Physical delivery in futures trading means the actual transfer of a commodity or asset when a contract expires. While most retail traders avoid it, commercial participants like farmers or manufacturers rely on it to secure physical goods. Here's what you need to know:

- What Happens: Sellers deliver the asset (e.g., oil, gold, corn) to buyers at a specified location. Buyers pay the full contract value.

- Key Dates: Pay attention to the First Notice Day (FND) - the first day sellers can declare delivery intent. Close or roll positions before this date to avoid delivery.

- Who Uses It: Commercial hedgers need physical delivery; speculators typically close trades early to avoid logistical challenges.

- Why It Matters: Physical delivery ensures futures prices align with spot market prices, maintaining market integrity.

- Challenges: Includes storage, transportation, quality checks, and full payment for the asset.

If you're trading futures, understanding whether a contract settles in cash or physical delivery is crucial. Always check the contract's specifications to avoid surprises.

What Is Physical Delivery in Futures?

Definition and Why It Matters

Physical delivery in futures means the actual transfer of the underlying asset from the seller to the buyer on a specified date, rather than settling the contract in cash. This process plays a key role in keeping futures prices closely aligned with spot market prices. As a contract nears expiration, the futures price converges with the spot price because arbitrageurs take advantage of any price discrepancies. This alignment is crucial for understanding settlement options.

Exchanges oversee every detail of physical delivery, including quality standards, delivery locations, and grading requirements, to ensure consistency. For instance, gold bars must meet a purity standard of 99.5% and weigh 400 troy ounces. Similarly, crude oil futures are delivered to specific storage facilities in Cushing, Oklahoma. This standardization gives commercial participants - like farmers, manufacturers, and airlines - the ability to secure inventory and manage supply chain costs with certainty.

While speculators typically close their positions before expiration to avoid the logistical challenges of physical delivery, this mechanism is vital for commercial hedgers who need the actual commodity. For example, a single WTI Crude Oil futures contract represents 1,000 barrels of oil, while a gold futures contract equals 100 troy ounces. These contracts are not just financial tools - they are binding agreements for the exchange of real goods.

Now, let’s compare physical delivery with cash settlement to better understand their practical differences.

Physical Delivery vs. Cash Settlement

Cash settlement provides a more straightforward alternative. Instead of transferring physical goods, the contract is settled with a net cash payment based on the difference between the entry price and the final settlement price. This means no need for warehouses, transportation, or quality inspections - just a simple adjustment to your margin account.

Here’s a comparison of the two settlement methods:

| Feature | Physical Delivery | Cash Settlement |

|---|---|---|

| Final Result | Actual transfer of physical goods | Financial credit/debit to account |

| Primary Users | Commercial hedgers and producers | Speculators and retail traders |

| Logistics | Requires storage, transport, and inspection | No logistical requirements |

| Margin Cost | Higher (approx. 10% of notional value) | Lower (approx. 5% of notional value) |

| Typical Assets | Crude oil, corn, gold, wheat, cattle | Stock indices, interest rates, crypto |

One notable difference is the initial vs. maintenance margin requirements. Physically delivered contracts generally demand about 10% of the contract's notional value as initial margin, reflecting the added complexity of handling real commodities. In contrast, cash-settled contracts often require only around 5%. Before trading, it’s essential to check whether a contract is labeled "P" for Physical or "C" for Cash Settled.

Run 24/7 while you sleep. Keep bots, platforms, and trade copiers online on a dedicated VPS.

Low-latency VPS hosting for your trading platform.

From $59.99/mo

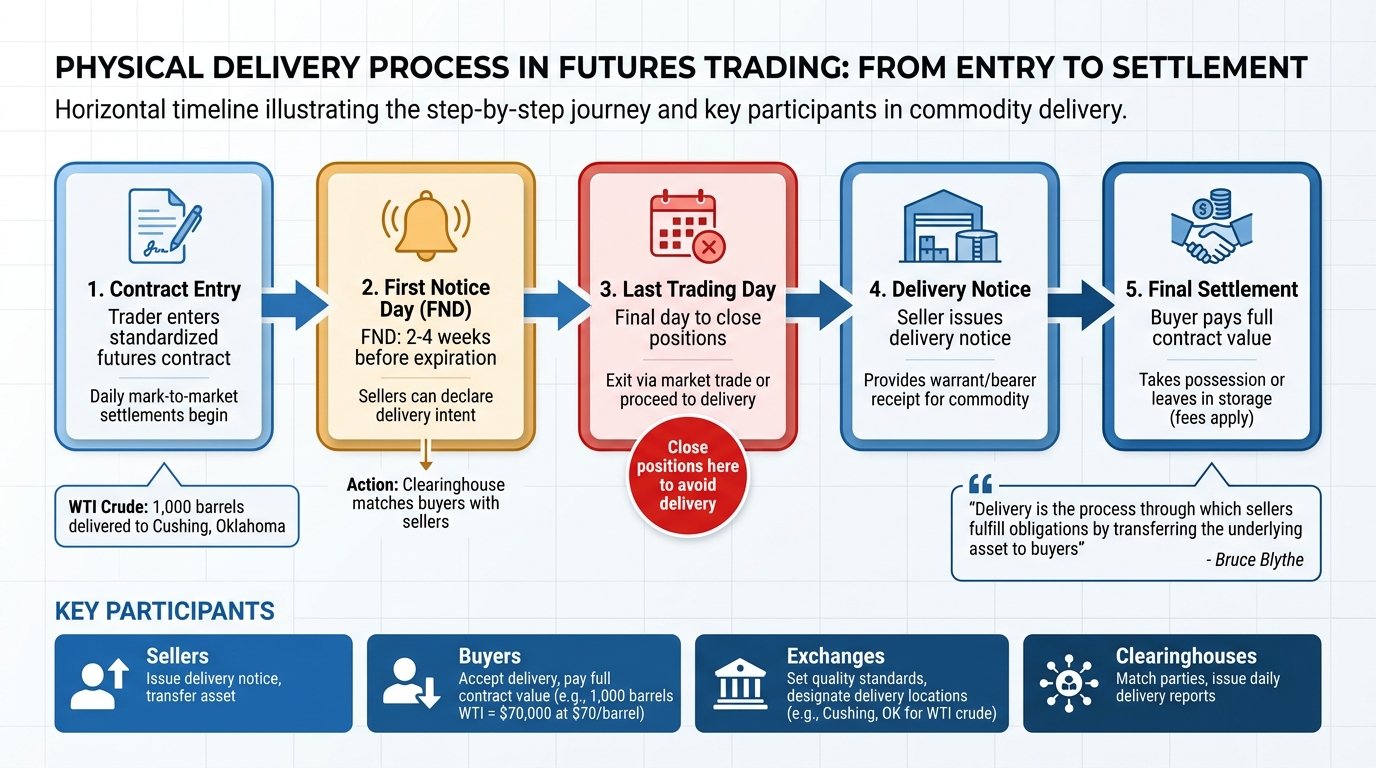

How Physical Delivery Works: Step-by-Step

Physical Delivery in Futures Trading: Complete Timeline and Process Flow

Timeline and Key Dates

Physical delivery in futures trading follows a carefully organized timeline, established by exchanges like CME and NYMEX. This process begins when traders enter into standardized futures contracts and continues with daily mark-to-market settlements, which help manage both margin requirements and delivery obligations.

The process kicks into high gear around the First Notice Day (FND) - typically two to four weeks before the contract expires. On this day, the clearinghouse notifies traders that they may need to either make or take delivery. Sellers signal their intent to deliver by issuing a delivery notice, and the clearinghouse matches these sellers with buyers holding long positions.

The Last Trading Day is the final chance for traders to close their positions through market trades. Any contracts still open after this point must go through physical settlement. For the seller, this means providing a warrant or bearer receipt that represents the agreed-upon quantity and quality of the commodity at a designated storage facility. The buyer, in turn, pays the full contract value.

This structured timeline ensures all parties know their responsibilities and deadlines, making the entire process run smoothly.

What Buyers, Sellers, and Exchanges Do

Each participant in the futures market has a specific role in the physical delivery process:

- Sellers holding short positions must issue a delivery notice as the contract nears expiration. This confirms their intent to deliver the asset.

- Buyers holding long positions are required to accept delivery and pay the full value of the contract. For example, a West Texas Intermediate (WTI) crude oil futures contract involves taking delivery of 1,000 barrels of oil.

Exchanges play a key role by setting quality standards, defining acceptable grades, and designating approved delivery locations. For instance, WTI crude oil is delivered to storage facilities in Cushing, Oklahoma, while agricultural commodities are delivered to licensed grain depots near Chicago or along the Illinois River.

Clearinghouses act as intermediaries, matching buyers with sellers and issuing daily delivery reports throughout the delivery period. Clearing brokers handle the final settlement process right after the last trading day.

This well-defined system ensures efficiency and clarity, as highlighted by Bruce Blythe:

"Delivery is the process through which sellers of futures contracts fulfill their obligations by transferring the underlying asset to buyers, who must accept and pay for it."

- Bruce Blythe, Financial Journalist

Once the buyer receives the warrant, they have two options: take physical possession of the commodity (which involves transportation costs) or leave it in storage for a fee. This flexibility allows buyers to manage their assets based on their needs and logistical considerations.

Physical Delivery Examples

Crude Oil Delivery

A single West Texas Intermediate (WTI) crude oil futures contract represents 1,000 barrels of oil. When physical delivery takes place, the process centers around Cushing, Oklahoma - an important pricing and storage hub for the CME Group.

Delivery is facilitated through a warrant or bearer receipt, which serves as proof of ownership for a specific quantity and grade of oil stored at an approved facility. To maintain consistency, the exchange enforces strict quality standards, ensuring all contracts deliver the same grade of crude oil.

Once the buyer receives the warrant, they have two options: leave the oil in storage (paying ongoing storage fees) or arrange transportation to move it elsewhere. Transportation costs fall on the buyer, making physical delivery impractical for most retail traders. Access to pipelines or storage facilities at the delivery point is essential, which is why this method is primarily used by commercial entities like refineries and oil producers.

For example, at a price of $70 per barrel, one WTI contract equates to a notional value of $70,000. To take physical delivery, the buyer must pay this full amount. This high cost explains why speculators usually exit their positions before First Notice Day, leaving physical delivery to those with operational needs.

Agricultural Commodities Delivery

Agricultural commodities, such as corn and soybeans, follow a comparable delivery process but involve different logistics. For instance, a standard soybean futures contract represents 5,000 bushels, with deliveries typically occurring at licensed grain storage facilities near Chicago or along the Illinois River.

Quality control is a key factor in agricultural deliveries. Take wheat as an example - it must meet the USDA's No. 2 hard red winter standard, which includes specific criteria for moisture and protein content. These standards are regulated by the exchange to ensure uniformity across contracts.

Thirty days before a contract expires, delivery notices are issued, specifying the quantity, location, and quality of the commodity. Once the warrant transfers to the buyer, they can either keep the goods in storage for a periodic fee or arrange transportation to another location.

Stay online and closer to execution. Choose a VPS location for CME futures, New York markets, London FX, API trading, and more.

Host your platform near the market route that matters.

From $59.99/mo

This standardized approach ensures consistency in both quality and logistics across agricultural contracts, much like in crude oil delivery.

Risks, How to Avoid Delivery, and Trading Considerations

Risks of Physical Delivery

Physical delivery in futures trading can pose significant challenges, especially for traders who aren't prepared. One of the biggest hurdles is the full capital requirement. Unlike trading on margin, taking delivery means paying the total value of the underlying asset. For instance, gold futures demand a significant financial commitment due to their high notional values.

As contracts near expiration, liquidity typically dries up because professional traders roll their positions forward. This reduced liquidity often leads to wider bid-ask spreads and more volatile prices, making it harder to exit positions favorably. On top of that, traders must deal with storage costs, transportation fees, and potential disputes over the quality of the delivered asset. Brokers may also impose hefty logistical fees or, worse, liquidate positions at less-than-ideal prices when delivery obligations are triggered.

How to Avoid Physical Delivery

To sidestep the complications of physical delivery, it's crucial to act before the First Notice Day (FND). This is the first date when sellers can notify their intent to deliver the underlying commodity. Long holders should close or roll their positions before this date.

"First notice day (FND) marks the date when holders of long futures contracts can first be required to take delivery of the underlying commodity." - Investopedia

One effective method is to exit positions at least two days before FND. This provides a buffer to correct any trade errors. Another option is to roll contracts forward - this involves closing the expiring contract and opening a new one for a later month. This approach helps maintain market exposure while avoiding delivery obligations.

For traders who want to completely bypass these logistical hurdles, cash-settled contracts are an excellent alternative. Products like the S&P 500 E-mini or Micro energy futures settle financially, eliminating the need for physical delivery. Always check the contract specifications - look for "C" to confirm cash settlement or "P" for physical delivery - before entering a trade.

Trading Implications and Technology Tools

Managing these risks requires efficient execution tools, especially as expiration approaches and liquidity becomes scarce. Speed is critical in this scenario. Automated trading alerts and low-latency execution systems can make the difference between exiting smoothly and being stuck with unwanted delivery obligations.

For example, low-latency VPS solutions like QuantVPS allow traders to execute time-sensitive trades almost instantly, reducing the risk of being caught in illiquid markets near FND. Setting up automated alerts for FND and the last trading day is another way to ensure timely rollovers. While many retail brokers automatically liquidate positions before FND, relying solely on this safeguard can lead to trades being executed at unfavorable prices. Advanced tools and proactive strategies are essential for navigating these challenges effectively.

Conclusion

This guide has broken down the essentials of physical delivery in futures contracts. In this process, the actual asset - be it 1,000 barrels of crude oil, 5,000 bushels of corn, or 100 troy ounces of gold - is transferred between parties, often involving high notional values. For commercial hedgers like farmers or manufacturers, this mechanism is a practical way to secure necessary commodities. However, for retail speculators, the logistical demands of storage, transportation, and quality checks make physical delivery far less practical.

These challenges emphasize the need for careful planning and the right tools to navigate futures trading effectively. One critical concept is understanding the First Notice Day (FND) - the earliest point at which a seller can declare their intent to deliver. Traders should always verify whether contracts are designated "C" for cash settlement or "P" for physical delivery before entering a trade.

As expiration approaches, timing becomes crucial. Leveraging low-latency tools like QuantVPS can help avoid slippage and steer clear of unintended delivery obligations.

FAQs

What happens if I hold a futures contract past First Notice Day?

If you keep a futures contract beyond its First Notice Day, you're obligated to either deliver or accept delivery of the underlying asset. At this point, the contract progresses toward settlement, and for contracts requiring physical delivery, you'll need to meet the terms specified in the agreement.

How do I know if a futures contract is cash-settled or physically delivered?

To figure out if a futures contract is cash-settled or physically delivered, take a close look at its contract specifications. Here's the difference:

- Physically delivered contracts: These involve the actual transfer of the underlying asset when the contract expires.

- Cash-settled contracts: Instead of exchanging the asset, these are settled by paying the price difference in cash.

You'll find the settlement method clearly outlined in the contract documentation, so it's worth reviewing those details carefully.

What do I need to take delivery of a commodity like oil or corn?

To take delivery of a commodity in a futures contract, you need to hold a short position as the delivery date approaches and be designated as the deliverer. This involves adhering to the contract's specific requirements, such as the quality, quantity, and delivery location of the commodity. Additionally, you'll need to manage logistics, including transportation and storage arrangements. Coordination with a clearing firm is also essential to ensure the commodity is transferred in line with the agreed-upon terms.