feature of Section 1256 contracts is mark-to-market (MTM) accounting. At the end of each year, all open positions are treated as if they were sold at their fair market value. This means you may owe taxes on unrealized gains, even if you haven’t closed the position. However, your cost basis is adjusted to the fair market value to ensure no double taxation occurs when the position is eventually liquidated.

60/40 Rule vs. Standard Capital Gains Tax Rates

60/40 Tax Rule Savings: Futures vs Stock Trading Tax Rates by Income Bracket

For traders in the top tax bracket, futures trading offers a significant advantage: an effective federal tax rate of 26.8% compared to the 37% rate applied to short-term stock gains. This results in a 10.2 percentage point tax savings on profits.

Unlike stock day traders, who are taxed at ordinary income rates on 100% of their gains, futures traders automatically benefit from the 60/40 split. This becomes even more appealing as income levels rise, making futures trading particularly attractive for high-income, active traders.

Let’s break it down further with real-world examples to see how these tax benefits translate into actual savings.

Blended Tax Rate Examples

Here are a few scenarios that showcase the tax advantages of the 60/40 rule:

- A trader earning $50,000 in annual profits would pay $18,500 in taxes at the top 37% rate when day trading stocks. However, the same profit from futures trading would result in a tax bill of just $13,400, saving $5,100.

- For $100,000 in profits, the difference grows. A top-bracket trader would owe $37,000 in taxes on short-term stock trading but only $26,800 on futures trading. That’s a $10,200 savings.

- Even in lower tax brackets, the benefits are evident. A trader with $10,000 in profits in the 24% bracket would pay $2,400 in taxes on stock gains but only $1,860 on futures, saving $540.

As Kazi Mezanur Rahman, Founder of DayTradingToolkit.com, puts it:

"The built-in tax efficiency is a powerful edge that stock traders simply don't have for short-term trading."

Tax Rate Comparison by Income Bracket

The table below compares blended tax rates and potential savings across various income brackets. For the lowest brackets (10% and 12%), the 60% portion taxed at the long-term capital gains rate (0%) significantly reduces the overall blended rate.

| Ordinary Income Rate | Long-Term Cap. Gains Rate | 40% Short-Term Portion | 60% Long-Term Portion | Blended 60/40 Rate | Tax Savings vs. Ordinary Rate |

|---|---|---|---|---|---|

| 10% | 0% | 4.0% | 0% | 4.0% | 6.0% |

| 12% | 0% | 4.8% | 0% | 4.8% | 7.2% |

| 22% | 15% | 8.8% | 9.0% | 17.8% | 4.2% |

| 24% | 15% | 9.6% | 9.0% | 18.6% | 5.4% |

| 32% | 15% | 12.8% | 9.0% | 21.8% | 10.2% |

| 35% | 15% | 14.0% | 9.0% | 23.0% | 12.0% |

| 37% | 20% | 14.8% | 12.0% | 26.8% | 10.2% |

Tax savings range from 4.2% in the 22% bracket to as much as 12.0% in the 35% bracket. These differences represent money that stays in your pocket rather than going to the IRS.

Example: Calculating Taxes on $50,000 in Futures Gains

Let’s break this down: Imagine $50,000 in net futures gains for the year, which includes both realized profits and mark-to-market unrealized gains.

For a trader in the top 37% tax bracket, here's how it works:

- Long-Term Portion (60%): $30,000 taxed at 20% results in $6,000.

- Short-Term Portion (40%): $20,000 taxed at 37% results in $7,400.

The combined federal tax comes to $13,400, which translates to an effective tax rate of 26.8%.

Now, compare this to stock day trading, which would result in $18,500 in taxes on the same $50,000. Thanks to the 60/40 rule, you save an extra $5,100.

Even traders in the 24% tax bracket see benefits. For example, with a 15% long-term capital gains rate:

- Long-Term Portion: $30,000 × 15% = $4,500

- Short-Term Portion: $20,000 × 24% = $4,800

This totals $9,300 in taxes. Without the 60/40 rule, the tax would be $12,000, meaning a savings of $2,700.

These examples show how the 60/40 rule can offer meaningful tax advantages, especially for traders in higher tax brackets.

How to Report Futures Gains on Your Tax Return

If you're taking advantage of the 60/40 tax treatment, here's how to ensure your futures gains are reported correctly on your tax return.

Start by using IRS Form 6781, officially titled "Gains and Losses From Section 1256 Contracts and Straddles." This form is essential for applying the 60/40 tax split to your Section 1256 contracts.

Form 6781 follows a mark-to-market accounting method, meaning open positions are treated as if they were sold at the end of the year. This means you'll report both profits from closed trades and any gains or losses from positions held as of December 31.

"You report gains as if sold at year-end, splitting them 60% long-term and 40% short-term." - Jacob Dayan, CEO, Community Tax, LLC

After completing Form 6781, the net totals are transferred to Schedule D of your Form 1040. Specifically, the 40% short-term portion is recorded on Line 4, while the 60% long-term portion goes on Line 11. Below is a guide to completing Form 6781 step by step.

Completing IRS Form 6781

Start with Part I, where you report your Section 1256 contracts. Use the data from your broker's Form 1099-B (Box 11) to enter your total Section 1256 profit or loss. Be sure to include unrealized gains or losses from contracts still open on December 31, meeting the mark-to-market requirement.

For instance, suppose a trader purchases a futures contract for $25,000 in May 2024. By December 31, the contract's value increases to $29,000, creating a $4,000 mark-to-market gain. This gain is split into $2,400 long-term and $1,600 short-term on Form 6781. If the contract is sold in January 2025 for $28,000, the earlier recognized gain adjusts the new loss to $1,000, divided as $600 long-term and $400 short-term.

Pay close attention to basis adjustments to avoid being taxed twice on the same gains.

Here are two common pitfalls to avoid:

- Don’t duplicate Section 1256 gains on Form 8949. This form is designed for stocks and bonds, not futures contracts.

- If you have a net loss, consider carrying it back. You can offset Section 1256 gains from the previous three years by checking Box D on Form 6781.

"That double count on Form 8949 shows up more often than you would expect, and Pub 550 is your anchor for the correct mapping." - Accountably

Lastly, keep detailed records of the pricing sources you use for year-end valuations of open contracts. These figures are critical for the fair market value calculations in Part I and can be invaluable if you're audited.

Benefits and Drawbacks of the 60/40 Tax Rule

Stay online and closer to execution. Choose a VPS location for CME futures, New York markets, London FX, API trading, and more.

Host your platform near the market route that matters.

From $59.99/mo

The 60/40 tax rule can lower your overall tax burden, but it comes with specific requirements that may not suit every trader. Understanding its advantages and limitations can help you decide if it aligns with your trading strategy.

Benefits of 60/40 Tax Treatment

One of the standout advantages is the reduced blended tax rate. For instance, if you're in the 37% ordinary income tax bracket, the 60/40 rule can bring your effective tax rate on short-term gains down to about 26.8%. To put it into perspective, a $10,000 profit for a trader in the 24% tax bracket would result in roughly $2,400 in taxes on stocks but only around $1,860 on futures, saving about $540.

"The 60/40 rule is the primary tax advantage of Section 1256 contracts, especially for short-term traders."

- DayTradingToolkit.com

Another benefit is the immediate application of the 60/40 split - there’s no need to hold assets for a year to qualify, making it ideal for day traders and scalpers.

The loss carryback provision is another advantage, allowing traders to offset net Section 1256 losses against gains from the prior three years. This can even lead to a quick tax refund.

Moreover, Section 1256 contracts are not subject to the wash sale rule. This means you can sell a position at a loss and immediately repurchase the same contract without losing the ability to claim that loss on your taxes.

Despite these perks, there are some strict rules and limitations that could impact your trading finances and tax planning.

Drawbacks of 60/40 Tax Treatment

While the 60/40 rule offers tax savings, it comes with challenges that traders need to consider.

One major drawback is the requirement for mandatory mark-to-market accounting. On December 31, any open positions are treated as if they were sold at fair market value, meaning you may owe taxes on unrealized gains.

"The mandatory mark-to-market rule means you may owe taxes on 'paper gains' even if you haven't closed your position."

This can create cash flow issues, as you’ll need to have enough cash on hand at year-end to cover potential tax liabilities, even if you haven’t realized those gains.

Another limitation is that the 60/40 treatment is non-optional. Once you qualify, you’re required to follow it - even in years when it may not work in your favor. Additionally, only specific assets qualify for this rule. Regulated futures and broad-based index options (like SPX) are eligible, but individual stocks, ETF options (such as SPY or QQQ), and most spot cryptocurrencies are excluded.

Lastly, not all states follow the federal 60/40 split. For example, California taxes futures gains as ordinary income, which could negate the federal tax benefits.

Benefits vs. Drawbacks Comparison

| Benefits | Drawbacks |

|---|---|

| Lower Tax Rate: 60% of gains taxed at long-term rates (up to 20%) | Tax on Paper Gains: Year-end mark-to-market creates tax liability on unrealized profits |

| Immediate Application: No holding period required, even for short-term trades | Limited Scope: Excludes individual stocks, ETFs, and cryptocurrencies |

| Loss Carryback: Offset losses against prior three years' gains | State Variations: Some states (e.g., CA) tax gains as ordinary income |

| No Wash Sale Rules: Losses can be claimed even with immediate repurchase | Mandatory Rule: Cannot opt out if conditions are unfavorable |

Carefully weighing these pros and cons is essential for traders looking to optimize their tax strategy while managing cash flow effectively.

How to Reduce Your Tax Bill with the 60/40 Rule

The 60/40 tax rule offers a unique opportunity to cut your tax bill, but how you approach it can make all the difference. By carefully choosing the right trading contracts and working with knowledgeable tax professionals, you can maximize these savings.

Trade Timing and Contract Selection

The type of trading instrument you use plays a big role in your tax liability. For example, switching from SPY to SPX options can qualify your trades for 60/40 treatment. SPX options fall under Section 1256 contracts, which means they enjoy a more favorable tax split, while SPY options do not - leading to significantly different tax outcomes, even for similar trades.

Cryptocurrency traders can also take advantage of the 60/40 split by focusing on CME Bitcoin futures (/BTC) or Ethereum futures (/ETH) instead of trading spot crypto on retail exchanges. Spot crypto is taxed as property by the IRS, which doesn’t allow for the same benefits.

Another perk of Section 1256 contracts is their exemption from the wash sale rule. This means you can harvest losses at the end of the year without waiting the usual 30 days to repurchase the same security. To maximize this benefit, make sure to harvest your losses before December 31. If needed, you can even use Form 1045 to carry back Section 1256 losses and claim a quick tax refund.

These strategies are essential building blocks for reducing your tax burden, but professional guidance can take your planning to the next level.

Working with Tax Professionals

Navigating the specifics of Section 1256 contracts and futures trading tax rules can be tricky, which is why it’s crucial to find the right expert. A Certified Public Accountant (CPA) or Enrolled Agent (EA) with experience in trader taxes can make a world of difference.

"CPAs specializing in trader taxes understand the futures trading tax rate nuances most general practitioners miss."

- Kelly Watson, Cloudzy

A tax professional can help in several key areas. They can model how state taxes will affect your overall liability, guide you through complex elections like Mixed Straddles, and determine if you qualify for Trader Tax Status (TTS). TTS can allow you to deduct certain business expenses on Schedule C, adding another layer of savings.

Perhaps most importantly, an experienced advisor can help you plan ahead for the April tax bill. They’ll ensure you have enough cash set aside to cover taxes on mark-to-market gains without disrupting your trading capital. By combining these strategies with professional advice, you can make the most of the 60/40 rule.

Summary

The 60/40 tax rule offers futures traders a notable federal tax advantage. Thanks to Section 1256, gains are taxed with a 60% long-term and 40% short-term rate split, regardless of how long the position is held - even intraday trades qualify for this treatment.

For high-income traders in the 37% tax bracket, this translates to an effective tax rate of about 26.8%, saving approximately 10.2%. That’s a reduction of $10,200 on a $100,000 profit.

Section 1256 contracts also simplify tax reporting by consolidating gains and losses on Form 6781. Additional benefits include wash sale exemptions and the ability to carry back losses to offset prior gains.

To maximize these savings, focus on qualifying instruments like regulated futures contracts and broad-based index options. However, keep in mind that mark-to-market accounting applies to unrealized gains as of December 31, so managing liquidity is critical.

Ultimately, choosing the right contracts and planning ahead can significantly lower your tax bill. For example, switching from SPY to SPX options or using CME Bitcoin futures instead of spot cryptocurrency can make a big difference. Consulting a seasoned trader tax professional ensures you take full advantage of these benefits while staying compliant with IRS regulations.

FAQs

Which trades qualify for 60/40 tax treatment?

Certain trades fall under the 60/40 tax treatment, offering a favorable tax split: 60% taxed as long-term capital gains and 40% as short-term capital gains. These are outlined in IRC Section 1256 and include:

- Regulated futures contracts

- Foreign currency contracts traded on regulated exchanges

- Non-equity options on futures, commodities, currencies, and broad-based stock indices

This setup can provide a tax advantage compared to other types of trading income.

How does year-end mark-to-market affect my tax bill?

Year-end mark-to-market treatment means traders must calculate their gains and losses as if all open positions were sold at their fair market value on the last day of the year. This process can increase taxable income, which might lead to a higher tax bill for that year. Knowing how this rule works is essential for proper tax planning and staying compliant with tax regulations.

What’s the easiest way to report Section 1256 gains and losses?

The simplest way to handle Section 1256 gains and losses is by using Form 6781, which is tailored for these types of contracts. Here's how it works: mark all open positions to market at the end of the year, calculate the net gain or loss, and then divide it into 60% long-term and 40% short-term capital gains. Once you've done this, the result from Form 6781 gets transferred to Schedule D on your tax return.