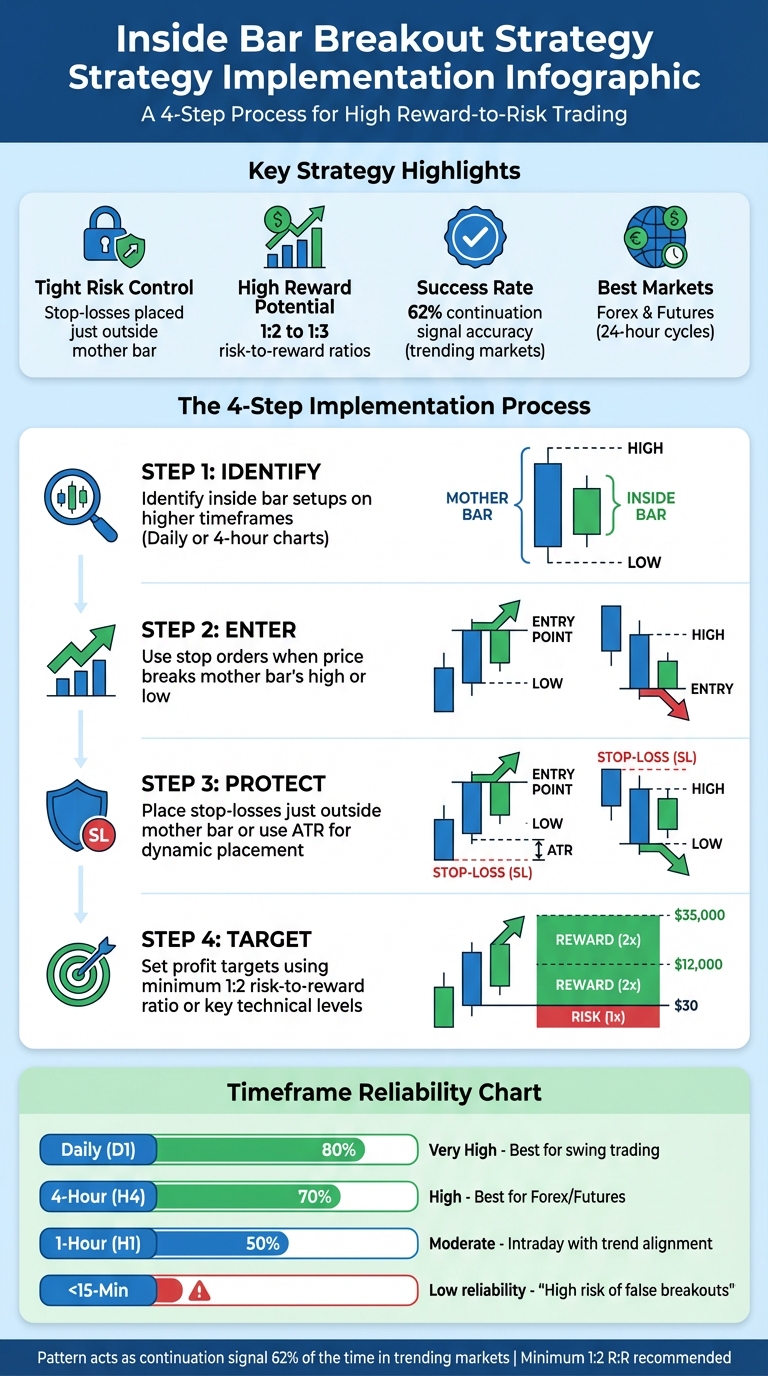

The Inside Bar Breakout strategy is a trading method that focuses on identifying periods of market consolidation, followed by sharp price movements. It uses a two-candle pattern where the second (inside bar) is entirely contained within the range of the first (mother bar). Here's why this strategy stands out:

- Tight Risk Control: Stop-losses are placed just outside the mother bar, minimizing risk.

- High Reward Potential: Traders can target risk-to-reward ratios of 1:2 or 1:3.

- Best Markets: Works well in forex and futures markets due to their 24-hour trading cycles.

- Trend Alignment: Most effective when used in the direction of the prevailing trend, with continuation signals succeeding 62% of the time.

To implement this strategy:

- Identify inside bar setups on higher timeframes (daily or 4-hour charts).

- Use stop orders to enter trades when price breaks the mother bar's high or low.

- Place stop-losses just outside the mother bar or use tools like ATR for dynamic placement.

- Set profit targets using a minimum 1:2 risk-to-reward ratio or key technical levels.

For precise execution, low-latency tools like QuantVPS can help avoid slippage during rapid breakouts. Understanding how to minimize slippage is critical when trading high-volatility patterns. This strategy rewards discipline and careful risk management.

Inside Bar Breakout Strategy: 4-Step Implementation Guide with Risk-Reward Ratios

What Is the Inside Bar Breakout Strategy?

This strategy builds on a simple yet effective two-candle pattern. The second candle, known as the inside bar, forms entirely within the range of the first candle, referred to as the mother bar. Essentially, this pattern reflects a moment of market indecision, where neither buyers nor sellers manage to push prices beyond the mother bar's high or low. Such periods of consolidation often set the stage for a sharp price breakout.

The compact size of the inside bar is particularly appealing to traders because it allows for tight stop-loss placement, just outside the inside bar's range. This often results in favorable risk-to-reward ratios, such as 1:2 or 1:3.

Key Features of the Inside Bar Pattern

The inside bar pattern is defined by its size relationship: the inside bar must stay entirely within the high and low of the mother bar. Occasionally, multiple consecutive inside bars can form within the same mother bar. This "coiling" effect signals intense price compression, which often leads to a strong breakout.

Another hallmark of this pattern is its association with low volatility. It captures a phase where the market is calm, often preceding significant price movement. These clear and distinct features make the inside bar breakout strategy a favorite among traders for its precision and well-defined execution points.

Why Traders Use This Strategy

The Inside Bar Breakout strategy is particularly popular because of its strong risk management capabilities. Since the inside bar is smaller than the mother bar, the distance between the entry point and stop-loss is minimal. This means traders can commit less capital while still targeting meaningful price moves. The strategy’s simplicity - using the mother bar’s high and low as clear entry and exit triggers - adds to its appeal.

Another reason for its popularity is its reliability as a continuation signal. According to Bulkowski's Encyclopedia of Chart Patterns, the inside bar pattern results in trend continuation about 62% of the time. This makes it especially effective for trading in the direction of the prevailing trend, particularly in markets like forex and futures, where 24-hour trading often produces smoother price action.

How to Identify Inside Bar Setups on Charts

Spotting a valid inside bar setup takes more than just noticing two consecutive candles. To effectively use the Inside Bar Breakout strategy, you need to focus on patterns that align with the broader market structure. This strategy works best on higher timeframes, like daily or 4-hour charts, where price action tends to be more reliable. These timeframes help filter out the noise and provide cleaner signals with stronger follow-through.

Step-by-Step Pattern Recognition

Run 24/7 while you sleep. Keep bots, platforms, and trade copiers online on a dedicated VPS.

Low-latency VPS hosting for your trading platform.

From $59.99/mo

Start by identifying a mother bar with a clear range. Then, confirm that the next candle’s high is lower than the mother bar’s high, and its low is higher than the mother bar’s low - this includes the wicks. The inside bar's color doesn’t matter; what’s important is that it stays entirely within the mother bar’s range.

After confirming the pattern, check for key technical levels for added reliability. The most effective setups often appear after a strong directional move in a trending market or near major support and resistance zones. A 20-period moving average can help define the trend. For bullish setups, look for inside bars forming above a rising moving average; for bearish setups, they should form below a falling one. To further validate the setup, use the ADX indicator - readings above 20 to 25 suggest enough trend strength for the breakout to have follow-through.

Mastering these criteria will help you spot variations that can impact the breakout’s strength.

Common Pattern Variations

Some setups include multiple consecutive inside bars, often referred to as "inside-inside" bars or coiling formations. These patterns indicate extreme price compression. When two or three inside bars form in a row, the breakout tends to be more forceful. This coiling effect shows growing uncertainty, which builds pressure for a sharp price move.

Another variation to watch is the Hikkake pattern, where the initial breakout fails and reverses sharply in the opposite direction, trapping early breakout traders. While these false breakouts can be frustrating, recognizing the pattern allows you to avoid premature entries and wait for a confirmed breakout - ideally with a full candle close beyond the mother bar’s range.

Tools for Chart Analysis

Once you’ve identified standard and variant patterns, advanced charting tools can help with real-time confirmation. Platforms like NinjaTrader and MetaTrader offer the tools you need to spot these patterns effectively. These platforms allow you to combine technical indicators such as moving averages, ADX, ATR, and volume on a single screen - critical for accurate pattern identification and tight risk management. Pairing these platforms with services like QuantVPS ensures low-latency connections, allowing for immediate execution when price crosses key levels.

Here’s a breakdown of how reliable different timeframes are for this strategy:

| Timeframe | Reliability | Best Use Case |

|---|---|---|

| Daily (D1) | Very High (~80%) | Swing trading, multi-day trends |

| 4-Hour (H4) | High (~70%) | Forex/Futures, balancing signal frequency and quality |

| 1-Hour (H1) | Moderate (~50%) | Intraday setups with trend alignment |

| < 15-Min | Low | Scalping, high risk of false breakouts |

How to Execute the Inside Bar Breakout Strategy

Once you've identified a valid inside bar setup, the next step is executing your trade with precision. This involves entering at the right moment, protecting your capital with a well-placed stop-loss, and setting profit targets that make the trade worthwhile. Get these elements right, and you'll stand a better chance of trading this pattern successfully.

Where to Enter Breakout Trades

The typical way to enter an inside bar breakout is by using stop orders. For a bullish breakout, place a buy stop just above the mother bar's high. For a bearish breakout, place a sell stop just below the mother bar's low. This approach ensures you're entering the trade only when momentum confirms the breakout direction.

There are two main entry strategies:

- Aggressive Entries: Triggered at the inside bar's high or low. These offer tighter stop-losses and potentially higher reward-to-risk ratios but come with a higher chance of false breakouts.

- Conservative Entries: Triggered at the mother bar's high or low. These provide stronger confirmation of the breakout but require wider stop-losses to accommodate market noise.

To avoid getting caught in minor fluctuations, add a small buffer to your entry level - such as $0.05 to $0.10 for stocks under $50 or a few ticks for other instruments. Additionally, wait for the breakout candle to close fully beyond the mother bar's range for added confirmation. In trending markets, inside bar breakouts have a historical tendency to continue in the trend's direction about 60% to 65% of the time.

Once you've entered your trade, the next critical step is managing your risk with a stop-loss.

How to Place Stop-Losses

Stop-loss placement is essential for managing risk and improving your trade's success rate. The most common method is to place your stop at the opposite end of the mother bar. For long trades, this means setting the stop below the mother bar's low; for short trades, it goes above the mother bar's high. This approach gives your trade enough room to develop without being prematurely stopped out.

For traders looking for tighter risk management, consider these alternatives:

- Place the stop at the 50% level (midpoint) of the mother bar.

- Use the Average True Range (ATR) indicator to place stops 1 ATR away from the inside bar's high or low. This method adjusts for market volatility.

Rayner Teo, Founder of TradingwithRayner, advises:

A better way to set your stop loss is 1 ATR below the low of the Inside Bar (for long trades) - so your trade has more 'breathing room'.

Regardless of the method, always position your stop-loss a few ticks or cents outside the mother bar's range. If your trade moves in your favor by one risk unit (1R), consider moving your stop to breakeven to lock in your capital.

Setting Profit Targets

With your entry and stop-loss in place, it's time to define your profit targets. Aiming for a minimum 1:2 risk-to-reward ratio is a good starting point, but a 1:3 ratio is even better for long-term success.

Here are a few ways to set realistic profit targets:

- Use a measured move: Calculate the range of the mother bar (high minus low) and project that distance from your breakout point.

- Identify the next key support or resistance level on your chart for a natural profit target.

- For more advanced targeting, apply Fibonacci extensions to pinpoint areas beyond immediate technical levels.

As the trade progresses, you can trail your stop-loss behind recent swing lows (for long trades) or swing highs (for short trades). This way, you can lock in profits while staying in the trade to capture larger moves.

| Entry Type | Trigger Level | Stop-Loss Placement | Best Use Case |

|---|---|---|---|

| Aggressive | Inside Bar High/Low | Opposite side of Inside Bar | Strong trending markets |

| Conservative | Mother Bar High/Low | Opposite side of Mother Bar | Choppy or high-volatility markets |

| Trend-Following | Mother Bar High/Low | 1 ATR from 20-period EMA | Pullbacks in established trends |

| Reversal | Mother Bar High/Low | Opposite side of Mother Bar | Key support/resistance levels |

Risk Management Techniques

Identifying breakout patterns is just the beginning - protecting your capital is where the real challenge lies. One of the key strengths of the inside bar strategy is its naturally tight risk. However, to make the most of it, you need to align your stop-loss method with the current market environment and your trading approach. Poor risk management can erode the edge of even the most promising setups. Precision in managing risk is critical to fully harness the potential of breakouts.

Stay online and closer to execution. Choose a VPS location for CME futures, New York markets, London FX, API trading, and more.

Host your platform near the market route that matters.

From $59.99/mo

Stop-Loss Methods for Futures and Forex

Your choice of stop-loss strategy should reflect the market's behavior. In trending markets, aggressive stops placed just outside the inside bar's extremes can provide a tighter risk-to-reward ratio. However, this approach may lead to more frequent stop-outs due to normal price noise.

In contrast, during more volatile or choppy conditions, conservative stops located outside the mother bar's range can give your trade more room to breathe. While this reduces the chances of premature exits, it also requires using smaller position sizes to maintain consistent dollar risk. For long trades, placing stops 1 ATR (Average True Range) below the inside bar's low provides additional breathing space.

High-volatility sessions call for ATR-based stops. By calculating one ATR and placing your stop that distance from the inside bar's extreme, you can dynamically adjust to market fluctuations. This helps you avoid false breakouts, where the price briefly moves beyond the inside bar only to reverse. Another option for trending markets is to position stops one ATR away from the 20-period EMA, as prices often find support or resistance near this level during pullbacks.

One key rule: avoid setting stops within the mother bar's range. Adding a small buffer to account for minor price fluctuations can also help prevent unnecessary stop-outs.

Comparing Risk-Reward Scenarios

Different stop-loss methods create varying risk-reward profiles, and understanding these trade-offs is essential for selecting the right approach for your trades. According to The Encyclopedia of Chart Patterns by Bulkowski, inside bar patterns act as continuation signals in 62% of cases. However, your win rate will depend heavily on your choice of stop-loss method.

| Stop-Loss Method | Risk Level | Market Suitability | Key Advantage | Main Drawback |

|---|---|---|---|---|

| Inside Bar Extreme | High | Strong, fast-moving trends | Tightest stop; best R:R ratio | Frequent stop-outs from price noise |

| Mother Bar Extreme | Moderate | Choppy or volatile markets | Higher win rate; more breathing room | Wider stops require smaller positions |

| ATR-Based Stop | Dynamic | High-volatility environments | Adjusts to market conditions | May exit late during rapid reversals |

| Key Level Buffer | Low | Reversals at major levels | Protects against false breakouts | Requires precise level identification |

The aggressive approach of using inside bar extremes works well when the ADX indicator reads above 20–25, signaling strong trend momentum. In such conditions, inside bar breakouts aligned with the prevailing trend succeed 60% to 65% of the time. However, when the ADX drops below 20, the market is likely ranging. In these cases, it’s better to either skip the trade or use conservative stops based on the mother bar to avoid getting caught in choppy price action.

For consistent results over time, aim for a minimum 1:2 risk-to-reward ratio, no matter which stop-loss method you use. This ensures that one winning trade offsets two losing trades, providing a statistical edge even with a 50% win rate. When you notice multiple consecutive inside bars forming a "coil" pattern, the potential reward can increase significantly. These compressed setups often lead to powerful breakouts, while your stop remains tight at the mother bar's extreme.

Using QuantVPS to Improve Strategy Performance

When it comes to precise risk management, executing orders without delay is absolutely critical. Inside bar breakouts often lead to rapid price movements, meaning any delay in order execution can result in significant slippage. Home internet connections, with delays ranging from 50–200ms, can quickly eat into your trading edge, especially when you're working with tight stops and aiming for pinpoint entries at the extremes of the mother bar.

How Low Latency Improves Breakout Trading

QuantVPS offers 0–1ms latency to major financial venues, with sub-0.52ms direct connectivity to the CME Group exchange. This ultra-low latency ensures that stop orders are triggered instantly when the inside bar range is breached. To put this into perspective, as of April 15, 2026, QuantVPS handled over $12.09 billion in daily futures trading volume, demonstrating its capability to support high-speed breakout trades without any performance bottlenecks.

The platform is powered by cutting-edge hardware, including AMD Ryzen 9 7950X processors and NVMe storage, and operates with a 99.999% uptime guarantee. This setup ensures your automated strategies can monitor inside bar setups 24/7, even if your local computer is offline.

For traders working with CME futures, selecting a Chicago datacenter location places your server close to the exchange’s matching engines. This proximity provides a sub-millisecond advantage, significantly reducing slippage on instruments like the ES or NQ.

These benefits make QuantVPS a strong choice for traders using various strategies, especially those relying on precise execution for inside bar breakouts.

QuantVPS Plans for Different Trading Needs

QuantVPS offers a range of plans designed to support different trading setups, ensuring you have the right infrastructure for your strategy. For simpler setups, such as monitoring 1–2 charts on a single timeframe, the VPS Lite plan is a solid choice. If your strategy involves multiple timeframes - like scanning daily charts for setups while executing on 4-hour or 15-minute charts - higher-tier plans with multi-monitor support are essential.

| Plan | Monthly Cost (Annual) | Cores | RAM | Storage | Monitor Support | Best For |

|---|---|---|---|---|---|---|

| VPS Pro | $69.99 | 6 | 16GB | 150GB NVMe | Up to 2 monitors | For 3–5 charts |

| VPS Ultra | $132.99 | 24 | 64GB | 500GB NVMe | Up to 4 monitors | For 5–7 charts |

| Dedicated Server | $209.99 | 16+ | 128GB | 2TB+ NVMe | Up to 6 monitors | For 7+ charts |

The VPS Pro plan is ideal for traders using platforms like NinjaTrader or Sierra Chart with a few inside bar scanners and basic volume analysis. If your strategy incorporates additional filters - such as ATR-based stops or ADX conditions - across Forex, Futures, and Equities, the VPS Ultra plan provides the extra processing power needed for complex backtesting and real-time data feeds from sources like Rithmic, CQG, or dxFeed. Plus, opting for annual billing can save you around 30% compared to monthly payments, helping you reduce costs while maintaining a competitive low-latency setup.

Conclusion

The strategy outlined combines sharp pattern recognition with strict risk management to create a structured approach to trading. The Inside Bar Breakout strategy offers a clear framework for managing risks tightly while aiming for substantial rewards. By focusing on the mother bar and its corresponding inside bar, waiting for confirmation signals like volume surges or strong candle closes, and aligning trades with the overall trend, traders can avoid false breakouts and zero in on setups with higher probabilities of success. Daily inside bars are particularly valued for their reliability, while 4-hour charts strike a balance between signal quality and trading frequency.

From identifying patterns to executing trades, this method emphasizes clear signals and reliable tools. Stop-losses should be placed just beyond the mother bar or positioned 1 ATR away to limit risk effectively. Coupled with a minimum 1:2 risk-to-reward ratio, the structured nature of inside bars supports outcomes that favor disciplined traders.

"The market moves from a period of low volatility to high volatility... if you trade a small range Inside Bar, it means volatility is low and there's a good chance it could expand in your favour."

- Rayner Teo, Founder, TradingwithRayner

QuantVPS enhances this strategy by delivering ultra-low latency execution, ensuring orders are processed instantly during fast-moving breakouts. With 0–1ms latency to key financial venues and a 100% uptime guarantee, automated strategies can operate seamlessly, monitoring setups around the clock. This dependable infrastructure reduces operational risks and keeps emotions out of the equation, helping traders stick to their plans.

FAQs

How do I filter out false inside bar breakouts?

To steer clear of false inside bar breakouts, it's essential to confirm the move using volume analysis. Typically, stronger breakouts are accompanied by a noticeable increase in trading volume. Also, assess the market context - a valid breakout often follows a period of clear consolidation, such as multiple inside bars forming consecutively.

Once you've confirmed the breakout with volume or clear trend direction, set a stop-loss on the opposite side of the inside bar. Following these steps can help improve the reliability of your trades.

What’s the best way to size positions with mother-bar stops?

To size positions using mother-bar stops, place your stop-loss on the opposite side of the mother bar. Then, adjust your position size to manage your risk effectively. Here's how: divide the amount you're willing to risk (for example, $200) by the distance between your entry point and the stop-loss. This method helps you maintain strict risk control, guards against false breakouts, and positions you for potentially significant returns.

Should I trade inside bars during low-volume or news sessions?

Avoid trading inside bars during low-volume or news sessions. These times usually come with reduced volatility and market indecision, which can lead to false breakouts.

To manage risk more effectively, look for confirmation signals - such as a breakout above or below the inside bar’s range. It’s best to do this during active trading hours when liquidity is higher, and price movements tend to be more dependable.